")

My Thesis

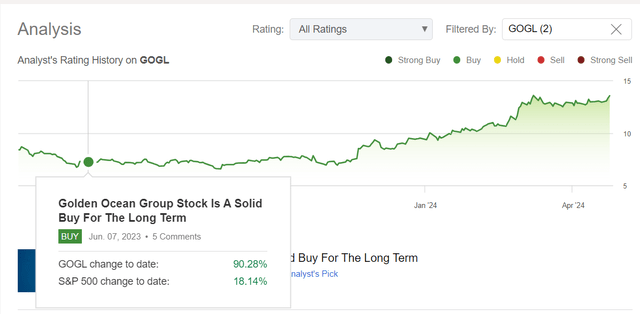

When I last wrote about Golden Ocean Group Limited (NASDAQ:GOGL) stock in June 2023, it was trading at $7.6 – at the time of this writing it’s trading at $13.8, and GOGL’s total return for the period indicated is around 90%. That’s more than five times what the market, as represented by the S&P 500 Index (SPX), has shown.

Seeking Alpha, Oakoff’s coverage of GOGL

And although at first glance it may seem that now is the time to “cast out the line” and sell GOGL after this great rally, I think otherwise. In my opinion, this stock should continue to experience strong tailwinds both due to the unexpected improvement in its financials (compared to what the consensus priced in initially) and the specifics of its shipping niche.

My Reasoning

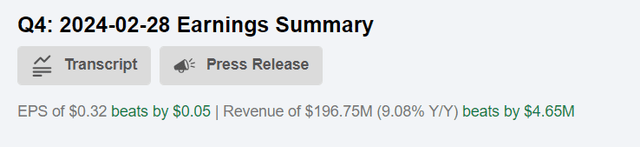

Traditionally, I like to start with financial analysis – here GOGL has something to brag about. The world’s largest owner of large bulk carriers has published its financial figures for Q4 FY2023, with revenue of almost $197 million and adjusted earnings per share of $0.32 – both figures came significantly above the consensus expectations:

Seeking Alpha, GOGL

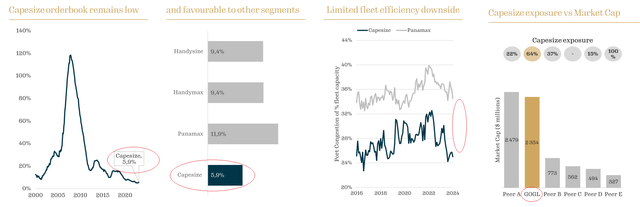

In Q4, net income surged to $57.5 million from $28.7 million, but for the full year, GOGL’s net income totaled $112.3 million, down from $461.8 million in 2022. The company made some important strategic moves, including selling a Supramax vessel and arranging financings of ~$625 million, ensuring their financial obligations are fully met until 2026. They also entered into agreements to sell another vessel, apparently trying to optimize their fleet. At the moment, GOGL is the only public pure-play capesize provider on the market – in theory, this shipping niche should suffer less than others from the imminent influx of new supply (which many shipping investors are afraid of).

GOGL’s IR materials, Oakoff’s notes

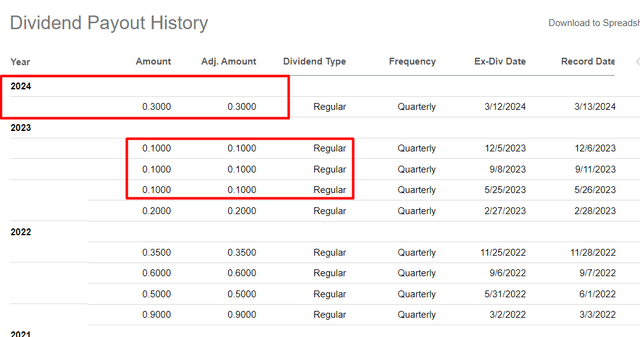

For the 11th consecutive quarter, GOGL announced a cash dividend of $0.30 per share for Q4 2023 – that was 50% more than last year or like the past 3 quarters of payouts combined:

