Q1 2024 Earnings Call Transcript")

")

Northwest Pipe Company (NASDAQ:NWPX) is a leading manufacturer of water related infrastructure products including engineered steel pressure pipe and precast and reinforced concrete products.

Northwest Pipe’s products serve markets including water transmission and infrastructure and water and wastewater plant piping.

Northwest Pipe has two segments, an engineered steel pressure pipe segment (otherwise known as “SPP”), and also a precast infrastructure and engineered systems segment (otherwise known as “Precast”).

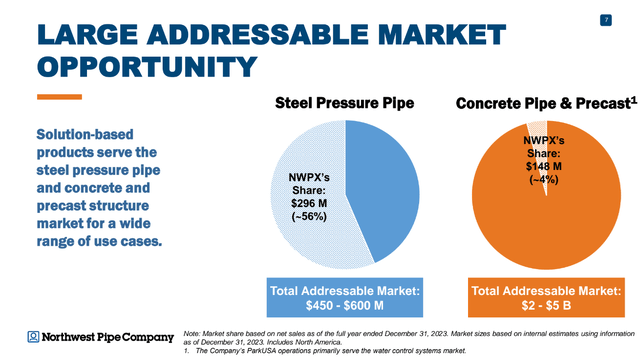

In terms of revenues, Northwest Pipe’s SPP segment has historically been the largest although the company’s Precast segment sales have grown in recent years thanks to acquisitions. In 2023, the company’s SPP sales were $296.4 million and its Precast segment sales were $148 million.

In terms of acquisitions, Northwest Pipe bought Geneva Pipe and Precast for $49.4 million in 2020 as a way to enter the precast related market. In 2021, the company bought ParkUSA for $90.2 million to expand further in that market.

In terms of market share, Northwest Pipe is the leader in the steel pressure pipe market with around 56% share of the total addressable market of between $450-$600 million.

Meanwhile, Northwest Pipe’s market share in concrete pipe & precast market isn’t very big at around 4% but the total addressable market for the segment is considerably larger at $2-$5 billion.

Northwest Pipe Investor Presentation

In the long term, management hopes for its precast related business to grow to a similar size as the SPP business.

On March 4, 2024, Northwest Pipe released 2023 results that indicated weaker year over year financial results and management optimism for 2024. Management, in particular, expects a larger bidding year for its SPP segment in 2024.

2023

For 2023, Northwest Pipe had annual net sales of $444.4 million, down 2.9% year over year.

Gross profit margin was 17.5% for the year, down from 18.8% in 2022.

Net income was $21.1 million, or $2.09 per diluted share, versus $31.1 million and $3.11 per diluted share in 2022.

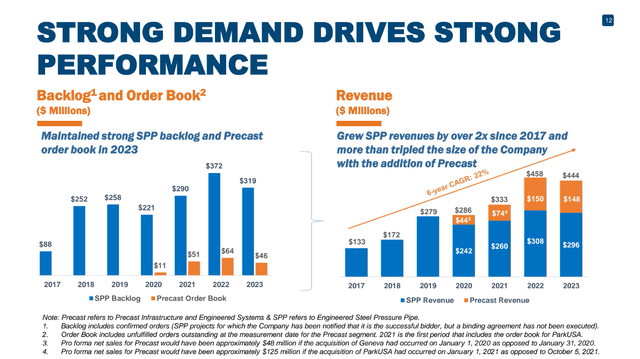

For the SPP segment, revenue declined 3.6% year over year to $296.4 million. SPP gross margin declined by around 20 basis points over 2022 to 14.3%, primarily due to changes in production volume. Backlog including confirmed orders was $319 million at the end of 2023, down from $372 million at the end of 2022 as 2023 was a relatively small bidding year for SPP.

For the Precast segment, net sales declined by 1.4% year over year to $148 million. Precast gross margin decreased around 380 basis points from 2022 to 23.8% due to decreased demand as a result of rising interest rates on commercial construction and residential housing markets and other changes. Precast related order book was $46 million at the end of 2023, down from $64 million at the end of 2022.

Northwest Pipe Investor Presentation

In terms of its balance sheet, Northwest Pipe has a net debt of $158.55 million according to Seeking Alpha and a 2023 net cash provided by operating activities of $53.5 million. As of the end of 2023, the company had $54.5 million of outstanding revolving loan borrowings and additional borrowing capacity of approximately $69 million under the revolving credit facility.

My takeaway is that 2023 was a relatively softer year given headwinds such as higher interest rates that weakened demand in some end markets for the Precast segment and also a relatively small bidding year for the SPP business.

2024

While 2023 was a relatively soft year, management is optimistic for 2024.

For the SPP business, management believes it could be a larger bidding year according to the Q4 2023 earnings call released on March 5, 2024,

The steel pressure pipe backlog, including confirmed orders, was $319 million at the end of December 31, which modestly declined from $335 million at September 30, 2023 and from $372 million as of December 31, 2022.

Our backlog remains elevated by historical standards, even when taking into account the relatively small bidding year we had in 2023. We anticipate a significantly stronger bidding year in 2024.

Management further added,

I’d also like to add that we remain encouraged by the amount of activity we’re seeing on our current and upcoming water transmission projects, as we are currently expecting a larger bidding year in 2024.

In terms of its other segment, management is projecting a strong year for the Precast segment in 2024.

