")

")

Approaching 2024, I have assigned Citigroup (NYSE:C) a “Strong Buy” rating, arguing that the bank’s stock is on the brink of appreciable valuation growth due to several key factors:

The bank has lately been making good progress in restructuring its operations, setting up for an expanding cost-to-income ratio going into 2024 and beyond. Moreover, conviction on rate cuts is building confidence on an improving credit environment, with both supportive loan growth and manageable write-downs on the bank’s existent book. In my opinion, this backdrop could drive multiples higher quickly.

Since the thesis has been published, Citigroup shares returned about 24%, outperforming the 10% return of the broader U.S. market by a factor of more than 2x.

Citigroup

Today, I reiterate a very strong buy thesis for Citigroup shares, as I believe that most recent price appreciation has only been the starting shot of a broader, long-dated bull run that could bring Citigroup shares towards a 16-18x P/E ratio, suggesting as much as 60% upside.

The Macro Backdrop Remains Very Bullish

On a broader macro perspective, I am pleased to note that my late-2023 thesis for dovish Fed pivot is playing out as expected. Specifically, I highlight recent developments have reinforced expectations that the Federal Reserve may cut a total of 75 basis points throughout 2024.

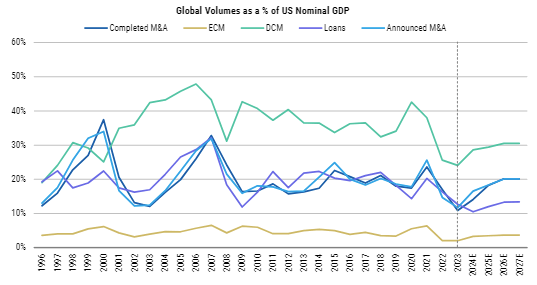

This backdrop, along with an optimistic adjustment in GDP growth predictions, establishes a robust basis for strong banking backdrop. Specifically, this backdrop has the potential to boost momentum in U.S. commercial activities, thus accelerating banking lending and operations. Furthermore, as the transition to a more accommodating monetary policy takes shape, the banking sector seems poised for a period of steadier net interest incomes. In particular, expected Fed funds rates ranging from 4.25% to 4.75% should reduce the costs of borrowing on deposits. Against this environment, I reiterate my expectation that Citigroup’s net interest income for 2024 will be in the range of $49 to $51 billion-clearly above levels seen pre-COVID. Moreover, an environment characterized by strong GDP growth and a dovish monetary stance is expected to reinvigorate the investment banking sector, particularly in Equity Capital Markets (ECM), Debt Capital Markets (DCM), and Mergers & Acquisitions (M&A), areas where Citigroup has significant influence. This expectation is further supported by a recent Morgan Stanley research note, which emphasizes a forecasted surge in investment banking activity (emphasis mine):

We’re bullish on a rebound in capital markets activity, with M&A, ECM, and DCM as a percent of US nominal GDP running near 3-decade lows. We expect activity to inflect sharply this year and build through 2025 and 2026, as pipelines build across investment banking products. Our leading indicators for activity are flashing bright green, with stock markets higher y/y, volatility down, issuance up, credit spreads tighter and CEO confidence rising. In addition to higher investment banking fees, record high stock market levels should drive up market-based revenues in asset management, wealth management and trading.

(Source: Morgan Stanley research note on large-cap banks, dated 20th March: Capital Markets Rebound to Drive Up Money Center SOTP Valuations)

Morgan Stanley

Citigroup’s Fee Income From Investment Banking Divisions Poised For A Sharp Uptick

