The latest economic activity data shows that GDP in Q1 2024 grew at a smaller pace than expected. This is directly in contrast with a higher-than-anticipated inflation print, coupled with firm labor market trends. The question now is… where do these unexpected data developments leave the Fed as it readies for its FOMC meeting at the end of April?

While there’s little to prompt any change in policy interest rates, especially now that the passthrough of increased rates into the real economy is becoming clearer, Fedspeak can still change. After all, it started its last FOMC statement by saying “Recent indicators suggest that economic activity has been expanding at a solid pace.” That’s not the case anymore.

Here I take a closer look at what’s really going on with the US economy to assess what to expect from the Fed’s language and also where to invest now.

Slowdown comes knocking

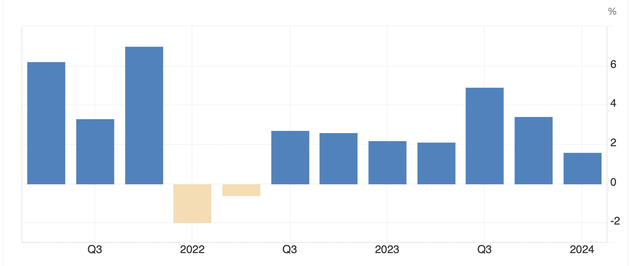

The US economy grew at 1.6% year-on-year (YoY) in Q1 2024, the slowest rate of increase in seven quarters (see chart below). It also came in far below the expectation of 2.3% growth. In fact, the latest figures also undershoot the Fed’s own projection of 2.1% for full-year 2024. As unexpected as this seems, a look at other economic indicators reveals that the growth softening hasn’t happened in isolation.

US GDP Growth, Quarterly, %, YoY (Source: Trading Economics)

Cautionary consumer sentiment

Consider consumer sentiment as an example, which is significant since consumer spending accounts for ~70% of the total GDP. The Conference Board Consumer Confidence Index is cautionary. While the headline index stayed above 100 at 104.7 in March, indicating consumer optimism, the index for future expectations suggests otherwise. It’s at 73.8, from the already low 76.3 in February. This is particularly worrisome since sub-80 levels can signal recessions. Similarly, the University of Michigan Consumer Sentiment Index was also slightly corrected as per the latest survey results.

Muted company sales and outlook

Erratic retail sales data in Q1 2024 is also discouraging, even as it picked up in March. This is also confirmed by the company-level data for some of the consumer stocks I’ve recently covered:

- While Delta Air Lines, Inc. (DAL) revenues are still showing healthy growth, the US Travel Association forecasts a deceleration in travel demand.

- The Hershey Company (HSY) also projects muted revenue growth this year.

- Even demand for premium categories like luxury fashion and wines is weak as evident from the cases of LVMH Moët Hennessy – Louis Vuitton, Société Européenne (OTCPK:LVMUY) and Constellation Brands, Inc. (STZ) respectively.

Elevated inflation and firm labor market

However, other than GDP, the other two data points crucial from the Fed’s perspective – inflation and the labor market – still don’t show convincing enough signs that rates should be cut.

The Fed’s preferred inflation measure, based on the personal consumption expenditure (PCE), has risen by 3.4% in Q1 2024, the highest in a year, while core PCE inflation is up even more by 3.7%. That an elevated inflation figure would be the outcome was already indicated by the CPI inflation figure, which came in at 3.5% YoY in March 2024, the highest in six months.

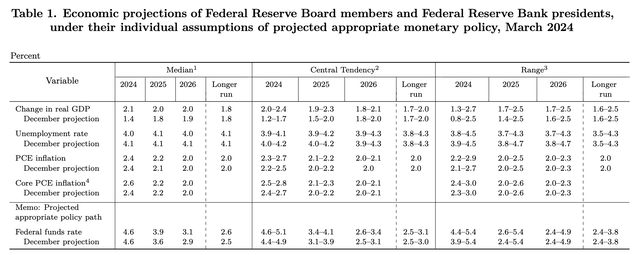

But that’s in no way comforting. Not only are the PCE numbers higher than the Fed’s comfort level of 2%, but they are also higher than the projected rates of 2.4% for PCE inflation and 2.6% for core PCE inflation in 2024 (see table below).

