")

")

On our last coverage of Dominion Energy, Inc. (NYSE:D), we looked at the asset sales from the company to Enbridge Inc. (ENB), (ENB:CA). The market was unusually antsy and beat down both the buyer and the seller. Surely the deal could not be bad for both? We actually took the opportunity to upgrade Dominion Energy to a Buy after that drop.

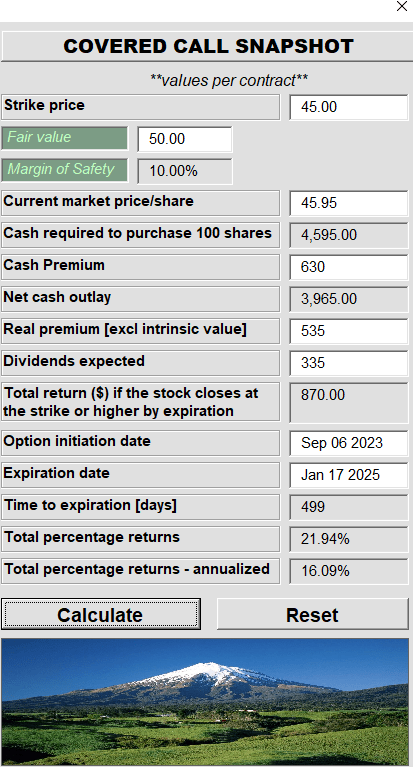

We had a neutral rating on the stock and are upgrading this to a buy as well. As we expect utilities to remain under pressure from interest rate hikes, we would play this defensively using a longer dated covered call for the $45 strike.

Author’s App

That 16% yield for a flattish price is a good deal for this beaten down utility.

Source: Establishing Dominion Over Regulated Utilities

We are about halfway through on that covered call and we are going to tell you why we are moving to a Hold.

1) 2023 Was Worse Than We Expected

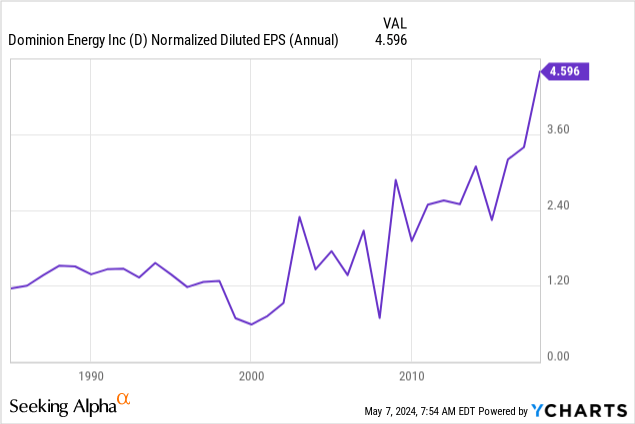

Dominion Energy was running into multiple issues in 2023, but we thought the earnings estimates were sufficiently discounting those problems. Our thesis was presented before the third quarter results for 2023 were out. Have a look at how 2023 shaped up from a year over year perspective.

Seeking Alpha

Total adjusted earnings were at $2.58 a share.

Let’s take a moment to put this number in context. You might remember 2017 the great year when Dominion Energy hit that figure below in adjusted earnings.

It was all too easy for everyone to slap a 22X multiple on that and assume that Dominion Energy will “make you rich”. After all, a utility growing at 10% per year in the era of ZIRP (zero interest rate policy) could certainly be worth 22X earnings. Fast forward to today, and we are now six years from where that chart ends, Dominion Energy is resting on trailing earnings of $2.58. So a 44% contraction over six years instead of growing at a 10% clip. Our bigger point is that, we knew most of this information in September 2023, but still the large misses in the last two quarters were not easy to forgive.

