Q1 2024 Earnings Call Transcript")

")

Things are getting really interesting when it comes to entertainment giant Paramount Global (NASDAQ:PARAA) (NASDAQ:PARA). Shares have been shooting up and pulling back over the past couple of days as opportunity arises because of a new bid to acquire the business, and as concerns over whether or not that will come to pass mount. At the end of the day, there are billions of dollars’ worth of shareholder value at stake in whatever decision is ultimately made. But I think that, if you frame the situation just right, it becomes clear that the company makes for a very compelling risk to reward opportunity at this moment.

This was the argument that I made when I wrote about the firm in early February of this year. I ended up rating it a ‘buy’ after news broke that Byron Allen, through his firm Allen Media Group, had offered to buy it for $14.3 billion on an enterprise value basis. Since then, a lot has transpired. In addition to coming out with new financial results that show continued improvement on the company’s top and bottom lines, the business has also gotten interest from other suitors, the most recent being what would be a consortium formed by Sony (SONY) and Apollo Global Management (APO) that would reportedly value the company at $26 billion.

Whether or not this transaction or any other transaction will come to fruition is anybody’s guess. What I do know is that we seem to have a favorable risk to reward prospect in front of us. On the one hand, if a deal does get agreed upon, the upside for investors will be tremendous. But even if it doesn’t, it’s difficult to imagine a scenario where shares would fall all that much. The stock looks attractively priced and, while it does still have some issues, it is experiencing continued growth in some key areas. Due to this, I have no choice but to reiterate the ‘buy’ rating I assigned the firm earlier this year.

To deal or not to deal

Perhaps it’s because of the value investment philosophy that has been instilled in me. But I view mergers and acquisitions opportunities from a perspective that is different than most do. Or at least I think I do. The way I view a situation like this is through the lens of whether or not the company is attractively priced, even if the transaction in question fails to come together. If it is something that I would consider buying without the catalyst of being bought out or merged, then I view the downside, at least in the long run, as being minimal. Of course, that’s not my preferred outcome. When I get into a situation like this, my preference is for the stock in question to see a short but significant increase as management agrees to some sort of deal. But we need to be cognizant of the fact that this does not always come to pass.

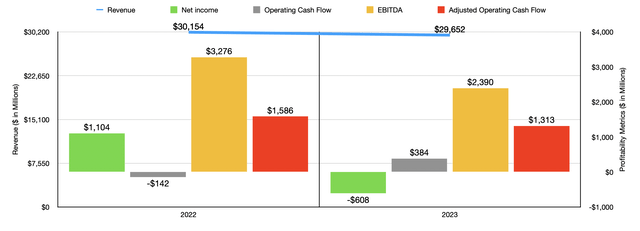

Whether or not a deal involving Paramount Global will occur is incredibly uncertain at this point in time. Although the company has a significant amount of debt, totaling $12.22 billion on a net basis, I don’t believe its financial situation is so bad that it has to have a deal in order for shareholders to do well. Even with that heavy debt load and the interest expense that comes with it, the company generated operating cash flow last year of $384 million. If we adjust for changes in working capital, and strip out amortization of content costs and other related expenses, in order to offset the working capital item involving those same activities, we end up with adjusted operating cash flow of $1.31 billion. Clearly, the company is not hurting all that bad.

Even so, it would be better for everyone in the short run if some sort of transaction does come to fruition. But this doesn’t mean it will. In fact, the market seems to be incredibly uncertain itself about what will happen. On May 2nd, for instance, the Class B shares of the stock, under the PARA ticker, jumped 13.1%. The Class A units, which are identical to the Class B with the exception that they get a vote while the Class B units do not, jumped 21.6%. This move higher was driven by news breaking that Sony and Apollo Global Management, apparently working together, sent a letter to Paramount Global, offering to buy the company in an all-cash deal valued at $26 billion.

As of the close of business on May 3rd, the market capitalization of the two classes of stock together was about $8.98 billion. When we factor in net debt and non-controlling interests, this gets us an enterprise value of $21.65 billion. If management agrees to sell the company for that offered amount, that would imply upside for shareholders, collectively, of 48%. That’s after shares plunged on May 3rd, with the Class A units plunging 14.1% while the Class B units dropped 7%. This move lower was driven by a report by Variety that Shari Redstone, whose company, National Amusements, owns 77.4% of the Class A stock and 9.7% of the Class B stock, allegedly said that she would be unlikely to support a sale to a buyer that was backed by private equity. The fear here is that such a partner in a buyout might ultimately destroy the family’s legacy by breaking up the business and selling off the pieces.

