2026-08-05")

The Pernas Portfolio substantially outperformed indexes in Q2 and was up 30% driven by large upswings in holdings: VPG (VPG) +245%, BWEN (BWEN) +112%, XMTR (XMTR) +136%, CEPL (CEPL) +68%, and RELY (RELY) +43%. Q2 was another roller-coaster quarter ultimately ending in de-risking. The S&P 500 rose 15% for the quarter, the Russell rose 22%, and the Dow rose 13%, but those returns conceal how much geopolitical uncertainty markets had to absorb along the way.

The quarter was dominated early by the U.S.–Iran conflict and the risk that a geopolitical shock would become an economic shock through surging oil prices. But businesses and consumers have absorbed higher rates, higher energy prices, and geopolitical stress better than many expected. Earnings were perhaps the real anchor. YoY Q2 earnings growth for the S&P 500 surprised to the upside at 23%, marking the second consecutive quarter of earnings growth above 20%.

The Best Time to Beat the S&P 500 in History

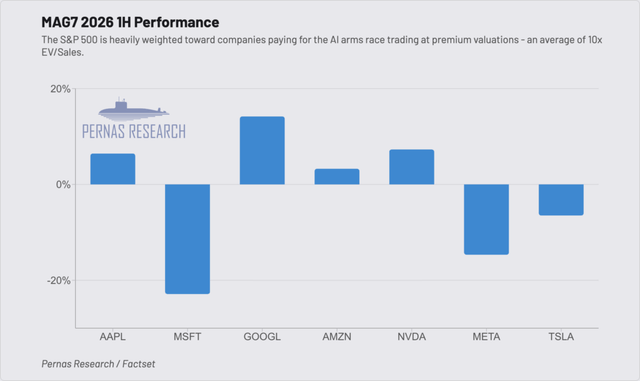

We believe the next several years will be the best environment in modern S&P 500 history for fundamental active managers⁽⁽¹⁾⁾ to beat the index. The setup is extraordinary, and it will likely last only a few years before the index organically corrects for today’s Mag 7 imbalance. The S&P 500 is now highly concentrated in a coterie of richly valued mega-cap technology companies at the exact moment those companies are being forced into an existential AI arms race. The scale of the buildout is becoming so immense that historically cash-rich hyperscalers are starting to dilute shareholders to fund it. Google (GOOGL) recently raised $85 billion through an equity offering to expand its AI infrastructure, while Oracle (ORCL) raised $5 billion of equity with a further $20 billion on the way. This is not to mention the aggressive tapping of debt markets—GOOG, AMZN (AMZN), META (META), ORCL, NVDA (NVDA) & SPCX (SPCX) have issued ~$224B in bonds YTD, already double all of 2025’s $108B⁽⁽²⁾⁾. The largest companies in the index are committing ~all of their free cash flow and more, roughly $750 billion in expected AI-related spending in 2026 (about $150 billion more than expected at the start of the year), to build the infrastructure layer for the next phase of the economy.

This is what makes the moment so unusual. In normal environments, companies tend to be value-maximizing. They optimize for some combination of revenue growth, margins, returns on capital, free cash flow, etc. But in existential environments, survival moves above everything else. When management teams believe that capex or acquisitions improve the odds of surviving the next technology shift, they will spend extraordinary sums, even if the near-term ROI is unclear and even if large amounts of value are destroyed along the way. The risk of falling behind in AI is simply too great.

Some of this investment will create value for the Mag 7. But a great deal of it will also become a productivity subsidy for the rest of the economy. The hyperscalers are funding the data centers, chips, models, power infrastructure, networking, and software layer that countless other companies will use to lower costs, improve products, automate workflows, and expand margins. We expect dispersion within the Mag 7 cohort to remain high as the market tries to discern ROI spend.

We are dubbing this period The Active Investor Opportunity Window:

High Concentration + High MAG7 Multiples + Forced MAG7 Capex + Productivity Spillovers = Index Vulnerability

Investors can find excess returns in smaller companies that benefit from this spending without having to fund all of it. The obvious beneficiaries are the picks-and-shovels businesses supplying power equipment, cooling, networking, data-center infrastructure, components, specialized services, etc. But the opportunity is broader than the direct/indirect infrastructure suppliers. The entire corporate economy is now trying to figure out how to use AI. The next stage of the investment opportunity will come from identifying who can convert this new infrastructure layer into better business economics.

Companies across industries are experimenting with AI in customer service, engineering, sales, marketing, procurement, fraud detection, logistics, software development, compliance, internal workflow automation etc. Uber (UBER) reportedly burned through its entire 2026 AI budget in four months and was forced to cap employee spending on AI tools. Other companies are moving from “tokenmaxxing” to “modelmaxxing, ” learning that encouraging AI usage for its own sake is not a viable strategy. The winners will be the companies that govern usage, optimize model use, measure ROI, and embed AI into workflows where it actually improves productivity.

