(NYSE:NLY)")

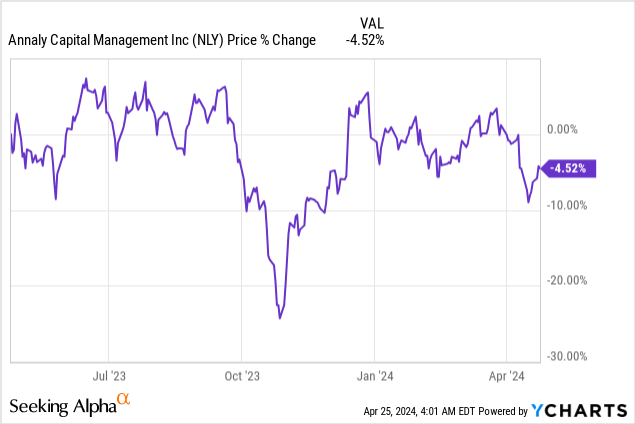

Annaly (NYSE:NLY) reported mixed first quarter earnings on Wednesday that showed an improving spread picture as well as as another quarter of book value growth, but the mortgage REIT also slightly missed earnings expectations. Recently, Annaly has seen some share price weakness which followed the revelation of higher than expected inflation numbers in March… which suggests that the Federal Reserve will want to take it easy with federal fund rate cuts in 2024. However, shares of Annaly are priced at a discount to book value (as well as below the 3-year average P/B ratio) and dividend investors can take advantage of recent share price weakness. The strength of Annaly’s first-quarter earnings sheet, especially the improving net interest spread, also supports my change in the stock rating to buy!

Previous rating

I rated Annaly a hold in February because shares re-priced to book value and because of the relative safety of the company’s double-digit dividend yield (which was supported by Annaly’s earnings available for distribution). I am upgrading Annaly to buy because of the REIT’s solid Q1’24 earnings sheet, return to book value growth as well as a more attractive valuation available to dividend investors. Key take-aways from the earnings report were that Annaly did not cover its dividend with earnings available for distribution, the mortgage REIT posted another quarter of book value growth and the net interest spread improved Q/Q.

A leading mortgage REIT with an improving spread picture

Annaly was not an especially attractive investment for dividend investors as the Federal Reserve raised the federal fund rate aggressively in FY 2022. Higher interest cost hurt the mortgage REIT during the last rate-expansion cycle, but the situation is slowly improving for Annaly, in large part because the market expects the Federal Reserve to be cutting the federal fund rate soon, potentially creating relief on the borrowing side of the equation for Annaly.

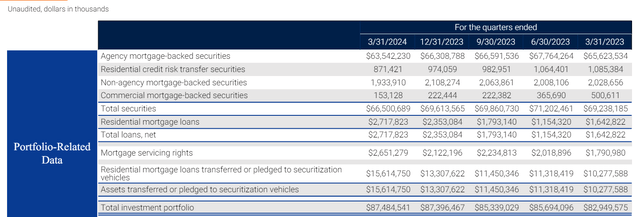

Annaly is chiefly invested in mortgage-backed securities that are issued by a government-sponsored enterprise which benefit from the full faith and credit of the U.S. government. In the first-quarter, Annaly owned $64.7B in agency securities which made it by far the biggest investment block for the mortgage REIT. Additionally, Annaly owned commercial MBS, mortgage servicing rights and residential mortgage loans that generated recurring income for the mortgage trust.

Annaly will continue to remain chiefly an agency MBS play for dividend investors that seek to generate recurring dividend income. I also expect Annaly to reduce its exposure to mortgage servicing rights going forward as these instruments fall in value when interest rates decrease. Therefore, they are more suitable investments for a rising-rate world than for a falling-rate world. MBS investments, on the other hand, stand to benefit from a lower federal fund rate.

Annaly

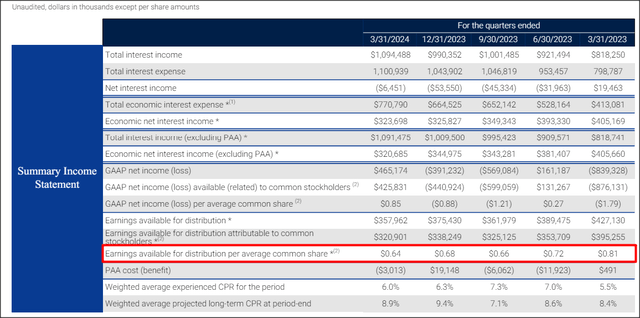

In the first fiscal quarter, the mortgage REIT generated a net interest spread — which is the difference between financing costs and yield on the REIT’s interest earnings assets — of negative 0.52%. It was the fifth straight quarter of Annaly achieving a negative interest spread which is a reflection of the Federal Reserve raising the federal fund rate, making leverage for mortgage REITs more expensive. The widening of MBS spreads is chiefly responsible for Annaly’s large book value contraction last year. I expect Annaly to return to a positive net interest spread in the second half of the year, as the Federal Reserve gets going on cutting the federal fund rate.

