(NYSE:NLY)")

")

Standard Motor Products (NYSE:SMP), an automotive parts manufacturer saw its stock plummet last month after reporting disappointing fourth quarter earnings. The selloff intensified in the couple of weeks following the report until the stock made a new 52 week low, down 25%. After reviewing the company’s earnings report and outlook, I purchased shares of Standard Motor Products as I believe the company is a good value play for investors.

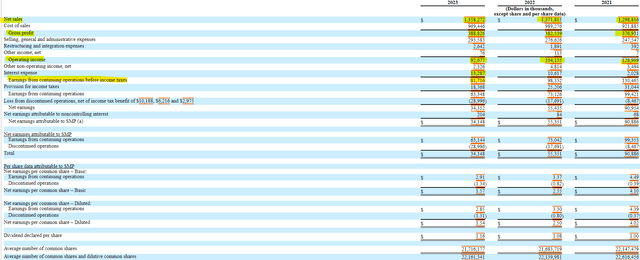

Standard Motor Product’s profitability did take a hit in 2023. The company saw sales fall by 1% to $1.36 billion. Fortunately, the cost of sales dropped by more than revenue, which allowed gross profit to grow by $6 million to $389 million. Where the pain came from was in the form of selling, general, and administrative expenses, which grew by $17 million. The growth in SG&A led to the drop in earnings before income taxes from $98 to $81 million.

SEC 10-K

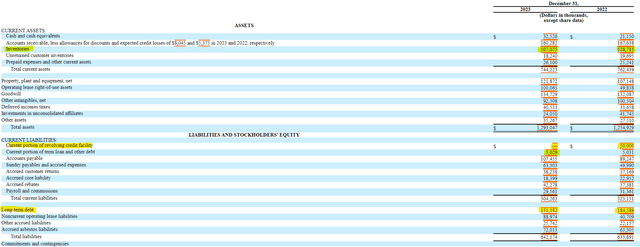

Despite the decline in profitability, Standard Motor Products did make improvements to the balance sheet during 2023. The company managed to pay down its long-term debt from $239 million to $156 million. The $83 million reduction in debt came with the assistance of a $21 million decline in inventory, which is still impressive as the company should not need much on the cash flow side to replenish inventory. Shareholder equity grew to $650 million from $621 million. At a market capitalization of $725 million, the company is trading at a modest 1.1 times book value.

SEC 10-K SEC 10-K

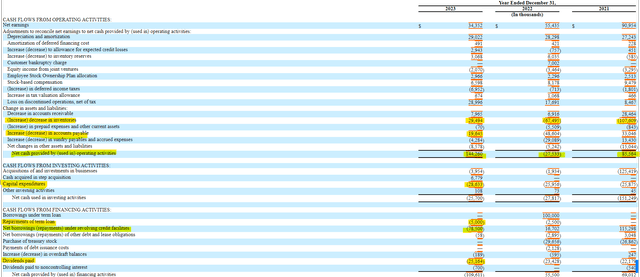

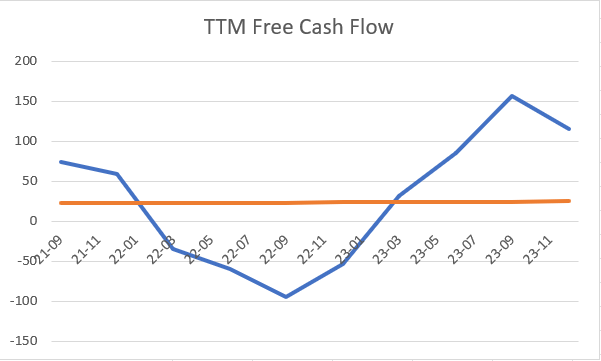

From a cash flow standpoint, Standard Motor Products had an outstanding year. While increases in inventory and paying down payables had an inverse effect on cash flow in 2022, the reverse happened in 2023. The company generated operating cash flow of $144 million, and a free cash flow of $116 million. This allowed the company to pay dividends of $25 million and reduce debt by $83 million. Even if working capital changes were at $0, the company would have been able to pay down more than $30 million of debt. On a trailing twelve month basis, Standard Motor Product’s free cash flow excelled for five straight quarters before taking a break in the fourth quarter.