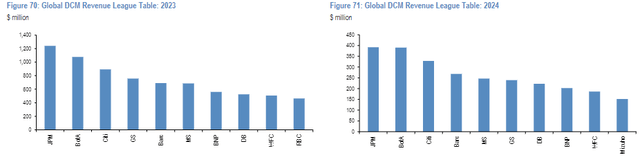

Building on Morgan Stanley’s expectation for an upturn in investment banking activity, I highlight further work by JPMorgan’s research team (Source: JPMorgan research note on investment banks, dated 21st March: Global Investment Bank Tracker). Analysing the first quarter of 2024, JPMorgan analysts predicts that Q1 2024 FICC revenues for major global banks will decrease by approximately 5-6% YoY. While this may seem bearish at first glance, it is actually not: Investors should note that FICC Q1 2024 is benchmarked against an enormously strong Q1 2023, as events surrounding the regional banking crisis pushed up volatility in FICC trading. In Q1, credit sectors have shown resilience, with US business seeing a 13-16% increase YoY in transactions, supported by a tightening in yield spreads. Meanwhile, JPMorgan anticipates a recovery in equity markets, as well as a significant bounce-back in Investment Banking Division revenues, forecasted to increase by around 12% YoY. Within IBD, JPMorgan sees a robust performance in Debt Capital Markets, which is a segment of Citigroup’s core strength.

Looking at the investment banking league table for Q1 2024, it is noteworthy to point out that the thesis of strengthening activity is solid, as well as Citigroup’s performance within the activity. Specifically, I highlight that Citi’s revenue in DCM is running at an annualized topline close to $1,300, vs. $900 million in 2023 (up 40-45% YoY, and the rate cutting has not yet even started!).

JPMorgan equity research

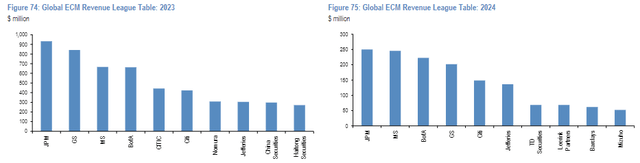

In ECM, Citigroup is running at an annualized topline of $600 million, vs. $450 million in 2023 (up 30-35% YoY)

JPMorgan equity research

Supported by healthy IBD trends, I am now modelling about $28-30 billion of fee income for Citigroup in 2024, on top of the $49-51 billion of net interest income.

Restructuring Is Gaining Steam, With More Upside

On the cost side, Citigroup management is doing some interesting work: Along with its Q4 financial disclosures, the bank announced strong intentions to eliminate approximately 20,000 positions, impacting roughly 8% of its workforce. This, according to management guidance, could lead to annualized costs of up to $1.8 billion in 2024, with a $2.5 billion run-rate by 2026. Furthermore, as part of its restructuring, Citigroup is planning additional layoffs, which will include the departure of 40,000 employees due to its exit from consumer banking operations in Mexico, among others. While Citigroup has not disclosed financial guidance associated with this, analysts currently sees the impact at about $1-2 billion of operative cost savings, according to data collected by Refinitiv. Now, if we apply a 11x implied P/E to the cumulative FWD 2026 savings, then the market capitalization upside of the restructuring could amount to as much as $44 billion. However, since the incremental restructuring cuts have been announced, Citigroup shares have only rerated by about $25-30 billion. Observing that 70% of the rerating was sector-wide, it is reasonable to assume that the incremental rerating dedicated to the restructuring work is less than $10 billion. Moreover, investors should also note that Citigroup is likely not yet done with cuts. In fact, pointing to a conversation with Warren Buffett, Citigroup CEO Jane Fraser suggested that investors should clearly expect more restructuring upside from the bank.

Risk In The Banking Sector Set To Drop Sharply

Despite all this positive backdrop, Citigroup shares trade cheap: Currently, the stock is valued at a P/E of 11x and a P/B of 0.6x. One probable and, in my view, quite likely cause for the cheap valuation stems from the heightened risk associated with banking stocks in general, a sentiment amplified by past banking crises such as the Global Financial Crisis (GFC) and the more recent regional banking crisis. Against this backdrop, I want to emphasize the emerging indications that the revival of the “Fed put” might substantially alter how investors perceive risks in the banking sector. This change could significantly narrow the valuation gap, moving the valuation of banking stocks closer to the typical price multiples observed in the S&P 500.