There is another offer on the table. And that is from Skydance, which had proposed to essentially merge with Paramount Global in an all-stock deal valuing Skydance at between $4 billion and $5 billion. As part of the transaction, Skydance would inject $3 billion into Paramount Global in order to pay down debt and would also set aside capital to buy back some stock. But that now seems very unlikely considering that the offer provided by Skydance is supposedly its ‘best and final’ offer and since the one-month exclusive negotiating window between the two sides ended at midnight on May 3rd.

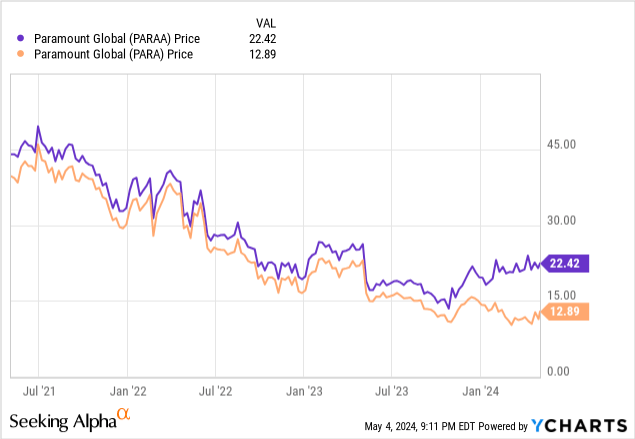

In the event that a transaction does occur, it is unclear how much upside the Class A shareholders would get compared to the Class B shareholders. There has been talk of the Class A shareholders receiving a premium given the voting rights that those units bring to the table. This has created a very interesting scenario as the chart above illustrates. As you can see, over the past three years, both classes of stock have closely followed one another. Obviously, there has been a slight premium for the voting stock. But recently, there has been a widening of the spread between the two. And that seems to be in anticipation of some extra amount provided to those shareholders.

Doing something like a pair trade where you go long one class of stock and short the other could be dangerous in this case. For instance, if you go along the Class A stock and short the Class B stock, you might capture extra upside if the deal goes through. But if the deal falls apart, the spread between those two classes of stock will narrow significantly, with the Class A units falling more than the Class B units would. If you take the opposite approach and go long the Class B stock while shorting the Class A stock, and if the deal for the Class A stock is significantly greater than it would be for the Class B stock, you may not lose a lot of money, but you could lose some.

Author – SEC EDGAR Data

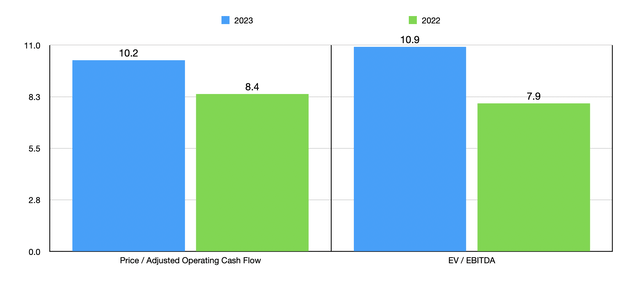

Of course, there are always risks involved in situations like this. But for those who are attracted to the company in general and who don’t mind owning the stock even if the deal falls through, it might just make the most sense to buy the Class B shares and hope for the best. This case could be bolstered by the fact that recent financial performance achieved by management has been encouraging. In the chart above, you can see that the company saw some weakness from 2022 to 2023. But in the chart below, you can see financial performance covering the first quarter of 2024 relative to the first quarter of last year.

Author – SEC EDGAR Data

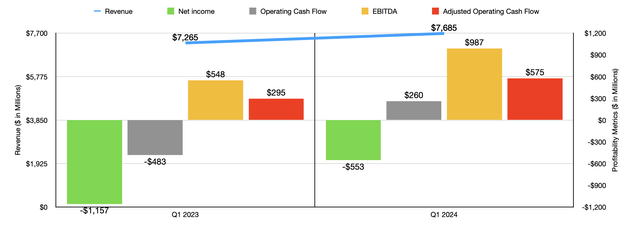

For the first quarter of this year, revenue totaled $7.69 billion. That’s an increase of 5.8% compared to the $7.27 billion reported one year earlier. Management attributed this increase largely to the fact that CBS broadcast Super Bowl LVIII for 2024 but did not for 2023. That contributed an 8 percentage point increase to the firm’s top line on a year over year basis. Digging deeper, it is clear that there are still some weak spots for shareholders to worry about. While advertising revenue jumped roughly 17% year-over-year and affiliate and subscription revenue rose by 6%, licensing and other revenue plunged by approximately 18%, dropping from $1.31 billion to $1.08 billion.