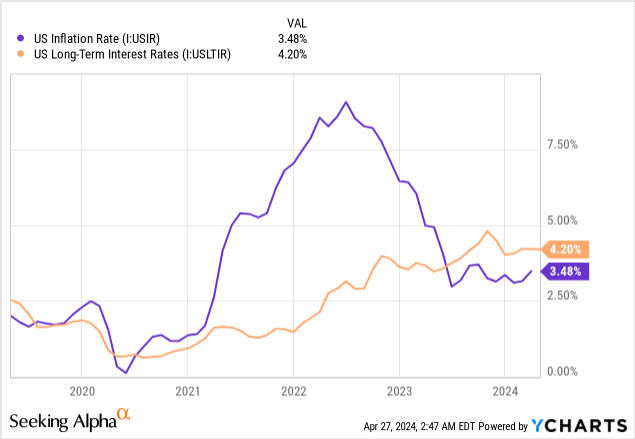

While inflation has been going up lately, it is still down significantly on a year over year basis. This strongly suggests that the Federal Reserve will follow suit and start to initiate federal fund rate cuts in the second half of the year. Another incentive for the Federal Reserve to lower the federal fund rate is that inflation has fallen below long term interest rates, making rate cuts ever more likely in FY 2024.

A change in the net interest spread could be a catalyst for a re-pricing of Annaly’s shares, but also for better dividend coverage.

|

NIS profile |

FY 2024 |

FY 2023 |

|||

|

1st quarter |

4th quarter |

3rd quarter |

2nd quarter |

1st quarter |

|

|

Net interest margin |

-0.03% |

-0.25% |

-0.20% |

-0.15% |

0.09% |

|

Average yield on interest earning assets |

4.88% |

4.55% |

4.49% |

4.27% |

3.96% |

|

Average GAAP cost of interest bearing liabilities |

5.40% |

5.37% |

5.27% |

5.00% |

4.52% |

|

Net interest spread |

-0.52% |

-0.82% |

-0.78% |

-0.73% |

-0.56% |

(Source: Author)

Annaly’s 14% supported by earnings

Given the dividend coverage profile for Annaly, I believe the dividend at this point is sustainable. Annaly slightly under-earned its dividend with earnings available for distribution in the first-quarter (by $0.01 per-share), but the mortgage REIT managed to cover its dividend on an LTM-basis: in the last year, Annaly had a dividend coverage ratio of approximately 104%. As a result, I consider a dividend cut to be highly unlikely in FY 2024.

Annaly

Return to book value growth

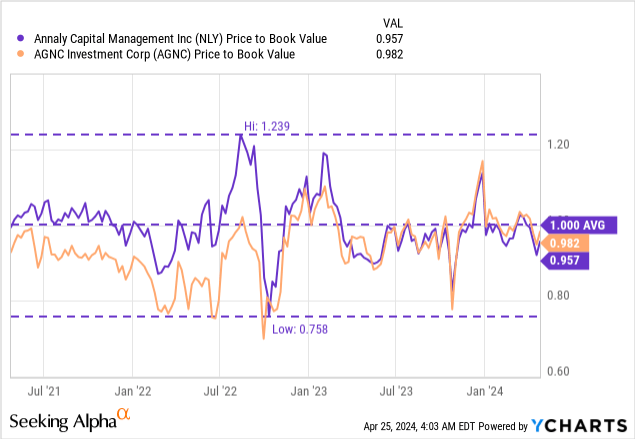

Annaly managed to grow its book value again in the first fiscal quarter which makes it the second quarter of growth in a row. Annaly’s book value per common share at the end of Q1’24 was $19.73, showing 1.5% Q/Q growth, but also a 5.0% Y/Y decline. Shares of Annaly are currently trading at a P/BV ratio of 0.96X compared to a 3-year average P/B ratio of 1.0X. I generally believe that Annaly becomes attractive as a buy once shares trade below book value as it improves the safety margin for dividend investors. This is especially true with the net interest spread improving and the Federal Reserve being on the cusp of lowering the federal fund rate. In the longer term, I expect Annaly to revalue to book value ($19.73). I therefore also raise my fair value estimate from $19.44 to $19.73 (reflecting the long term P/B ratio of 1.0X). AGNC Investment (AGNC) is valued at a P/BV ratio of 0.98X. Both NLY and AGNC have traded at very similar price-to-book ratios over time.

Risks with Annaly

The biggest risk for Annaly is the manifestation of a higher for longer rate environment. If inflation continues to go up in the coming months, the Federal Reserve may push federal fund rate cuts back into FY 2025 which would delay a return to a positive net interest spread for Annaly. What would change my mind about the mortgage REIT is if Annaly’s book value declined again or Annaly failed to support its dividend with earnings available for distribution. Two metrics that I am monitoring in this regard at the net interest spread and the dividend coverage ratio (based off of distributable earnings).

Final thoughts

I believe the value and risk proposition of Annaly has considerably improved after Q1’24 earnings due to three factors: 1) Annaly’s book value is growing, 2) Overall dividend coverage metrics still look good (they are above 100% on an LTM-basis), and 3) Shares are trading at a discount to Q1’24 book value. In the medium term, the earnings and spread picture should continue to improve as the Federal Reserve is set to lower its federal fund rate which should 1) Increase the REIT’s net interest spread due to lower financing costs, and 2) Take pressure off of the REIT’s mortgage-backed security portfolio. While the short term earnings and spread out look remains challenging, Annaly’s share price weakness and discount to book value make NLY a buy in my book!

")

Q1 2024 Earnings Call Transcript")