Seeking Alpha, Oakoff’s notes

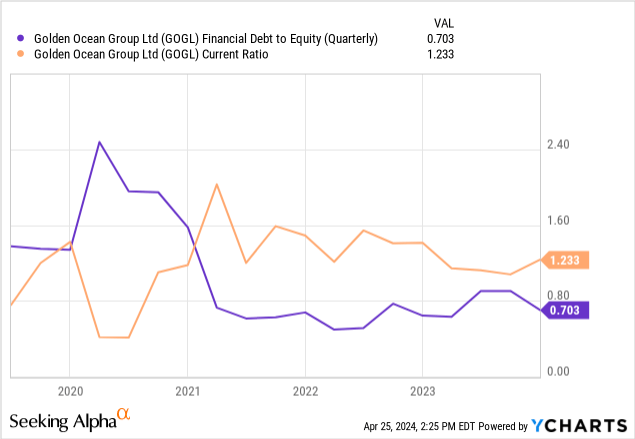

Importantly, the company ended the quarter with increasing liquidity (the current ratio rose above 1.2) and decreasing debt-to-equity ratio (now it’s ~0.7). GOGL’s balance sheet looks clean, despite some external challenges from the market.

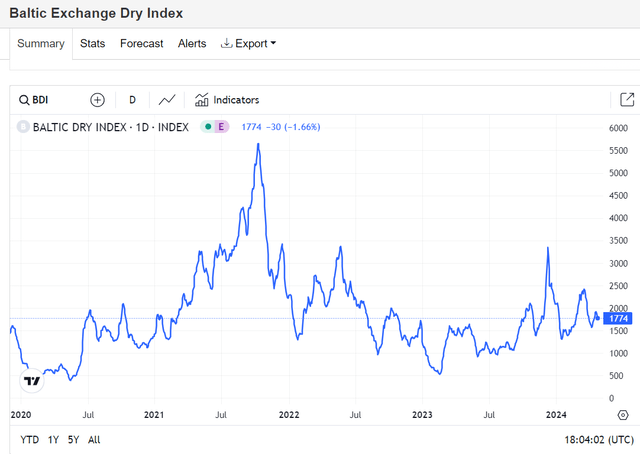

Obviously, the trend towards lower freight rates, which started from the peak in October 2021, when the problems in global logistics started to gradually resolve, put a lot of pressure on GOGL’s business. The same fate befell the rest of its peers, so Golden Ocean is not alone in this respect.

TradingEconomics

The freight rate jumped from time to time as you can see, but the downward trend remained unchanged. This led to the market starting to price in a sharp deterioration in GOGL’s EPS. If you open my June article on the company out of curiosity, you will see that Wall Street was expecting earnings of only $0.9 per share for FY2023, which was almost 53% less than in FY2022:

Seeking Alpha, GOGL

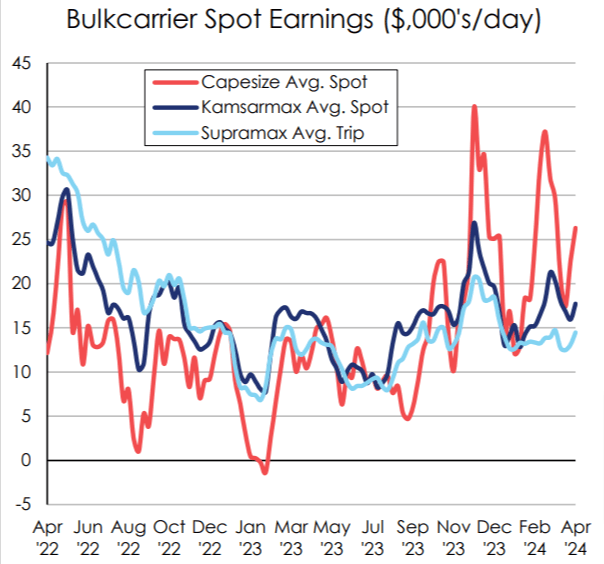

At the end of the year, this forecast was lowered by a further 42% and GOGL was only expected to generate EPS of $0.52 for the full year 2023. But from the freight rates movement chart above – the Baltic Dry Index – we see that the trend has actually already changed. Moreover, the Capesize market is one of the leaders of this trend reversal:

Shared by Ed Finley-Richardson (On X: @ed_fin)

Against this backdrop, it’s not surprising that GOGL is trying to build on its previous highs, even against the backdrop of such a sharp decline in sales, EBITDA, and net profit last year (compared to 2022).