For the year, the Precast segment could benefit from the potential beginning of a decrease in interest rates, which could help the residential and non-residential construction markets. I think interest rates will begin to decrease this year and will normalize within one or two years.

For 2024, management expects free cash flow to range between $19 million and $25 million.

For the future, Northwest Pipe hopes to grow organically and management also remains focused on repaying debt it incurred to finance the 2021 acquisition of ParkUSA in order to position for further acquisitions.

Management believes M&A, specifically in the precast related space, could be another opportunity for growth.

My takeaway is that management generally sees stronger demand for 2024.

Past 2024

Past 2024 and in the long term, management believes its Precast segment is well positioned to grow given the significant level of pent up demand for residential housing and a growing need for infrastructure spending in the United States.

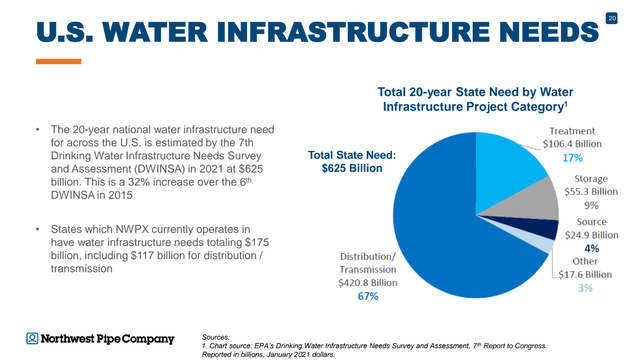

In terms of tailwinds, management notes that there has been substantial underinvestment in water infrastructure over the past several decades. As a result, many aging water and wastewater systems need upgrades, repairs, and replacement. According to the company, the states that Northwest Pipe currently operates in have water infrastructure needs totaling $175 billion, including $117 billion for distribution/transmission.

Northwest Pipe Investor Presentation

In terms of funding, the Infrastructure Investment and Jobs Act has added $55 billion in federal funding for relevant, water infrastructure projects through Fiscal Year 2026.

Risks

Management could make a bad acquisition in M&A.

Northwest Pipe’s margins might not be as strong as expected for various reasons including weaker than expected demand.

Northwest Pipe’s margins and profits could face headwinds if competition increases.

The expected stronger bidding years might not be as strong as expected.

My View

For Northwest Pipe’s SPP business, I think the market isn’t pricing in the potential for larger bidding years in the medium to long term.

With the cost of solar becoming increasingly competitive, the price of electricity could decline substantially in the medium to long term. If the price of electricity declines substantially, water desalination plants could become more economically competitive as they are energy intensive.

With many places in the United States needing more water, I think there’s opportunity for substantial increases in the number of water desalination plants and also correlating substantial increases in demand for water pipes to transport the desalinated water to the areas that need it.

In my view, this could create substantially larger bidding years for Northwest Pipe’s SPP business in the medium to long term.

Although the company will have competition as over 90% of its water transmission projects are secured through completive bid, Northwest Pipe is a leader in the market with larger scale than many of its competitors. If it maintains its market share, I think Northwest Pipe will benefit from larger bidding years for the SPP business in the medium to long term, and as a result, I am bullish on the company.

With that said, if electricity prices don’t decline as expected given various reasons, there could be less demand than expected and my bullish thesis may not materialize.

In terms of estimates as of March 26, analysts on average expect Northwest Pipe to earn $2.31 per share for 2024, $2.79 per share in 2025, $2.71 per share in 2026, $2.75 per share in 2027, and $2.78 per share in 2028 according to Seeking Alpha.

That gives Northwest Pipe a forward PE ratio of 14.82 for 2024, 12.28 for 2025, 12.65 for 2026, 12.47 for 2027, and 12.33 for 2028.

Seeking Alpha

I think Northwest Pipe can meet or exceed analyst EPS estimates for 2024 and 2025 as management sees generally stronger demand in the future than 2023 and the company, in my view, will likely benefit from the potential beginning of decreases in interest rates.

Further in the future, I think Northwest Pipe will have more EPS growth than current average analyst expectations in the 2027 and 2028 given my thesis that potentially lower electricity prices could increase the number of water desalination plants which will likely increase the amount of water transmission projects. This could increase demand for Northwest Pipe’s SPP business.

When incorporating debt, Northwest Pipe has a forward EV/EBITDA of 9.16 versus the sector median of 11.6 and the company’s 5 year average of 8.05. I think paying a slight premium to the 5 year average is worth it given the potential for higher water transmission projects in the future.

In my view, I think Northwest Pipe stock could trade for a forward PE ratio of 15x 2025 EPS estimates given the potential for larger SPP bidding years, which gives me a price target of around $41.85 per share in around a year.

As a result, I rate Northwest Pipe a ‘Buy’ and I would own it in a diversified portfolio with the Magnificent Seven. While I am bullish, I would not be ‘overweight’ on Northwest Pipe given it isn’t a big company with numerous competitive advantages. The margins in the future may not be wide given competition and demand might not be as strong as expected.

In terms of things I would follow, I would follow solar energy prices and see if they continue to trend lower. I would also follow the economical competitiveness of water desalination plants. For the Precast segment, I would follow interest rates.

I think catalysts include earnings results that might indicate larger backlogs.

")

")

")

")