")

")

Researchers working in a laboratory.

In investing, some of my favorite investments are what I like to call triple threats/triple plays/triple shots. These include Automatic Data Processing (ADP) and UnitedHealth Group (UNH). What do I mean?

For those who are especially attentive, my primary headline for this article may give the answer away. By triple shot, I mean a stock that provides shareholders with the following attributes:

- 1) Decent starting income. My requirement is generally that the starting yield is at least higher than the S&P 500 index’s (SP500) 1.4% yield. I also generally prefer that the yield be greater than the sector median per Seeking Alpha’s Quant System.

- 2) Solid earnings growth potential. The metric that I typically like to examine is the 3-5Y CAGR for EPS forward long-term growth in the Quant System.

- 3) A discounted valuation. This can be relative to a company’s fundamentally justified valuation and/or its sector median. A helpful metric can include the forward non-GAAP PEG ratio within Seeking Alpha’s Quant System.

One triple shot pick that I don’t own but remain optimistic toward is the United Kingdom-headquartered pharmaceutical company, AstraZeneca (NASDAQ:AZN). At the time when I initiated coverage with a strong buy rating last October, I was impressed by the wide margin of outperformance versus the S&P 500 over 10 years. For context, AstraZeneca’s 282% cumulative total returns were much better than the 200% cumulative total returns of the S&P over that time.

Since that time, the drugmaker’s 16% capital appreciation was in line with the S&P’s 16% gains. Adding in dividends, the 18% total returns were slightly ahead of the S&P.

Today, I’m going to be going over AstraZeneca’s first-quarter earnings results that were released April 25. The market was impressed enough to send shares rallying by nearly 6% in intra-day trading.

Without getting too much into it here, I am also impressed enough to reaffirm my belief the company’s fundamentals remain vigorous here. Overall, everything about AstraZeneca is as impressive as ever. The recent rally and valuation are the only reasons that I’m downgrading AstraZeneca from a strong buy rating to a buy rating.

AstraZeneca Knocked Q1 Out Of The Park

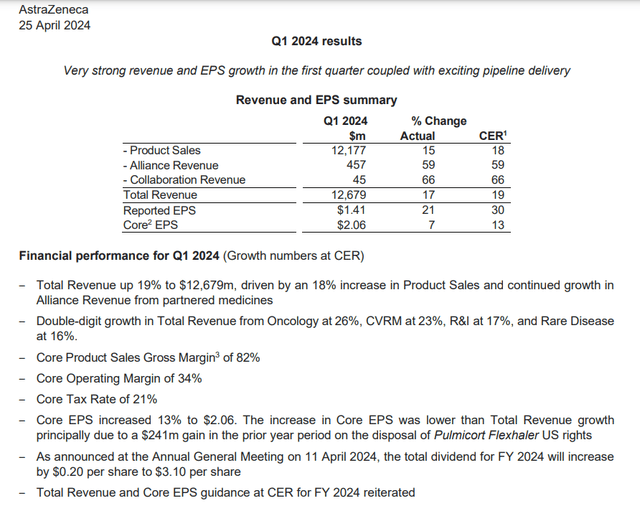

AstraZeneca Q1 2024 Earnings Press Release

When AstraZeneca shared its first-quarter results this morning, it certainly didn’t disappoint. On the contrary, the drugmaker’s total revenue climbed 17% year-over-year to $12.7 billion during the quarter. According to Seeking Alpha, this was ahead of the analyst total revenue consensus by a whopping $850 million.

If this topline growth isn’t strong enough, it gets even better. When accounting for unfavorable foreign currency translation, AstraZeneca’s currency-neutral total revenue surged by 19% in the first quarter.

That brings us to the question at hand: What was behind these admirable results?

It was a complete effort throughout the business but in a word: Oncology. This therapy area accounted for approximately 40% of AstraZeneca’s total revenue for the first quarter. In oncology, the company has six drugs that are on pace to be blockbusters this year. Each of these six medicines posted revenue growth during the quarter, ranging from 8% for Lynparza to 79% for Enhertu. These results were driven by increased uptake rates and recently launched new indications. That propelled oncology revenue 23% higher over the year-ago period to $5.1 billion in the quarter.

Led by strength from the heart failure/type 2 diabetes/chronic kidney disease hit Farxiga, the BioPharmaceuticals segment posted almost $3.1 billion in first-quarter revenue. That was enough for a 20% year-over-year growth rate. This was a key secondary growth driver for AstraZeneca.

