")

")

The Polen Capital Global Growth ETF (NYSEARCA:PCGG) is an actively managed ETF concentrating capital in 25-40 global large cap stocks of what the manager believes are high-quality companies.

Although we can appreciate the fund’s emphasis on owning competitively advantaged businesses that have sustainable, above-average earnings growth, we’re initiating coverage on PCGG with a Hold rating due to concerns around valuation.

We agree the fund owns many of the highest quality businesses in the world, including Microsoft, Alphabet, Mastercard, and Visa. However, we also think many of these stocks are pretty expensive, and lack the margin of safety we require to invest.

The ETF has a limited track record since it was only just launched in August of last year, but its strategy is the same as the longer-running Polen Global Growth Mutual Fund (PGIIX), which launched in December 2014 and has outperformed its benchmark with an +11.76% return vs. +8.97% for the MSCI ACWI through March 31, 2024.

Despite the fund’s solid absolute and relative returns since inception, we remain disciplined on valuation and believe more expensive, higher-growth stocks could face a correction if rates stay higher for longer and/or the Fed’s first rate cut is further out than the market currently expects.

Overview of the Manager

Polen Capital is a well-respected growth manager with a solid track record. Founded in 1979, the firm focuses on high-quality growth companies with sustainable competitive advantages, strong balance sheets, and robust earnings growth potential.

In our view, Polen’s disciplined investment process, experienced team, and long-term orientation are some of the manager’s key differentiators.

We view Polen Capital positively due to its commitment to quality, strong alignment of interests with investors as the PMs “eat their own cooking” and invest in the same strategy alongside LPs, as well as a solid long-term track record.

While we have valuation concerns about the current portfolio, we think Polen is a high quality manager worth watching.

Performance

Since PCGG was launched less than a year ago, for the purposes of our performance review we focused on the mutual fund vehicle (PGIIX) which was launched in 2014 and is managed within the same strategy as the PCGG.

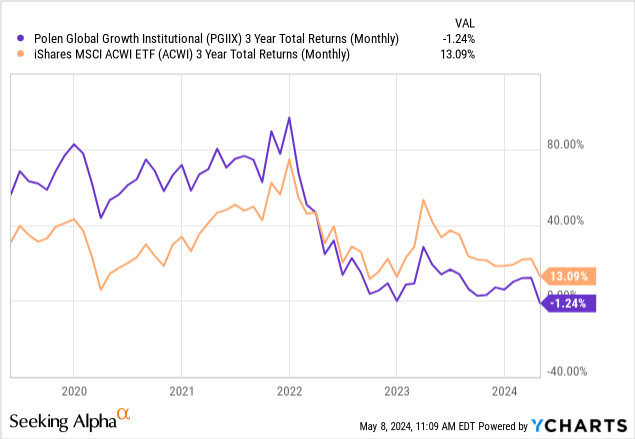

While performance has generally been solid, and the strategy has outperformed its benchmark since inception, the strategy’s 3-year rolling returns, included in the chart below, highlight a performance pattern worth noting.

Thus far, the return profile of the fund seems highly correlated to the performance of the growth factor. As growth led the markets coming out of the pandemic, Polen was meaningfully outperforming its benchmark. When growth significantly unperformed in 2022, the strategy experienced a roughly -30% drawdown, underperforming its benchmark that year by more than 12%. That disappointing period of performance has weighed on the strategy’s 3-year rolling returns, and as such Polen still has a lot of ground to cover to catch up.

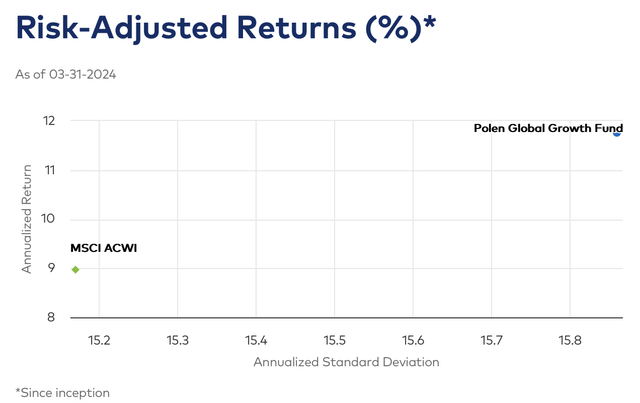

As previously mentioned however, the fund’s longer term absolute and relative performance is solid, as shown in the chart below. Day one investors in the fund have been rewarded for the volatility they’ve been willing to stomach, as the fund has solidly outperformed its benchmark since its inception in 2014.