TrendSpider, Oakoff’s notes

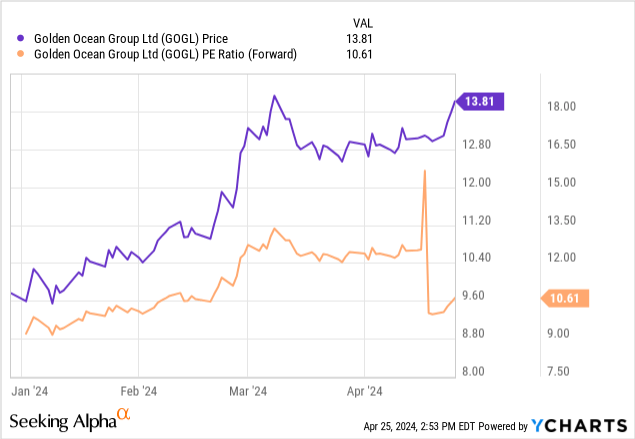

Shipping is all about cyclicality, so you can’t look at TTM data when assessing the growth prospects of a particular company – anything in the past is no guarantee for the future, this wisdom should be taken literally in shipping. What do I see with GOGL? Firstly, the company has succeeded in significantly reducing its debt – the process of debt reduction has been in full swing recently and has not stopped at the deterioration in profitability. Secondly, the company’s liquidity has increased noticeably – I do not believe that GOGL will have any problems in this respect in the foreseeable future. Thirdly, GOGL is a pure Capesize play – this is the sweetest piece of the dry bulk carriers niche if we consider the order book and potential profitability going forward. These three points are already enough to justify the move in the stock that you see in the chart above – i.e. the stock’s appreciation has fundamental underpinnings even if we take geopolitics out of the equation (which I always recommend, because geopolitics are the hardest to predict). Fourthly, GOGL had an upside from its cheap valuation. By maintaining a decent dividend, the company proved its strength to all income-seeking investors and “forced” them to pay more – the forwarding P/E multiple has risen in recent weeks before falling sharply a few days ago:

This sharp decline in the multiple hides one of the additional arguments for my updated “Buy” thesis: Wall Street’s revised projections for GOGL, which assumingly consider the recent momentum in freight rates, make the company cheap again at 10.6x forwarding earnings.

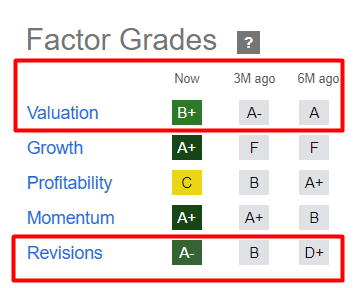

Yes, this multiple may seem a little high in a historical context – GOGL is no longer as dirt cheap as it was a few months ago. But the stock can’t be described as expensive – I’d call it “affordable, inexpensive”. Especially when you consider that a) the end market has become stronger and b) analysts have started to revise their estimates. This is most evident in Seeking Alpha’s Quant grades:

Seeking Alpha, GOGL’s grades, Oakoff’s notes

That’s why I decided to update my coverage with a “Buy” rating today, waiting for GOGL’s rally continuation.

Risk Factors To Consider

First, I could be wrong about the cyclicality. I wouldn’t wish to be in shipping during a down cycle on anyone – I experienced that firsthand in my position at ZIM Integrated Shipping Services (ZIM), which has slipped back into the red. The fundamental factors affecting ZIM and GOGL are very different for the two companies, but even so, at GOGL everything can change at any time. There are too many factors surrounding us that cannot be quantified and taken into account in the analysis. That is why investing in shipping is not a very common activity.

Secondly, my conclusions about GOGL being undervalued may be completely wrong – that is, the stock may actually be overvalued. This is especially true if the company fails to meet the new revised upward revenue and EPS consensus estimates over the next few quarters. This is a separate risk actually, but it is related to the valuation.

Your Takeaway

Despite the severity of the above risks, I still believe that GOGL is an excellent choice among bulk carriers due to its narrow specialization in the Capesize niche market, its strong financial metrics, and the revising market expectations leading to undervaluation. I therefore reiterate my Buy rating on the stock.

Good luck with your investments!

")

Q1 2024 Earnings Call Transcript")