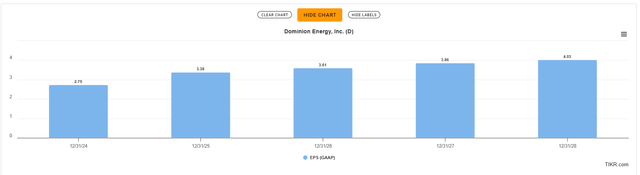

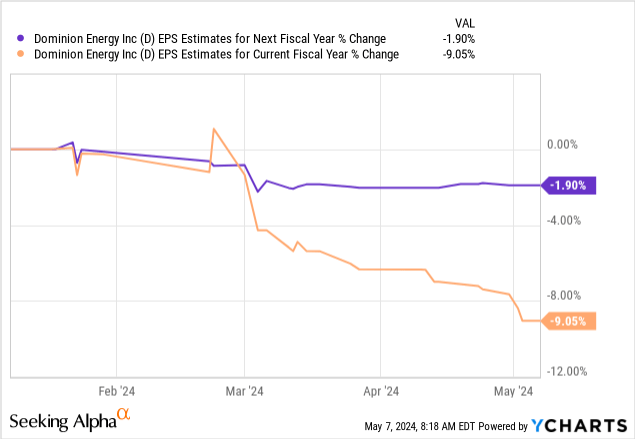

2) The Hockey Stick Ahead Looks Unachievable

The more we look at the recent results, the more we believe that Wall Street numbers are just too delusional. Here are the estimates for the next few years and that big jump from 2024 to 2025 is not going to happen in our view.

TIKR

The assets Dominion Energy (D) has sold will likely cripple the earnings power from 2025 onwards and even the rest is built on optimistic assumptions. In general, you want to buy stocks which have the room to enter an upgrade cycle rather than the other way around. Stocks can go up while earnings estimates are dropping, but it is incredibly rare.

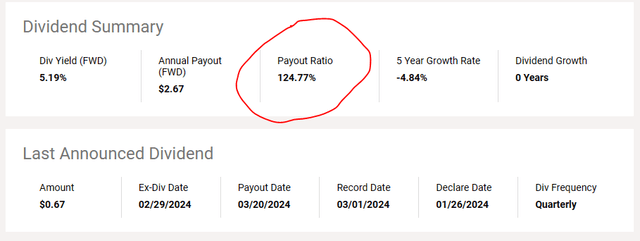

3) The Dividend Could Be Cut, Again

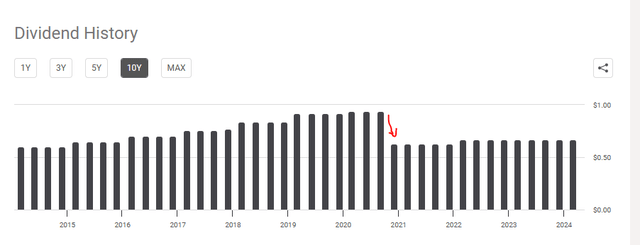

Dominion Energy has a checkered dividend history.

Seeking Alpha

While we can all blame it on the asset sales that it had to execute, the truth is that the company was leveraged to the gills trying to grow way faster than Utilities could grow. We have all forgotten about that cut, but let’s look at where we are today. The current dividend has a payout ratio approaching 125%.

Seeking Alpha

If you combine this with point 2, you can see how things will get rough if Dominion disappoints. Most utilities like to have a sub 60% payout ratio over the very long run. This one is running at 2X that. Even assuming zero dividend growth and the company delivering on both its 2024 and 2025 estimates, the payout ratio only improves to about 80% in 2025. It will be almost 100% in 2024. This is dangerous territory to be sustained, especially if we hit a speed bump in the economy.

Verdict

The 5.2% yield is higher than many other utilities and investors are naturally drawn to it. But safety should always come first and Dominion Energy’s latest disappointments are not encouraging. Earnings estimates for current and next year slowly continue to trend lower.

This is despite some booming consumption trends that we have fired up around the country into some rather worthless endeavors like cryptocurrency mining. Our sense is that this is reflecting continued mediocre execution by the company and the pushing out of expected interest rate cuts. As readers know by now, we are still bullish on inflation and think long term interest rates could surprise on the upside. So we don’t expect this trend (more estimate cuts) to change in the near future. What this comes down to is valuation. We were expecting close to $3.75 in earnings for 2025 around the time of our buy rating. At 12.5X earnings, we were ready to give this a go. The stock has appreciated nicely and earnings estimates have been crushed. At 15.25X 2025 estimates today, we can be far more circumspect. Especially with the potential of a dividend cut. We are now moving this to a Hold.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

")

")

")