Source: Federal Reserve

The firm labor market also continues to remain stronger than the Fed’s expectations. In March, the unemployment rate was at 3.8%, a 0.1 percentage point decline from the month before. Relatedly, non-farm payrolls rose by 303,000 in March, 31% higher than the 12-month average.

The reserve projects the rate to sustain at 4% from this year onwards for the PCE inflation to eventually subside to 2%. Clearly, the rate is not there yet. In fact, as per the San Francisco Fed’s Philips Curve model, the unemployment rate has to rise even higher to 4.6% for inflation to touch the Fed’s comfort levels. In other words, economic activity hasn’t slowed down convincingly enough so far.

Where to invest now

Whichever we look at the US economy, though, two facts are clear:

- Instead of clarifying, the latest data actually indicates that the path ahead for the US economy is less predictable than expected. This in turn makes it even more likely that the Fed will be in no hurry to change its stance on rates.

- But also the risk of a slowdown is very much real in 2024, and investors should brace for further growth deceleration.

Short-to-medium term buy

Based on this, for at least the short term, if not the medium term, the WisdomTree Floating Rate Treasury Fund ETF (USFR) can still be a good idea to consider. Since the last time I checked on the ETF in October last year, which invests in Treasuries with a maturity period of two years, has seen a steady dividend yield of 5.3%.

Avoid broader indices and cyclicals

On the other hand, the broader stock market had limited short-term upside even earlier based on healthy US GDP growth, as I pointed out in my recent article on the SPDR S&P 500 ETF Trust (SPY). Now there’s the likelihood of a correction in the S&P 500 too.

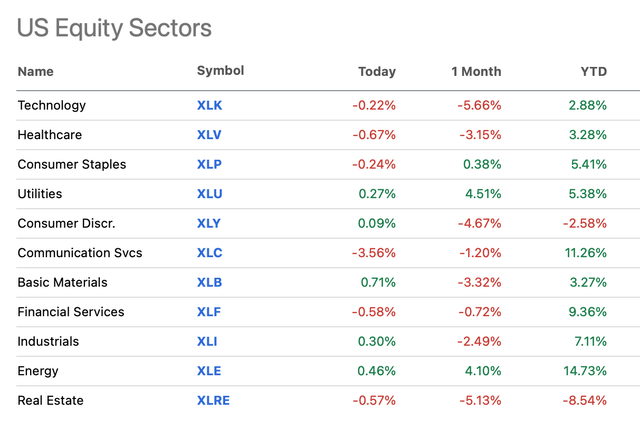

I’m naturally more cautious about cyclicals for this reason too. This also ties in with the examples of consumer discretionary stocks earlier discussed, which are seeing signs of demand softening. It’s no coincidence that year-to-date it’s the only US equity sector besides real estate to see a decline (see table below).

Source: Seeking Alpha

Consider Healthcare

Defensives, on the other hand, look good right now. In the past, I’ve mentioned the VanEck Pharmaceutical ETF (PPH) as one to consider. Despite its correction this month, the ETF, with its largest holdings in big pharmaceutical companies that hold promise in terms of stock market performance, still looks like a good buy.

In sum

The key takeaway here is that while there’s likely to be little change in the Fed’s rate stance, Fedspeak can alter in keeping with the latest GDP print. However, with inflation and labor markets still firm, the tone is likely to remain balanced.

At the same time, it might be a good idea for investors to be more cautious now. ETFs investing in US Treasuries still look attractive, and for the longer term, healthcare continues to be a good choice too. In a change from my previous view though, I do believe that cyclicals once again look riskier, particularly consumer discretionary stocks. In fact, investing even in the S&P 500 is avoidable for now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")