Q1 2024 Earnings Call Transcript")

")

Overview

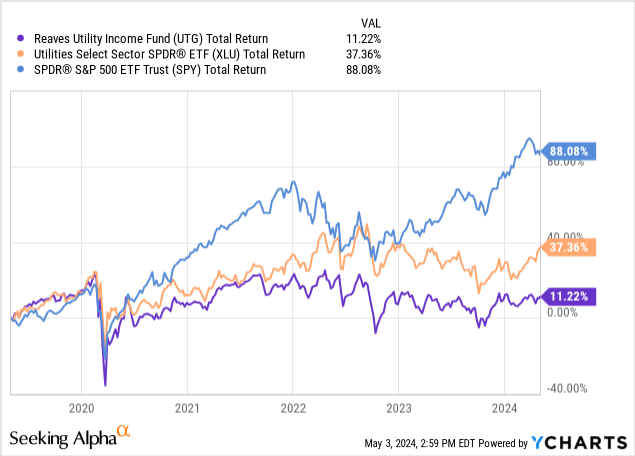

The utilities sector continues to lag behind the rest of the market since the rapid rising of interest rates in 2022. For example, the utilities sector (XLU) has delivered a modest 18% price gain over the last 5 year period. In comparison, the S&P 500 (SPY) has grown in price by over 75% through the same time frame. I believe that receiving a high dividend income even though price movement may disappoint, may help offset this underperformance and make it easier to hold through unfavorable market conditions.

We can see that in a measure of total return, Reaves Utility Income Trust (NYSE:UTG) has outperformed the utility sector by returning 3x through it’s higher distribution rate. At the same time though, UTG also underperforms the SPY but this only serves as a reference point. The main objective of UTG is to provide a sustainable source of income for investors so comparing the total return against the S&P 500 doesn’t really paint the full picture of how UTG is utilized.

For context, Reaves Utility Income Trust operates as a Closed End Fund that provides exposure to the utilities sector and has the main objective to provide high after tax income and total return. The total return is aimed to be mostly comprised of tax advantaged dividend income and capital appreciation which is what makes this a popular choice for retired investors. Retired investors typically aim to invest in funds that can offer some of the following things and UTG manages to deliver:

- A reliable source of dividend income

- Tax advantaged distributions

- Diversified exposure

- Low Cost

- Capital Preservation

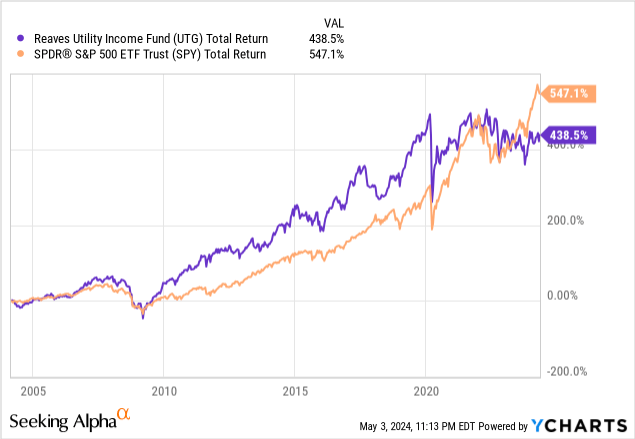

If we zoom out and look at the total return profile, UTG actually had long periods of time where it outperformed the S&P 500. This consistency in total return instills a lot of confidence to maneuver through whatever future headwinds may appear.

[object HTMLElement]

Fund Strategy & Safety

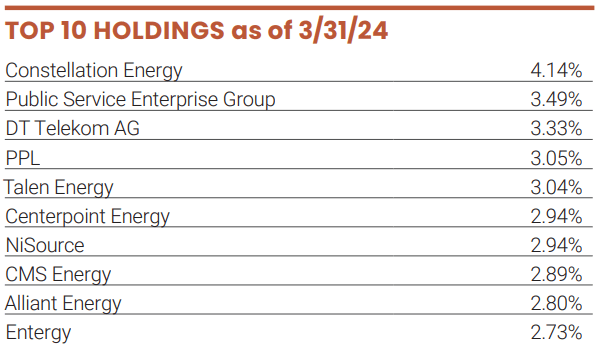

The fund is mostly exposed to stocks within the utilities sector as expected, making up over 58% of the fund. In addition, we do get exposure to Communication Services at 18%, Real Estate at 7.8%, Industrials at 7%, and the Energy at 7.6%. The fund’s strategy is to invest at least 80% of their assets in dividend paying stocks as well as debt instruments within the utility industry. The remaining 20% is invested in all of the other areas previously mentioned. For reference, here are the top ten holdings allocation:

