(NASDAQ:SPT)")

As earnings season continues in full swing, volatility is at a year-to-date high as stocks react sharply to earnings news. Unfortunately, while many large caps have succeeded at winning back investors’ trust this quarter, many small caps have faltered dramatically.

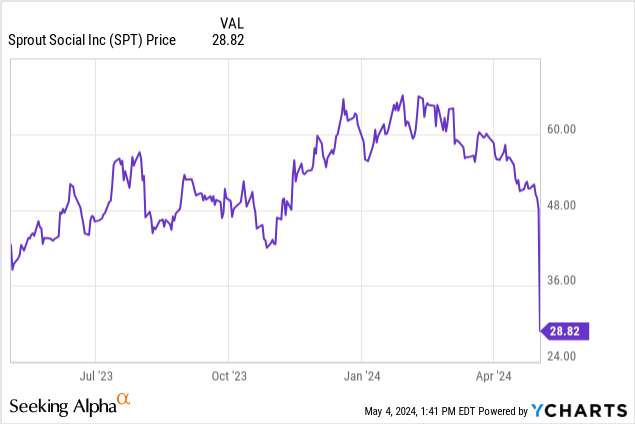

Sprout Social (NASDAQ:SPT) is in this bucket. The social media management software platform dropped more than 40% after reporting Q1 results. These results were accompanied, no less, by a meaningful reduction to current-year guidance as well as news of a CEO transition.

Upgrading Sprout Social to neutral; the bull and bear cases now balance out

I last wrote a bearish note on Sprout Social in February, when the stock was trading closer to $65 per share. I had downgraded the stock at the time based on slowing growth fundamentals and an exceedingly expensive valuation. Now, with slower growth having materialized in Sprout Social’s latest forecast and its valuation having already taken a major beating, I’m more sanguine on the company’s prospects through the remainder of the year and am upgrading Sprout Social back to neutral.

At current share prices, I do see both positives and negatives for this company. Of course, many risks that I was concerned about when I was bearish still remain:

- Companies are cutting back on sales and marketing spend, and social media managers are on the chopping block. Companies are slashing their sales and marketing budgets – both for advertising spend as well as the G&A headcount that supports it. While social media management as a core company function will continue to see secular tailwinds, we’ll likely see retrenchment as companies tighten their belts.

- Lack of execution chops in enterprise sales. Part of what made Sprout Social cut its guidance this quarter was that it acknowledged being unprepared for enterprise buying cycles, despite the fact that it’s now predominantly an enterprise sales company. Execution missteps may further hamper growth rates.

- DIY competition. Sprout Social’s tools are useful but not groundbreaking. Managing social media posts and running analytics on campaign performance can be done with in-house tools, or with more general-purpose competitors like HubSpot (HUBS).

At the same time, however, there are positives to note:

- Large >$50 billion TAM with secular tailwinds. More and more advertising spend is shifting away from traditional formats and into social media. Having a social media strategy is essentially a must in today’s business climate.

- High margin recurring revenue. Nearly 100% of Sprout Social’s revenue base is SaaS, with its customers paying recurring fees to use Sprout Social’s post schedule, monitoring, and analytics tools. This revenue stream also comes at very high gross margins, giving Sprout Social the formula for a profitable software business once it reaches scale.

Guidance cut and slowing growth

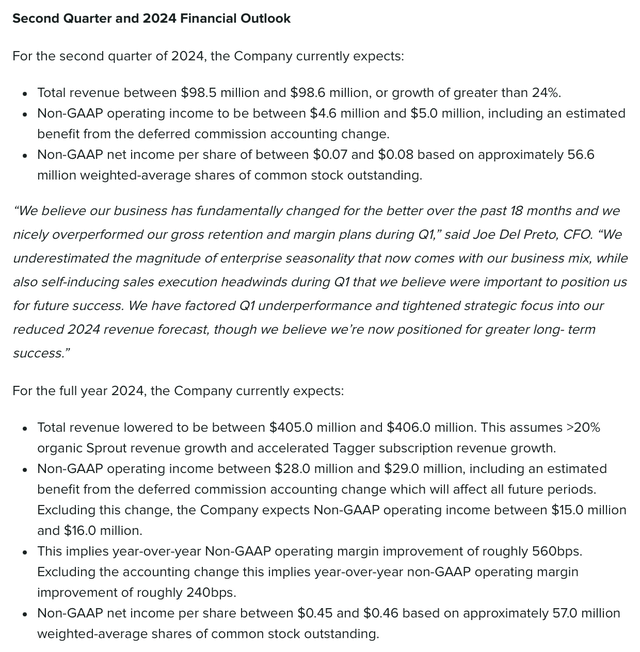

Let’s now address the elephant in the room of why Sprout Social tanked so dramatically after earnings. The company tapered down its guidance forecast for the year to $405-$406 million in revenue, or just 22% y/y growth at the midpoint:

Sprout Social outlook (Sprout Social Q1 earnings release)

Its previous outlook, meanwhile, had called for $425.3-$425.5 million in revenue, or 27% y/y growth.