Recent risk perception of banks was exacerbated by uncertainties regarding the Federal Reserve’s capacity or willingness to provide the same level of support seen in previous crises. This was especially true as the Fed, under Chair Jerome Powell, shifted its focus to price stability over economic growth. However, with inflation currently around 3% yearly and interest rates over 5%, the Federal Reserve is seemingly ready to act as a market backstop in times of economic stress. This assumption is supported by Powell’s recent comments, as for the first time in this monetary cycle, Powell indicated that a sudden increase in unemployment could prompt the Fed to lower interest rates, signifying that:

… an unexpected weakening in the labor market could also warrant a policy response

With the Fed now capable of quickly reducing rates and expanding its balance sheet, there could be significant effects on the performance of financial assets, particularly bank stocks, which historically are more responsive to Fed actions. In my opinion, given the bolstered sentiment from the “Fed put,” Citigroup’s shares are expected to align more closely with the company’s intrinsic strengths as we move into 2024 and beyond.

Valuation Update: Raise TP To $95/ Share

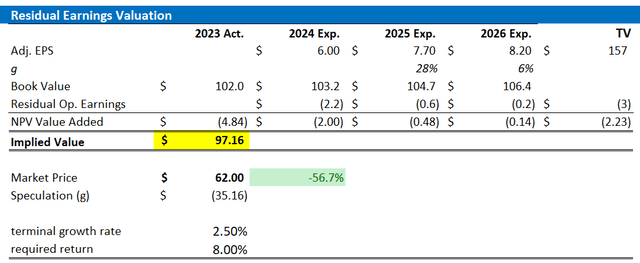

In line with my fundamental view on Citigroup, I am updating my residual earnings model for the bank’s stock: I now project that Citigroup’s earnings in 2024 will range from $5.8 to $6.0 (non-GAAP). For the fiscal years 2025 and 2026, I expect earnings to be $7.9 and $8.4 respectively, with a subsequent average annual growth rate in earnings of 2.25% after fiscal year 2026. For the 2024-2025 growth expectation, I base my starting value for EPS on consensus estimates as collected by Refinitiv. On top of this, I model a 10% uplift on earnings, as I believe analyst consensus is lagging to incorporate the strong IBD momentum that I have discussed earlier. Furthermore, I continue to set my cost of equity assumption at 8.0%. This assumption is primarily based on the Capital Asset Pricing Model, incorporating an adjusted beta of 1.1 relative to the S&P 500 and a long-term risk-free rate between 2.0% and 2.5%, in line with Federal Reserve guidance.

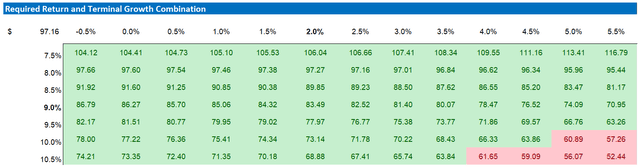

Based on these revised assumptions, I now estimate Citigroup’s fair stock price to be $97.

Refinitiv; Company Financials; Author’s Calculations

Below is also the updated sensitivity table.

Refinitiv; Company Financials; Author’s Calculations

Investor Takeaway

I continue to view Citigroup stock as deeply undervalued and a strong buying opportunity. In my view, the bank has been effectively restructuring its operations, which is expected to lead to an improved cost-to-income ratio in 2024 and beyond. Additionally, growing expectations of rate cuts are fostering optimism for a better credit landscape, supporting potential loan growth as well as a sharp uptick in IBD activity. Given these factors and improved commercial dynamics, I am also updating my valuation model anchored on earnings through 2026, setting a new fair share price at $97 (which is approaching a triple-digit share price valuation).

")

")

")

")