UTG Fact Sheet

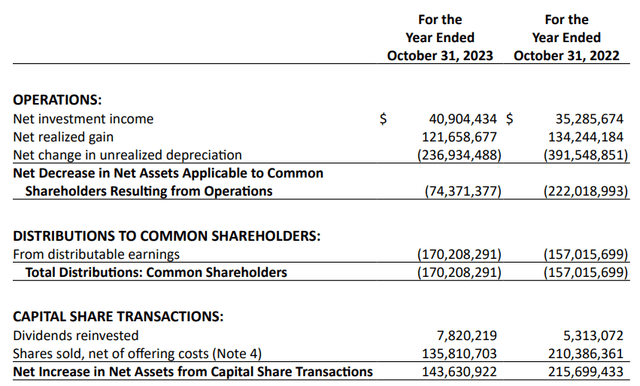

The top ten holdings make up approximately 31% of the funds total value. There are currently about 63 total holdings within the fund. Having no position size larger than 5% of net assets is a great strategy for portfolio allocation as it offsets any sort of concentration risk. This diverse breakdown can be partly responsible for the growth of net investment income for fiscal year 2023. The last annual report was issued in October of 2023, where we can see that net investment income grew from $35.2M in 2022 , up to $40.9M in 2023.

We can see that the net realized gain slightly decreased in 2023, down to $121.6M. While NAV (net asset value) unfortunately decreased for 2023, it still managed to decrease a lot less than the year before. The total net decrease in net assets was -$74.3M, which can be attributed to the utilities sector’s poor performance during the fiscal year. Despite a bad year for the sector, I believe that UTG management did the right thing by reinvesting more dividends than the year before to take advantage of the lower valuations. In addition, they also retain a larger portion of their positions as shares sold, net of offering costs, decreased for fiscal year 2023 down to $135M.

UTG 2023 Annual Report

As a result of the poor performance, the net assets decreased year over year. In 2022 the net assets of the fund ended at $1.99B, compared to 2023’s net asset total of $1.89B. I also noticed that the total distributions out to shareholders were not fully covered in 2023.

- NII = $40,904,434

- Net Realized Gain = $121,658,677Total: $162,566,111

- Minus the distribution total of ($170,208,291)Distribution Shortage: ($7,642,180)

Since the fund has not been able to earn enough to cover the distribution, ROC (return of capital) was likely used to fill in this difference. Compare this to the year before where the distribution amount was fully covered by the NII and realized gains. While ROC may not be favorable for some people, it does help eliminate some of the tax burden as ROC is usually not taxed the same as dividends received.

Vulnerabilities

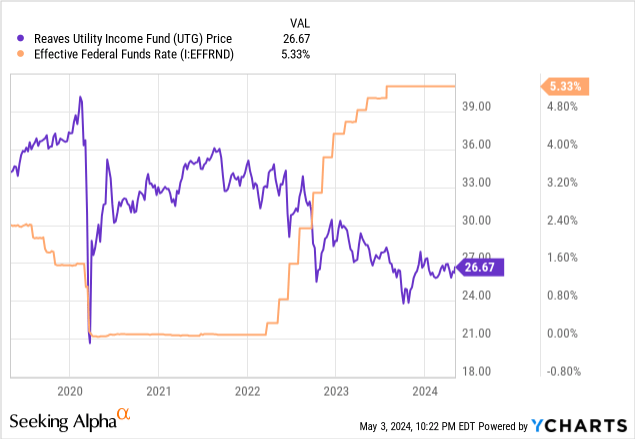

Throughout 2023, utilities was one of the worst performing sectors. This can be attributed to the rapidly rising interest rates starting from 2022. We can see how the rise of interest rates had an inverse relationship on UTG’s price in the graph below. After the initial drop of 2020, the price of UTG started to climb as the sector gained growth momentum from the near zero rate environment.

