to Launch on Uniswap and Immediately List on Multiple Exchanges on May 21")

")

Introduction

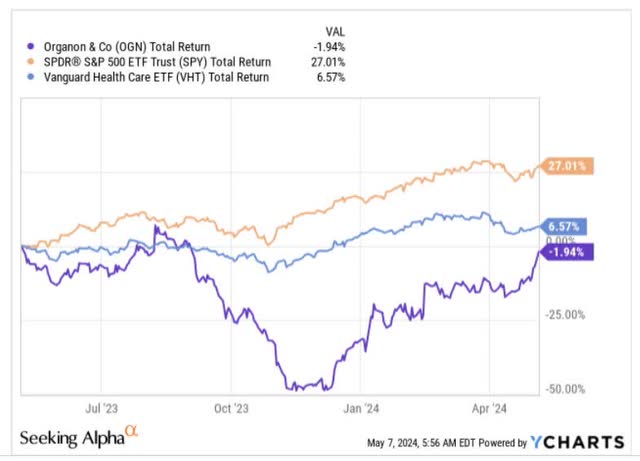

Organon Inc. (NYSE:OGN), is a mid-cap pharmaceutical stock, noted for a portfolio of prescription therapies in the fields of women’s health, biosimilars, and established medicines. Over a one-year time span, OGN’s stock hasn’t made a great deal of progress, losing 2% of its value, and underperforming both its healthcare peers and the prime US equity benchmark.

YCharts

Looking ahead, we suspect OGN will be better positioned to put up a much better return profile, as we see quite a few positive developments. Here are a few reasons why we are optimistic about a reversal in fortunes for OGN stock.

Resilience of Nexplanon

Organon’s Women’s Health portfolio is dominated by the sales of Nexplanon (64% of the portfolio), a flexible single-rod contraceptive implant whose popularity is driven by its relatively low long-term average cost (over a 3-year time span). Recently in January, the company also implemented some price increases which will ensure double-digit constant currency growth of this product through this year (for context in Q1 it grew at 34%). Management has suggested that Nexplanon could hit $1bn of annual sales by next year, and even though there is some consternation over the loss of market exclusivity (in the US, loss of exclusivity will extend until 2027, and outside the US it will expire in 2025), management sought to play down those fears.

Firstly, management sounded confident that they would secure FDA approval to market the product with a 5-year label from 2026; the 5-year label will also give them data exclusivity for three years. Secondly, note that Nexplanon is a removable implant that is pre-loaded into an applicator device which is not easy to conjure under the right safety and efficacy conditions; Note that OGN will still have patent protection on some aspects of this device until 2030.

Leverage Concerns To Abate As FCF Ramps Up

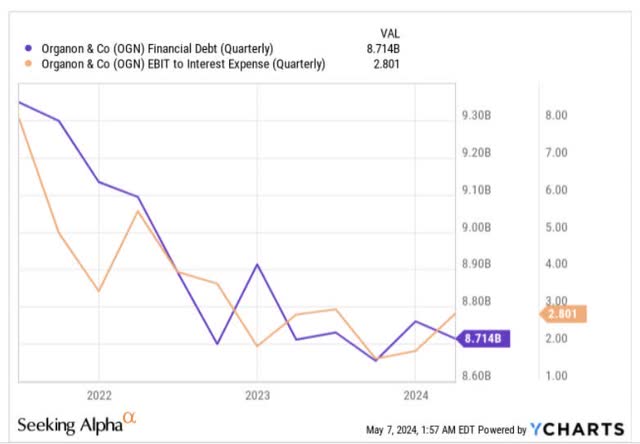

Hitherto, one of the reasons why OGN may not have attracted too many bulls is that it is quite highly financially geared at around 4.1x net debt to EBITDA (as of Q1-23). This has put a spanner in the works of further M&A/R&D collaboration momentum and also prevented the firm from growing its dividend.

Having said that, it’s not as though OGN’s leverage position has been worsening over time. Rather, note that it has been able to bring down its level of gross debt from levels of over $9bn over time, and over the last couple of quarters, we’ve also seen the interest coverage weakness bottom out and reverse.

YCharts

Going forward, OGN looks well set to bring the leverage down to less than 4x by the current year, and to 3.5x by the end of next year, because FCF generation has been progressing quite nicely, and will only get better from here.

