")

")

Thesis

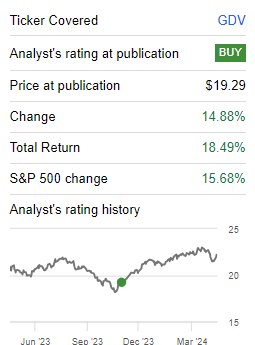

We started covering the Gabelli Dividend & Income Trust (NYSE:GDV) last year, when we argued the fund was getting penalized unfairly for a perceived high financials exposure during the rates melt-up. The call proved to be a very robust one, with the CEF up +18% since, handily outperforming the S&P 500:

Analyst Rating (Seeking Alpha)

CEFs sometimes get good entry points from both a fundamental and structural perspective. This was the case with GDV at the time, when our coverage article highlighted why we thought the fund held less financials than the market expected and why structurally the very high discount to NAV was outside the CEF norms.

The fundamental moniker in finance is ‘buy low, sell high’, and in this article we are going to re-visit the name and highlight for retail investors why the name no longer presents an attractive entry point, but is nonetheless a robust long-term hold.

With yields back at the highs, financials might revisit their HTM portfolios

The dislocation in yields in October 2023 caused market participants to believe financials were in for another March 2023 moment. As a reminder, in March 2023 the U.S. experienced a regional banking crisis driven by unrealized losses in Held to Maturity (‘HTM’) and Available for Sale (‘AFS’) portfolios. These are accounting designations for bond portfolios held by banks for investment income purposes, but which do not get marked to market. The banks, however, need to report the unrealized profit and losses on these portfolios for regulatory reasons.

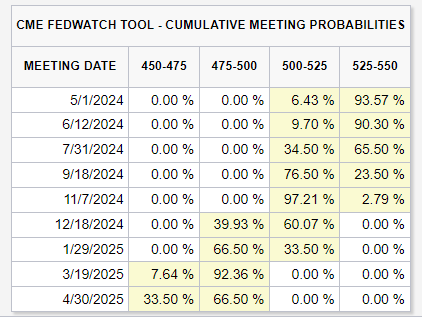

The market has now fully priced out six cuts for the year (where we started in January 2024), and is now looking at only one rate cut late in 2024:

CME Tool (CME)

Things have changed tremendously since this call by Goldman Sachs in January 2024:

Fed Cuts (MoneyWatch)

Higher rates have translated into mathematical losses in respect to long-dated bonds, which have underperformed in 2024. With the Bank Term Funding Program now closed, banks which did not take advantage of it might be liquidity strained again.

We are not advocating for another regional banking crisis, just merely pointing out that with yields back towards 5%, financials do not exhibit attractive entry points anymore. In fact, some names would be best exited. GDV has 15% invested in Financials as a sector.

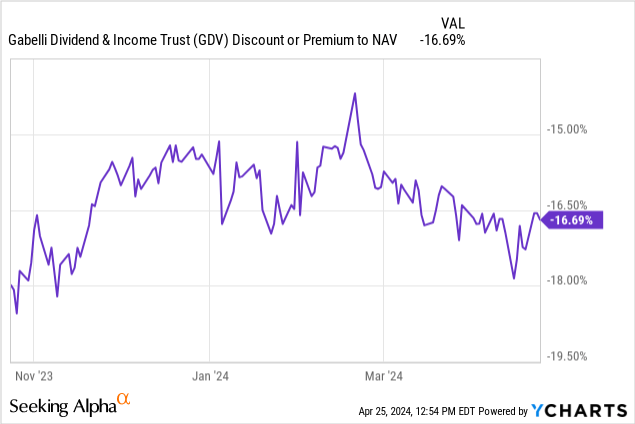

The discount to NAV has narrowed, but not as much as we expected

One structural feature to point out for GDV is its discount to NAV. When we wrote our initial piece, the discount was close to -18%. It has since narrowed, but much less than expected, to -16% only:

Funds with a high beta in their discounts tend to have their discounts move in the same direction as the market. Thus, when the fund pricing goes up, the discount narrows. We can see the CEF experienced something similar up to the bout of weakness that started in April. We think there is more left here in terms of discount narrowing, hence our ‘Hold’ rating for the name. We think we can see -12% to -10% here if the market does not tank overall.

Leverage helps in an up-market

The CEF has a 12% leverage ratio, which helps returns in an up-market. Conversely, in a bear market, the fund tends to do worse. We are on the fence regarding the overall direction for equities in 2024 given the current rally and macroeconomic data. With the GDP data worse than expected today, but inflation higher than consensus, we might be contemplating a potential period of stagflation.

We think the economy has surprised everybody to the upside (including us), and we are not going to bet against America. However, a sustained rally much higher from here is hard to fathom. A range bound market means GDV is a hold, especially in light of a potential further narrowing in its discount to NAV.

Conservatively valued exposure

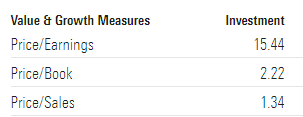

Another reason to keep holding the name here is its portfolio valuation. The fund is long core/value names mostly, thus its blended P/E ratio is significantly lower than the S&P 500:

Valuation Metrics (Morningstar)

The blended P/E for the CEF stands at 15x, versus 20x for the SPY. Similarly, the P/B ratio here is low at 2.2. Valuations do matter, especially for a market that might be toppy.

The top names in the portfolio are large, well-known companies, with a significant presence in Financials:

Top Holdings (Fund Fact Sheet)

We would be much more wary if the top holdings were populated with ‘hot’ AI names which might be subject to significant corrections on the back of market weakness. Not the case here.

When holding a CEF makes sense

While we are advocates for active portfolio management, sometimes holding the name long term also makes sense if there are no signs of over-valuation. GDV is a solid performer, with annualized 10-year returns in excess of 7%.

The fund does not over-distribute via an eye-popping yield, and has managed to utilize its leverage wisely throughout time, having termed out some of the leverage via preferred shares. This structure has helped the fund in a high rate environment, and we actually reviewed the preferred shares for the fund with a Buy rating last year.

GDV is an appropriate equity allocation for a balanced portfolio, and its structural features do not flag an overvalued fund presently.

Conclusion

GDV is an equity CEF. The fund falls in the core Morningstar bucket, and represents a conservatively valued equity exposure. We started covering the name last year when the market was fretting over the CEF’s high Financials exposure. Our ‘Buy’ rating proved to be correct, with a total return on the name exceeding 18% since our rating. With the market significantly higher and consolidating, we no longer find the name to present an attractive entry point. While the discount to NAV has not narrowed to our expectations, the underlying equity holdings have rallied from oversold levels. We do not expect another furious rally in the portfolio names for the rest of the year, but like the name for its conservative equity allocation.

")

")

(NASDAQ:SPT)")