Another lesser growth catalyst for the company came from the respiratory and immunology therapy area. The R&I therapy area logged $1.9 billion in total first-quarter revenue, which was up 15% over the year-ago period. Even with generic pressures on Symbicort, the asthma and COPD drug more than offset this with strong underlying demand throughout both China and ex-China markets.

The rare disease therapy area was another component of AstraZeneca’s growth for the first quarter. Growth in U.S. GMG patients and launches in emerging markets helped Ultomiris’ revenue to rise by 32% to $859 million. This pushed total therapy area revenue higher by 12% to $2.1 billion during the quarter.

Vaccines and immune therapies and other medicines were the only two therapy areas that didn’t grow in the first quarter. Falling other medicines revenue and Nexium revenue led other medicines revenue to fall by 7% to $297 million for the quarter. Substantially reduced demand for COVID-19 antivirals and vaccines resulted in a 35% plunge in V&I revenue to $232 million during the quarter.

Moving to the bottom line, AstraZeneca’s core EPS grew by 7% year-over-year to $2.06 in the first quarter. That was $1.11 higher than anticipated by the analyst consensus per Seeking Alpha. Backing out unfavorable foreign currency translation, this growth rate was even higher at 13%.

The reason why core EPS growth lagged total revenue growth had to do with a transaction in the year-ago period: A $241 million gain on the sale of U.S. rights to the maintenance asthma treatment, Pulmicort Flexhaler.

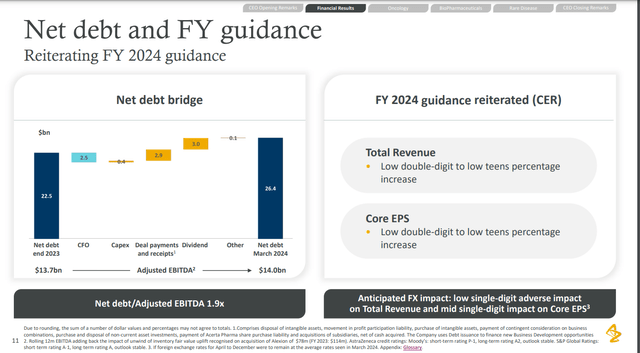

AstraZeneca Q1 2024 Investor Presentation

AstraZeneca’s results were enough for the company’s executive team to reiterate their previous guidance of low double-digit to low teens percentage growth in both total revenue and core EPS for 2024.

I think this guidance makes sense for at least a few reasons. For one, the company’s existing product portfolio is demonstrating its worth. Quarter after quarter, AstraZeneca’s blockbuster products are improving uptake.

Secondly, it’s worth noting that new product launches are happening consistently and I expect this to continue. As of April 25, the company had 182 projects in its pipeline, with 19 of those being new entities in the late-stage pipeline.

In the first quarter, Beyfortus was approved in China to prevent RSV disease in infants. Voydeya was approved in Japan to treat adults with PNH in combination with Ultomiris or Soliris. According to AstraZeneca, the latter will address the needs of a subset of 10% to 20% of patients with PNH who experience clinically significant extravascular hemolysis with a C5 inhibitor like Ultomiris or Soliris.

These are just two of a handful of product launches that happened in the first quarter alone. That should help to further grow the topline at a double-digit rate in the quarters to come.

Also, the aforementioned gain of the U.S. rights to Pulmicort Flexhaler is now in the rearview. That means the bar for the company to clear to post double-digit core EPS growth will be lower in the quarters ahead.

Management’s expectations and my expectations jive with the Seeking Alpha Quant System’s 12.1% 3-5Y compound annual growth rate for forward EPS. For perspective, that’s also moderately better than the healthcare sector median of 11%. The FAST Graphs consensus of 11% core EPS growth in 2024, 14% core EPS growth in 2025, and 9% core EPS growth in 2026 also line up.

Moving forward, I will be focused on whether the company can keep delivering new and commercially successful products to the market. If that is the case as I suspect it will be, these growth forecasts should be proven right.

On the balance sheet front, AstraZeneca’s net debt to adjusted EBITDA was less than 2 in the first quarter. This demonstrates that the company’s $26.4 billion debt load is manageable against its $14 billion in trailing twelve months adjusted EBITDA. I believe that is why S&P awards an A credit rating to AstraZeneca on a stable outlook (unless otherwise stated or hyperlinked, all details in this subhead were sourced from AstraZeneca’s Q1 2024 Earnings Press Release and AstraZeneca’s Q1 2024 Investor Presentation).