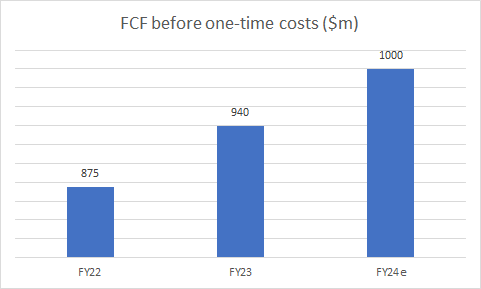

If one only looks at absolute FCF, one may not get a true measure of progress as OGN is still facing a lot of one-time costs linked to the Merck spin-off. For instance, in the recently concluded Q1, it only saw a positive FCF of $6m, but if one accounts for one-time spin-related costs, FCF could have been $74m. If one looks at OGN’s FCF progress over the years, without these one-time costs, the picture looks a lot healthier. Note that after growing at 7% last year, FCF ex-one-time costs in FY24 are poised to grow by another 6% this year and cross the $1bn landmark (do also consider that traditionally, Q1 has also been the weakest FCF quarter on account of incentive payments, so there should be some improvements here all the way through Q4).

Earnings transcript

Also note that with the passage of time, the impact of these one-time costs will fade, and by FY25, it will only be marginal; for instance, this year alone, those costs are expected to drop-off by 40% YoY.

Ongoing Cost Containment Measures Not Yet Felt On the Valuation Front

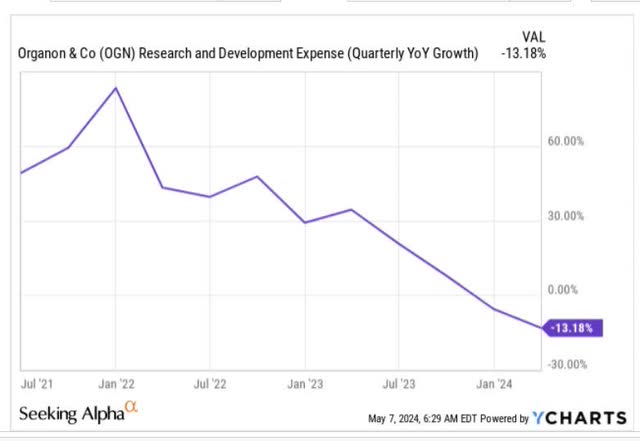

The R&D function is a vital cog of most pharmaceutical firms, but it also needs to be noted that in the case of OGN, its priorities don’t lie in the areas of in-house discovery and early research. Rather OGN typically goes about filling these early-stage gaps through M&A, partnerships, etc. In recent quarters, management has been getting, even more, laser focused on trimming and optimising their R&D function

YCharts

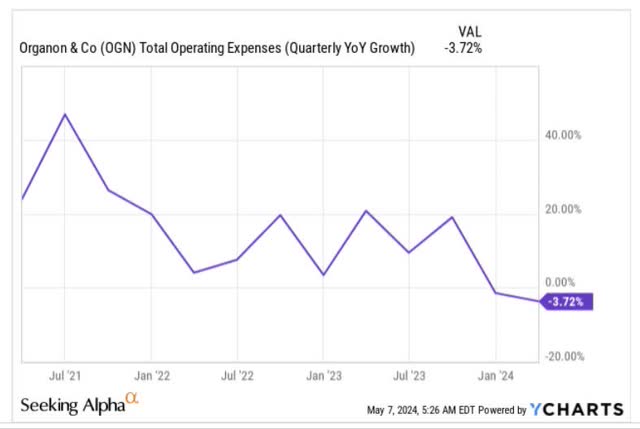

Note that R&D expenses, which were growing at a pace of 30-60% a few years back, have now been dropping by double-digit percentages over the past few quarters. Besides R&D, headcount attrition is also taking place in other avenues, and by the end of this year management is targeting a 5% drop in the headcount. Note also that the company’s overall OPEX has now started declining on a YoY basis.

YCharts

Given the ongoing improvements on the cost base, you’re looking at fairly healthy bottom line growth of 11-12% for the year, based on the implied FY24 EPS consensus of $4.449.

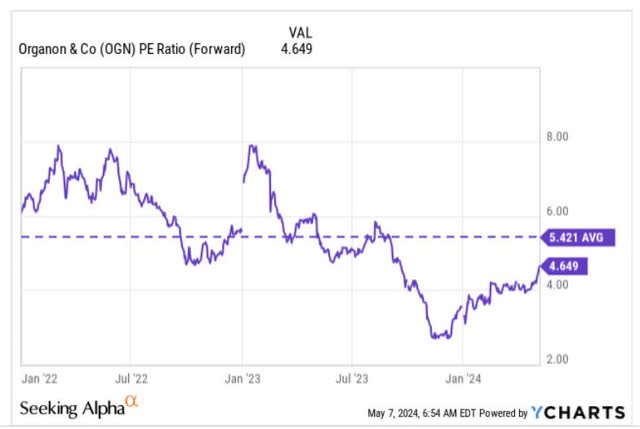

YCharts

When you have a business that is on course to deliver double-digit earnings growth, it feels discordant to note that it is priced at a miserly forward P/E of just 4.6x, as that translates to an attractive PEG (Price to earnings growth) ratio of just 0.4x. Note also that the current P/E represents a 14% discount to the stock’s long-term average, which makes it an even more attractive proposition.