Polen Capital Global Growth – Risk-Adjusted Returns Since Inception vs. MSCI ACWI (as of March 31, 2024) (Polen Capital)

While the manager has displayed an ability to generate solid long term returns, we wonder how repeatable that performance is in light of the new higher interest rate environment we find ourselves in today. While growth and momentum has thus far led the markets in 2024, we think expensive higher growth stocks could be in for a bumpy ride if valuations come back to earth.

Speaking of valuations…

PCGG: Top Holdings & Valuations

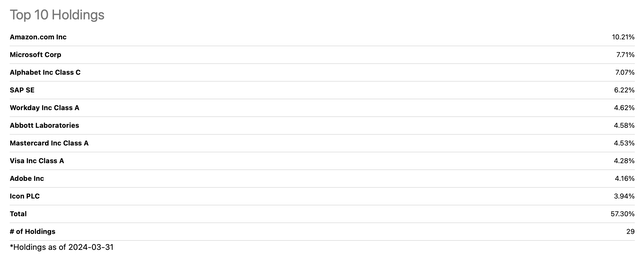

As we mentioned earlier, PCGG owns many of the best businesses in the world in our view, as outlined in the table below.

PCGG – Top 10 Holdings (as of March 31, 2024) (Seeking Alpha)

We are less enthused by the manager’s willingness to pay up for these businesses. Many of the fund’s top holdings are trading around 30x FCF or more, more than double where the benchmark is trading today.

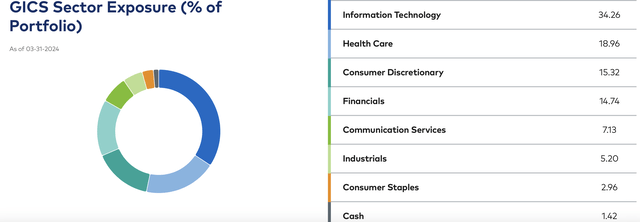

Given the fund’s focus on growth, it tends to have a concentration in Tech, Healthcare, and Consumer stocks, which make up most of the fund today.

Polen GICS Sector Exposure (Polen Capital)

The fund’s focus on large-cap growth stocks in sectors like Tech, Healthcare and Consumer has led to an overall portfolio that appears at least fully valued to us.

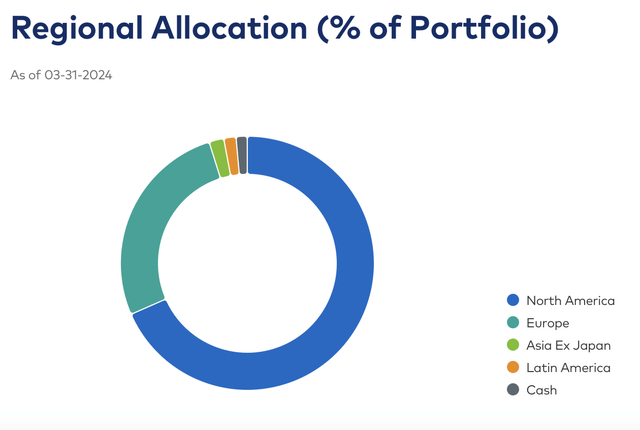

We do like the fund’s global orientation, which should allow the manager to pivot from the U.S. to international markets as the opportunity set abroad becomes more attractive. That said, the fund is mostly North America today, as outlined in the chart below.

Polen Regional Allocation (Polen Capital)

Key Risks

The fund is fairly concentrated, with 25-40 holdings on average and the majority of the portfolio in the top 10 holdings. And given the fund’s high active share (~85%), investors should expect the performance profile of the fund to look much different than its benchmark over time.

In our view, the biggest risk is valuation. The fund’s focus on high-quality, large-cap growth stocks has led to a portfolio that we think is at least fully valued, and could be vulnerable to multiple compression in the current environment.

The fund’s global mandate could also elevate the fund’s risk profile, as we think investing in developing markets involves greater risk. Historically, the fund has primarily focused on developed markets where risk is comparable to the U.S. in our view.

PCGG: Watching from the Sidelines

While PCGG offers investors exposure to a concentrated portfolio of high-quality, global large-cap growth companies, we are initiating coverage with a Hold rating due to valuation concerns.

Although we appreciate Polen Capital’s disciplined investment process, experienced team, and solid long-term track record, we believe the fund’s holdings are at least fully valued and vulnerable to multiple compression if interest rates remain elevated.

Until valuations become more attractive, we’ll remain on the sidelines.

")

")