I Don’t Love The Valuation Anymore But I Still Like It

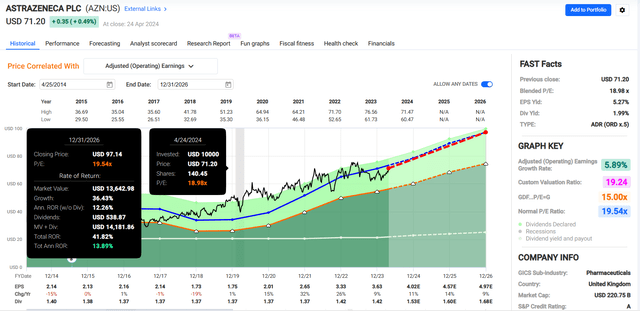

FAST Graphs, FactSet

From the current $75 share price (as of April 25, 2024), AstraZeneca’s shares are priced at a current-year P/E ratio of 18.7. This is below the 10-year normal P/E ratio of 19.5, which I think is a great value. The earnings growth consensus from FAST Graphs is reasonable in my view and would represent an acceleration over much of the last 10 years.

That’s why I am confident that the valuation multiple could revert to 19.5 moving forward. Plugging in the $4.02 FAST Graphs core EPS consensus for 2024, this would be a 2024 fair value of $79 a share. Using the $4.57 FAST Graphs core EPS consensus for 2025, I would get a 2025 fair value of $89 a share.

Markets tend to focus on the next 12 months. Thus, I am opting to weight these fair values for the 67% of 2024 that remains and 33% of 2025 that lies ahead. This gives me a weighted average fair value of $82 a share. That would imply shares of AstraZeneca are 8% undervalued.

This isn’t quite the margin of safety that was present in my last article, which is why I no longer have a strong buy rating. However, the 1.5 forward non-GAAP PEG ratio is below the healthcare sector median of 1.9 (up to par for a B grade from Seeking Alpha’s Quant System). This still makes AstraZeneca a decent value in my view.

The Starting Dividend Remains Appealing

AstraZeneca’s 2.1% forward dividend yield compares favorably to the 1.6% median yield of the healthcare sector. This is enough to earn a B grade within Seeking Alpha’s Quant System for forward dividend yield. Earlier this month, the dividend was also hiked by almost 7%.

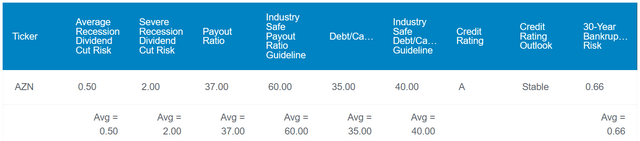

Dividend Kings Zen Research Terminal

AstraZeneca has room to further grow the dividend, too. The company’s 37% EPS payout ratio is below the 60% that rating agencies prefer from the industry.

AstraZeneca’s dividend is also covered by free cash flow. Through the first quarter of 2024, the company generated $2.1 billion in free cash flow. AstraZeneca’s dividends paid during that time were just over $3 billion. But adjusting for the fact these dividends were paid for the first half and not just the first quarter, the free cash flow payout ratio would have been manageable at 71.5% (info according to AstraZeneca’s Q1 2024 Earnings Press Release).

Risks To Consider

AstraZeneca is executing in every aspect of its business. The company is properly managing its existing product portfolio by taking more market share and launching new indications. AstraZeneca is also developing plenty of next-generation products that could also become blockbusters. However, there are still risks to the company.

These are largely the same as my prior article. The biggest risk to AstraZeneca is the same as any other big pharma pick. If the company can’t develop and advance enough drugs through clinical trials and to the market to reach commercial success, the fundamentals could suffer. That could translate into AstraZeneca not growing as analysts expect.

Just like any other big pharma player, the company also faces both regulatory and litigation risks. Major legislative overhauls in key markets could stunt growth. Not to mention that any sizable and successful lawsuits could weigh on AstraZeneca’s free cash flow/earnings.

Summary: An Interesting Pick For A Mix Of Reasons

AstraZeneca is intriguing in so many ways. The company’s above-average dividend yield appears to be secure to me. Above-average growth prospects look to be supported by the fundamentals picture as well. The value isn’t as compelling as it was six months ago, but it is still there for the taking. For these reasons, I’m updating my coverage of AstraZeneca with a buy rating.

Q1 2024 Earnings Call Transcript")