Utility companies are usually involved in long term growth and development projects that require lots of time and capital. With a higher rate environment, the progress of these can be stalled as they are no longer within budget due to a higher interest payment required on the financed debt. There is always new demand in utilities. For example, I recently wrote an article on Black Hills Corporation (BKH) where I mentioned how the company has ongoing construction projects to create better infrastructures to service a growing population in the Mid-west region of the US but interest rates have slowed progress.

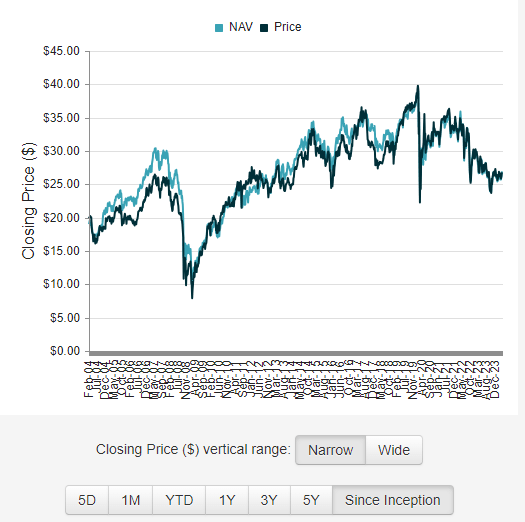

Lastly, while incremental uses of ROC are conveinent and helpful at times, long term use of it is a bit different. Long term use of ROC can have the side effect of eroding NAV and essentially stealing future growth away from the fund. Thankfully, the NAV has managed to continue growing over time so the ROC use here has not been excessive. Taking a look at the chart from CEF Connect, we can see how the NAV remains higher than it was during the fund’s inception period. A general indication that a Closed End Fund is out earning the distribution is whether or not the NAV has grown over time.

CEF Connect

Dividend

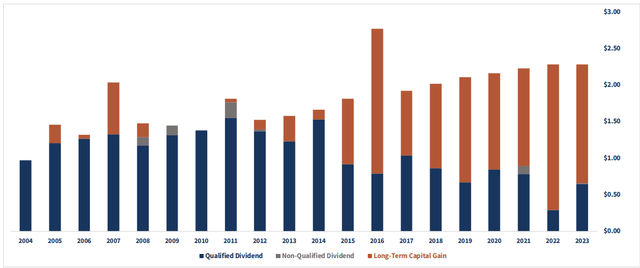

As of the latest declared monthly dividend of $0.19 per share, the current dividend yield sits at 8.6%. As previously mentioned, a huge positive of UTG is that the fund aims to deliver tax advantaged income when possible. This is great because it cuts down on the tax obligation for investor with a large amount of capital deployed. Taking a look at the recent distribution history, we can see that it has mostly consisted of long term capital gains and qualified dividends which are taxed at more favorable rates compared to non-qualified dividends. In 2023, there’s a small slither of gray area which was likely ROC to fill the difference.

UTG Fact Sheet

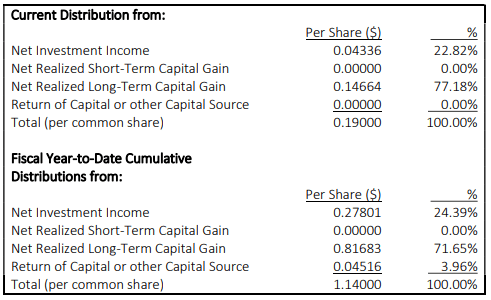

From the latest April Form 19a, it looks like most of the dividend for April was funded from long term capital gains, approximately 77%. The remaining portion was funded from the NII (net investment income), approximately 23%. The year to date earnings look pretty strong as the fiscal YTD earnings sit at $1.14 per share. This means that UTG has essentially earned 6 months of the distribution, in only 4 months time.