We expect large dispersion across companies, even companies within the same sub-industry. The reason is that AI adoption is not purely a technology issue. It is also a cultural and operational one. There is historical precedent for this with other general-purpose technologies. In the early decades of electrification, many manufacturers initially believed that the opportunity was simply to replace a central steam engine with a central electric motor. That was only a partial improvement. The true productivity gains came later, when the best manufacturers realized that electricity allowed them to redesign the entire factory. Power no longer had to be distributed through one central engine, shafts, and pulleys. Machines could have their own motors. Factory layouts could be reorganized around production flow rather than power transmission. The technology gained compounding efficacy through organizational redesign.

AI is following the same pattern. Some companies have the culture, management urgency, and operational flexibility to redesign workflows around AI. Our goal is to continue adding these companies to the portfolio as we find them and to keep improving our understanding of each company’s ability to metabolize the technology into actual economics. The question is who can turn AI into faster growth, lower costs, better products, higher margins, and better returns on capital. That is a company-level question, not a sector or industry-level question. Yet another reason why we believe this environment will reward fundamental active managers.

Is the Recent AI Anxiety Rational?

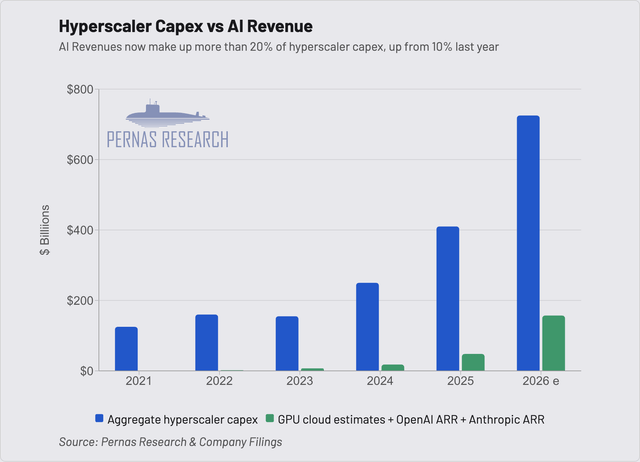

The ultimate return on hyperscaler capex remains uncertain, but the spending is no longer difficult to defend. There is now clear evidence that revenue is accelerating behind the buildout. The open question is whether each layer of the capex stack—chips, data centers, cloud infrastructure, frontier models, applications, and enterprise workflows—will capture enough of the economics to justify the capital being deployed. That question remains unresolved, and it is exactly why we expect dispersion among the funders, suppliers, and adopters. But the chart below shows that revenue accruing to the companies funding the buildout is no longer theoretical. It is compounding quickly.

Today’s revenue is being earned on GPUs that were racked twelve to eighteen months ago. Anthropic (ANTHRO), the leading frontier model company that relies heavily on infrastructure partners, ran from $10 billion to $70 billion in ARR in six months, and rising rents on depreciated hardware like the H100 are the opposite of what oversupply looks like. Meanwhile, bears keep changing their argument: first the models hallucinated too much to be useful, then the frontier labs would never turn a profit, now the models are too expensive for enterprises to adopt.

On top of this, the biggest source of demand is coming into view: agents are coming. A year ago, agents lived mostly in demos. They could not run long without breaking and needing a human to step in. They are now becoming systems that complete real multi-step work with limited supervision. The longer and more independently an agent runs, the more demand is unlocked. Within a year, it is plausible that the number of deployed agents runs from the tens of millions into the hundreds of millions.

The implication is hard to fully grasp because it overturns an assumption baked into nearly every business: that the party on the other side of a transaction, a support ticket, or an API call is human. As economic activity shifts toward agent-to-agent interaction, whole categories of tooling, identity, security, governance, and orchestration will need to be rebuilt. More importantly, agents extend the capex runway. They create a credible path for compute demand to grow far beyond human prompt volume, as software systems begin calling models, tools, APIs, and other agents on behalf of users. That makes it much harder to imagine hyperscalers materially pulling back from the buildout over the next one to two years. If anything, we expect agents to shift the likely range of infrastructure spending towards the high end.

References

*The ”Pernas Portfolio” is a private account managed by Pernas Research LLC. Performance inception date is 01/01/2017. Periods longer than a year are annualized.

(1) By fundamental active managers, we mean managers willing to look meaningfully different from the index and take security-specific risk. Most “active” managers are closet indexers optimizing for career safety.

(2) Trendforce

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

")

")