SEC 10-K TIKR

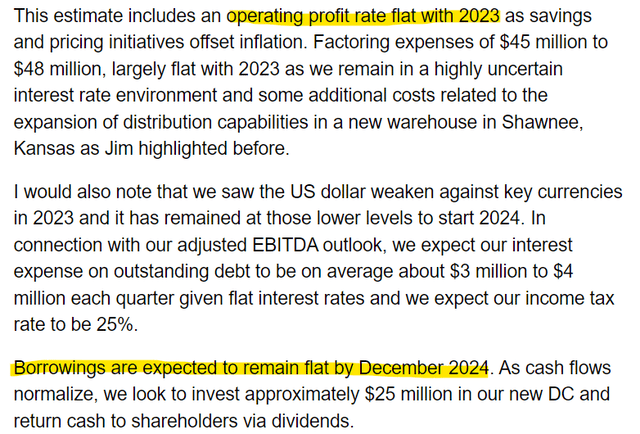

After making such strong progress on its debt paydown during 2023, investors may have been disappointed to hear the company guide no debt paydowns for 2024, but the company does not have any debt coming due until 2027. Additionally, the company has $340 million in additional liquidity, mostly available through a $400 million revolving credit facility, which only has $63 million drawn.

Earnings Transcript SEC 10-K

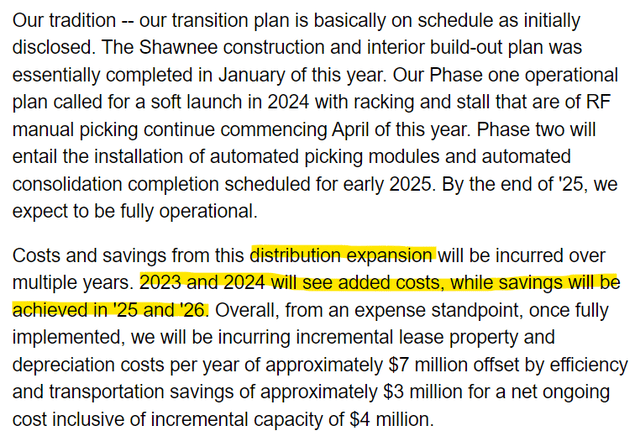

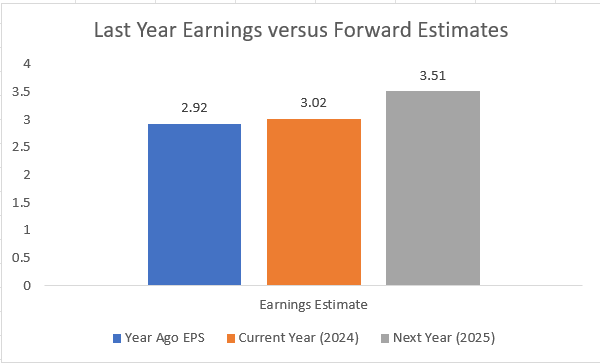

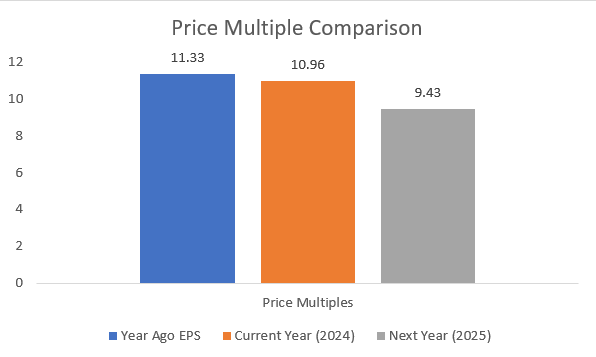

In addition to earnings headwinds, Standard Motor Products is in the second year of a two-year distribution expansion. This expansion will lead to higher costs in 2024, but ultimately grow profitability in 2025 and 2026. Analysts are projecting more than 15% earnings growth in 2025, which leads to the stock trading at a great value of less than 9.5 times next year’s earnings.

Earnings Transcript Yahoo Finance Yahoo Finance

Being a supplier to the automotive sector does raise macroeconomic risks for Standard Motor Products. If the consumer comes under pressure from higher unemployment and/or lower wage growth, the corresponding consumption changes could negatively impact the industry and company earnings.

I believe that the selloff in Standard Motors Products stock was overdone. The company is facing some short-term earnings pressure, but not nearly enough to justify a 25% selloff. I believe that Standard Motors Products will return to the $40 per share level later this year with more upside potential depending on outlook.

Despite the risks, I believe Standard Motor Product’s stock is a good value play for investors. The company has taken measures to grow free cash flow and use those proceeds to pay down a good chunk of debt. I have no reason to believe that their investments in distribution won’t be successful in the long term. I’ve decided to take a long position at less than 10 times next year’s earnings and will consider dollar cost additions.

Q1 2024 Earnings Call Transcript")

")

")

")