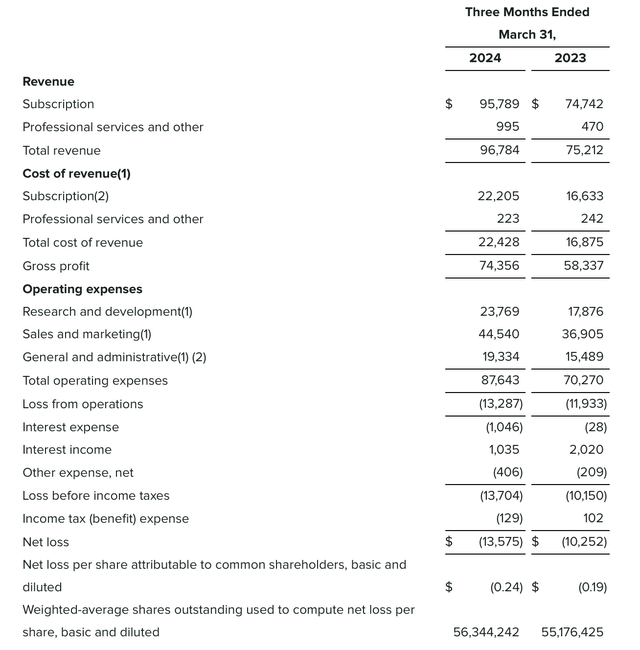

On top of the deep guidance cut, we’ve already started to see large deceleration in Sprout Social’s results. Revenue in the first quarter grew 29% y/y to $96.8 million, which missed Wall Street’s expectations of $97.3 million, as well as decelerating five points sequentially versus 34% y/y growth in Q4.

Sprout Social Q1 results (Sprout Social Q1 earnings release)

Worse yet: while many companies have reported slowing growth, most have done so out of macro pressures or other exogenous circumstances. Sprout Social, however, noted that it was ill-equipped to handle its own growing shift to an enterprise buying base. Per new CEO Ryan Barretto’s remarks on the Q1 earnings call:

We had a strong quarter on many dimensions, but ultimately didn’t meet our revenue goals. After a record back half of 2023, where the majority of our focus was deeply weighted on closing deals versus creating new pipeline, we walked into 2024 with a different business. We’re now enterprise-heavy and the linearity of our business has changed materially, which affects our revenue recognition and planning.

Our months, quarters and years are now more heavily weighted to traditional enterprise buying cycles. We underestimated the magnitude of this shift and the quickly changing dynamics in our customer mix. On top of this, we made several important strategic decisions heading into Q1, such as building new vertical sales teams, accelerating promotions in our midmarket and enterprise teams, adjusting our account coverage model and prioritizing Tagger enablement for all of our customer-facing teams.

We thought we could manage these changes without disruption, but they collectively set us back. I believe each of these moves support our long-term strategy and better positions us for the future, but in the short-term there were execution headwinds that were self-induced. Although Q1 net new revenue added was less than Q1 of last year and not where we expected it to be, there was a lot of important learning, progress and momentum coming out of this process. I own this and fully expect us to be much better going forward.”

Barretto’s elevation to the CEO post, from his prior role as President and head of sales, is a reflection of the company’s need to address these operational challenges.

Still, however, there is hope. The company noted that it grew its qualified pipeline by 37% in Q1. It is also transitioning its sales teams away from smaller, less lucrative accounts to prepare to handle more enterprise deal flow.

Profitability, in addition, is another plus. Pro forma operating income more than tripled to $6.0 million in the quarter, representing a 6% pro forma operating margin, from just 2% in the year-ago quarter.

Valuation and key takeaways

Amid the earnings fiasco, Sprout Social has also fallen to a much more palatable valuation. At current share prices near $29, the company trades at a market cap of $1.63 billion. After we net off the $94.2 million of cash and $45.0 million of debt on the company’s most recent balance sheet, Sprout Social’s resulting enterprise value is $1.58 billion.

Against the company’s latest $405-$406 million guidance outlook for the year, the stock trades at just 3.9x EV/FY24 revenue – when earlier this year, it changed hands at a >8x forward revenue multiple.

I’d say with lower expectations for Sprout Social, we now have a much safer entry opportunity into this stock. I’d wait for earnings volatility to settle, and then jump in with a small trial position.

")

")

")