($0.19 per share distribution x 6 months = $1.14 per share in total distributions)

This is reassuring from an income perspective as it means that ROC (return of capital) doesn’t need to be implemented since earnings are mostly covering it. However, the year to date distribution total has consisted of 4% ROC during the months where the capital gains and NII may not have been sufficient enough to cover the distribution. The ROC make up is a conveinent filler to make up the difference. Long term use of ROC can be destructive to NAV but with UTG this has not been the case since net assets continue to grow.

UTG April Form19a

Even though the current yield sits high at over 8%, the growth has been surprising. Even though we’ve had a lack of base dividend raises since 2021, the years prior were quite strong. I believe the recently lack of raises has a lot to do with the sectors underperformance as well as higher interest rates. I will touch on the effects of higher rates shortly.

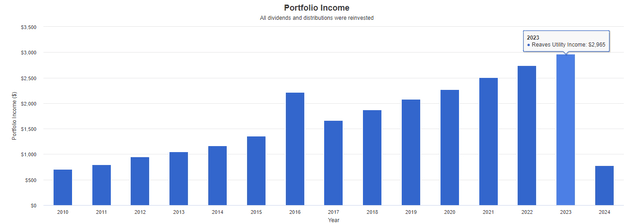

Portfolio Visualizer

The dividend growth here is something that is ideal for investors looking for reliable income as well as growth with minimal effort. Running a back test of UTG’s dividend growth over time shows solid income increases. Assuming an initial investment of $10,000 in 2010, your income would have grown from $702 annually up to nearly $3,000 in 2023. In addition, your position size would ow be over $36,000. This assumes no additional capital was ever deployed after your original investment and dividend were reinvested every month.

Valuation & Outlook

In terms of valuation, the price has remained in a pretty consistent range over the last decade. We’ve rarely seen the price go above $35 per share or below the $25 per share mark over the last ten years. As a result, this has made UTG a pretty predictable stock as far as knowing when may be the best time to enter. For reference, the price is only down -6% over the last ten year period. There have certainly been times where the price has spiked upward and given investors an opportunity to lock in price gains and rebuy at a later date.

Taking a look at the price to NAV (net asset value) history, we can see that the price frequently traded at a discount to NAV between 2014 – 2019. This has changed in the post pandemic era of 2020 – 2024 as the price has now frequently traded near fair value. I am referring to fair value as the cross-point where the price is almost equal to NAV; neither a discount or premium. We can see that the price currently trades at a very slight discount to NAV of -0.11%. In the last 3 year period, the price has traded at an average premium of 0.72%. Based on this, an entry here is slightly more attractive than usual.

CEF Data

While the price sits at an attractive range, I believe that accumulation here would also allow you to take part in the sector’s rebound. If rates get cut in the later part of 2024, I believe that UTG may see some upside. Future rate cuts are a potential catalyst because this would lower the borrowing cost for a lot of utility companies. A lower borrowing cost would enable growth initiatives, potentially fueling more upside as valuations grow from increased operations.

Therefore, I think that UTG’s tax advantaged income can be best utilized at this current cycle of unfavorable market conditions. Accumulation here would enable you to grow a source of dividend income that is rooted in a diverse exposure to utilities. You’d essentially collect a high dividend yield while you await market conditions to improve over time.

Conditions in the market change quite frequently and sometimes unexpectedly. For example, a recent jobs report came in softer than expected and the market reacted to the upside. A slowing job market indicates that the Fed’s rate hikes are starting to slow the economy. As rates start to come back down eventually, you would likely see UTG move to the upside. At which point, you’d now have built yourself a large income stream from UTG and your capital would have also appreciated.

Takeaway

In conclusion, I believe that Reaves Utility Income Trust (UTG) is a great income play to await the turnaround of the utilities sector. While rates remain high, the sector has ben crushed by lower valuations and lower earnings growth. While this also translates into UTG having to implement ROC into their distribution make up at times, it isn’t necessarily a bad thing as long as NAV continues to grow over time. The portfolio within is diversified and valuation sits at a more attractive discount than what has been the normal average over the last three year period. UTG can be a great income play but I also expect some price upside when rates finally start to get cut. Therefore, I rate UTG as a Buy.

")

")