Licensing and other fees largely come from the licensing of rights for other firms to show the television and film content that the company has produced or acquired throughout its life. Unfortunately, the firm suffered on this front because of a lower volume of television licensing in the secondary market. At least some of this pain was driven by a temporary production shutdown caused by both writer and actor strikes last year. But in all likelihood, the continued shift away from cable, not to mention a reduction in the purchase of DVDs and Blu-ray discs, and other older formats, is weighing on the company as well. This is made worse by the fact that the large TV Media segment appears to also be in a state of secular decline, even though the aforementioned Super Bowl boost did help in the short term.

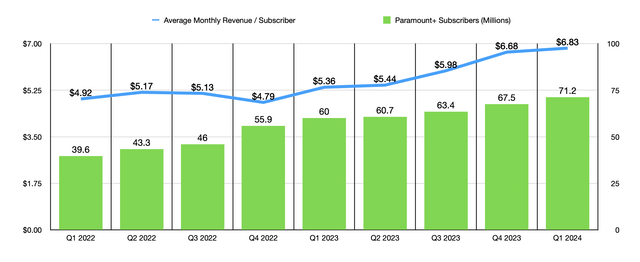

If we ignore that side of the equation, the rest of the company seems to be doing quite well. The part that has me most excited would be its streaming operations. Namely, we are talking about Paramount+. During the first quarter of the 2024 fiscal year, the number of subscribers paying for access to that platform hit 71.2 million. That’s up significantly from the 60 million reported one year earlier. That increase caused revenue associated with those operations to jump 51% from $965 million to $1.46 billion. As the chart below illustrates, the average revenue per subscriber also continues to grow, hitting $6.83 per month. That compares to the $6.68 per month reported just one quarter earlier and it is up from the $5.36 per month reported for the first quarter of 2023. Although this may not seem like much, when using the number of subscribers reported for the first quarter of 2024, the change in average revenue per subscriber from the first quarter of last year to the first quarter of this year would translate to an extra $1.26 billion in sales annually.

Author – SEC EDGAR Data

The rise in revenue for the company also resulted in improved profits and cash flows. Although the company is still generating net losses year after year, the improvement in its net loss from $1.16 billion to $553 million is impressive. Operating cash flow went from negative $483 million to positive $260 million. If we adjust for changes in working capital, we get a rise from $295 million to $575 million. Meanwhile, EBITDA nearly doubled from $548 million to $987 million.

Even if we assume that this increase in revenue and profits is not here to stay and that every year would look like 2023, the picture for the company looks fairly decent. In the chart below, you can see how shares are priced using results from last year and the year before. Those multiples, while not exactly making the company a deep value play, do strike me as fairly attractive. By comparison, rival Netflix (NFLX), which is clearly superior in quality to Paramount Global and deserves a premium because of it, is trading at a price to operating cash flow multiple of 33.3 and at an EV to EBITDA multiple of 30.8. There’s a lot of distance between that multiple and what Paramount Global is going for.

Author – SEC EDGAR Data

Takeaway

I have no idea what is going to happen in the days, weeks, or months to come when it involves Paramount Global and these merger talks. It is entirely possible that no deal will occur. If it does turn out that way, there might be some short-term downside for shareholders of the Class B units. The Class A shareholders could see a bit more pain. On the other hand, the stock does not look unappealing from a long-term perspective. I do understand that while the TV Media segment that makes up the vast majority of the company’s revenue does continue to decline, with that decline certain to remain a problem for shareholders, the growth in streaming, combined with additional opportunities in the Filmed Entertainment portion of the business, means that management can nurse the old legacy operations while focusing on growth for the newer and more stable parts of the firm. For the kind of risk that this entails, the multiples at which the company is trading at seem appropriate. On the other hand, there’s also some chance that a big purchase could come through. And if it does, it would result in nice upside. So irrespective of which situation comes to pass, I have a difficult time imagining the stock turning out poorly.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")