YCharts

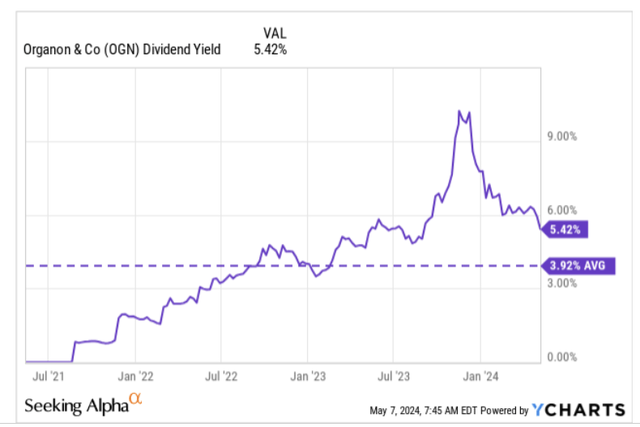

Then, even though the dividend hasn’t been growing, you still get to pocket a very tasty yield of over 5%, which is still around 150bps more than what you normally get.

YCharts

Closing Thoughts- Encouraging Chart Developments and Good Rotational Prospects

Our bullish stance on OGN stock is further emboldened by the recent developments on the charts. The image below captures the stock’s weekly movements over the past two years, and what’s evident is that it has taken place within the area of the two black downward-sloping trendlines, or a descending channel.

A breakout from this channel, or the upper trendline looked rather imminent, as since February we’ve seen some sideways price buildup just near the channel boundary. In April we finally saw the stock breakout from its 2-year long channel, marking a significant technical event.

Investing

The bullish conditions can be further validated by what’s seen on the daily chart, with the stock now trading above both its key moving averages- the 50DMA and the 200DMA. Crucially, we also saw the golden cross pattern play out a few weeks back, with the 50DMA crossing over the 200DMA for the first time since August 2022.

Investing

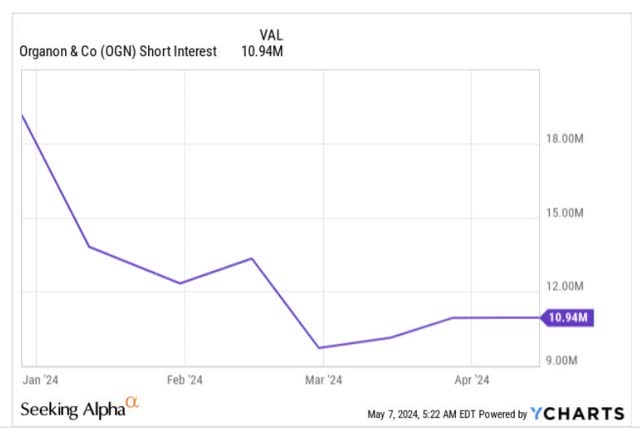

Note that whilst these bullish triggers are taking place, the short-sellers do appear to be running for cover. The number of shares that are sold short has almost halved from what was seen at the start of the year, and still with another 10-11m shares to go, don’t be surprised to see the stock benefit from further short covering momentum.

YCharts

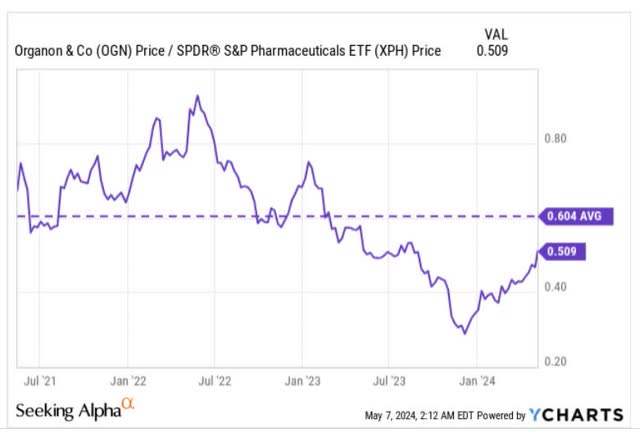

Rotational specialists who focus on the pharmaceutical space could continue to pile on OGN, as its relative strength ratio versus other pharma options is still rather low by historical standards. To expand on this, note that the current RS ratio is roughly 15% lower than its long-term average, and still offers scope for mean-reversion.

YCharts

")

")

")