")

When we last visited with Lantheus Holdings, Inc. (NASDAQ:LNTH) in late February, we stated the stock was undervalued, and the company had a solid outlook. Lantheus Holdings posted its Q1 numbers on Thursday, May 2, and if anything, we might have understated the investment potential of this midcap healthcare name. Therefore, it seems a good time to dive into first quarter results and update our investment thesis around this intriguing healthcare concern.

Seeking Alpha

Company Overview:

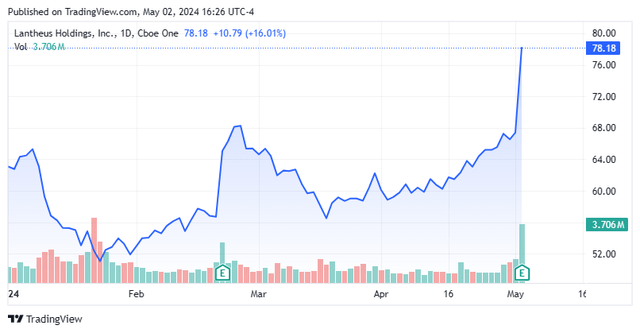

This midcap company (approximate market capitalization of just under $5.4 billion) is focused on developing/commercializing diagnostic and therapeutic products that assist clinicians in the diagnosis and treatment of heart, cancer, and other diseases. Its primary contributor to overall sales is a compound called PYLARIFY. This is an IV injected radioactive diagnostic agent used for positron emission tomography or PET imaging. DEFINITY also contributes meaningfully to overall revenues and is a leading diagnostic ultrasound enhancing agent for patients with suboptimal echocardiograms. With Thursday’s just over 15% rise, the stock trades just over $78.00 a share.

First Quarter Results:

Lantheus Holdings delivered a non-GAAP profit of $1.69 a share, an impressive 15 cents a share over the consensus. Operating income improved to $106.6 million from a $9.3 million loss in 1Q2023. It should be noted that, on a GAAP basis, operating income came in at $155.3 million from $142 million in the same period a year ago. Lantheus produced $119 million in free cash flow in the first quarter. At that run rate and with the stock’s current market cap, that equates to a free cash flow yield in the high single digits.

November Company Presentation

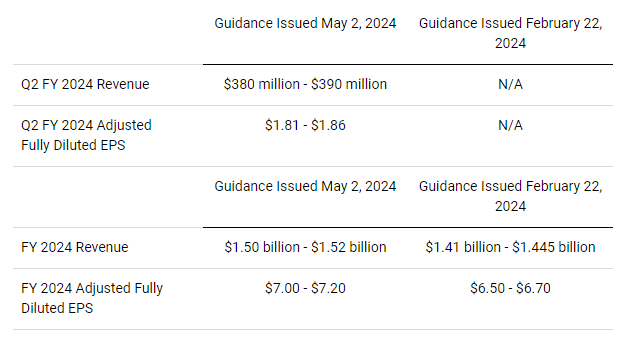

Revenues rose 23% on a year-over-year basis to $370 million, besting expectations by some $20 million. Net product sales of PYLARIFY rose over 32% from the same period a year ago to $258.9 million. Sales growth was the beneficiary of increasing utilization of PSMA PET with PYLARIFY at existing customers, as well as the expansion of the overall PSMA PET imaging market. DEFINITY sales rose just over 11% from the prior period a year ago to $76.6 million. Management upped both FY2024 sales and earnings guidance substantially based on this quarter.

Earnings press release via Seeking Alpha

Finally, the company continues to advance its late-stage candidate PNT2002. This is a PSMA targeted radio-ligand therapy [RLT] targeting the treatment of patients with metastatic castration-resistant prostate cancer (mCRPC). Pluvicto from Novartis (NVS) became the first like therapy approved for this indication last year. Additional and key data from a Phase 3 study should be out in the third quarter of this year for Lantheus.

Updated Conclusion:

Lantheus Holdings had $6.23 a share of profits in FY2023 on $1.3 billion in sales. The current analyst consensus has earnings rising slightly to $6.58 a share in FY2024 on $1.43 billion in sales. They project profits will increase further to $6.67 a share in FY2025 on seven percent sales growth. Based on the first quarter beat and updated guidance, I would expect estimates for both FY2024 and FY2025 will be taken up nicely by analyst firms in coming weeks. I would also expect a few upward price target revisions from these analyst firms as well. Both B Riley Financial ($99 price target) and Leerink Partners ($98 price target) reissued Buy ratings on LNTH in mid-April, it should be noted.

I added to my Lantheus Holdings position in the first half of March as the stock had a decent pullback. I will do the same if given the same opportunity in the months ahead. Even after Thursday’s rise, the stock trades for a bit over 12 times trailing earnings, a deep discount to the overall market multiple. It is somewhat cheaper taken in consideration that Lantheus has just over $700 million in cash and marketable securities on its balance sheet as of the end of the first quarter against approximately $560 million in long-term debt according to its 10-K for the quarter.

In addition, imaging should have few impacts from the slowing economy. Finally, AstraZeneca (AZN) acquired Fusion Pharmaceuticals (FUSN) in March, buoying buyout speculation in the radiopharma space. In short, first quarter results just made the long-term investment case around Lantheus Holdings stronger.

")

")

")

")