")

")

Investment Thesis

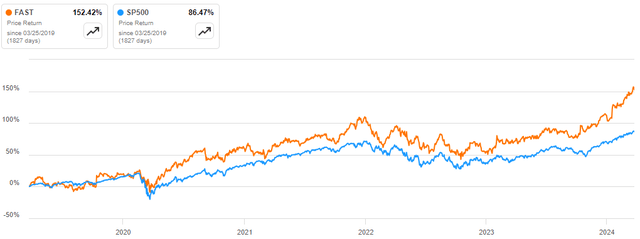

Fastenal Company (NASDAQ:FAST) stock has soared more than 152% over the last five beating the S&P 500 by a margin of about 66%.

Seeking Alpha

Following this solid upward trajectory, this stock is currently trading at a premium something which rules it out as a good value investment. However, the company has a bright future courtesy of its robust business model and cost-control measures which I believe will keep fueling growth. From a dividend standpoint, FAST is a good dividend choice based on its growth history and consistency. Lastly, from a technical point of view, this stock has been on a solid upward trajectory which is about to reverse. Given this background, I believe this stock is a hold for value investors as we wait for a trend reversal or a pullback. For dividend investors, if you’re comfortable paying a premium price for a great dividend stock you can consider FAST.

Company Overview

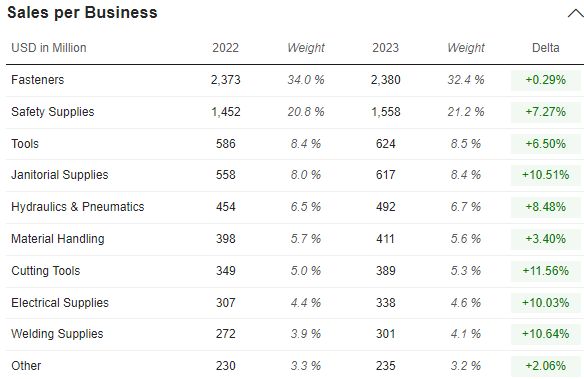

FAST is a global wholesale distributor of industrial and construction supplies. It offers a diverse range of products including fasteners and related industrial products. Its commitment to investing in its customers through technology and end-to-end supply chain management in my view positions them in a competitive place. Below is the company’s diverse product range and respective sales contribution.

Market Screener

From this data, it is clear that this company has diversified revenue streams with none of its business segments contributing more than 34% of revenue in 20222 and 2023 FY. From where I stand, this diversity is very essential because it ensures that this company is generating its revenue from different end markets which cushions them from significant financial crisis in case of a market downturn if they were focusing on one end market. Secondly, the company doesn’t over-rely on one product line for a majority of its revenue and therefore this has ensured an effective distribution of risk in case one of its product lines fails or experiences severe competition.

Further, FAST operates in different geographical regions enabling it to capitalize on different economic zones something which adds to its diversity. However, the majority of its revenue accrues in the US and this means that any significant changes in its US market would have an equivalent impact on its performance.

Market Screener

MRQ Performance

In Q4 2023 dated January 18th, 2024 FAST reported what I would term a strong quarterly performance whose highlights are as follows. First off, net sales came in at $1.76 billion representing a YoY growth of 3.7% with daily sales growing by 3.7% a reflection of higher unit sales majorly at the new Onsite locations. In addition, its gross profit rose by 4% to $799.4 million with its operating income growing by 6.3% to about $354 million. Net earnings grew by 8.5% to about $266 million with its diluted net EPS increasing by 8.4% to $0.46 and beating expectations by $0.01 according to Seeking Alpha. Interestingly, the company was able to convert this growth into cash, reporting an operating cash flow of $354 million marking a YoY growth of 17.3%. Its operating cash flow was about 132.9% of its net income.

This impressive performance was impacted positively by modest product pricing and stability in price levels throughout the quarter. Foreign exchange also played a part in impacting sales by about 10 bps. In general, the company’s performance is a demonstration of its strategic acumen and commitment to growth, and efficiency. I believe so given the apparent growth both in the top and bottom lines. Further, the growing profit margins clearly show the company’s ability to manage cost hence efficiency. More details on these takeaways from the quarterly performance will be provided in the succeeding section.

Growth Catalysts: Robust Business Model And Cost Control

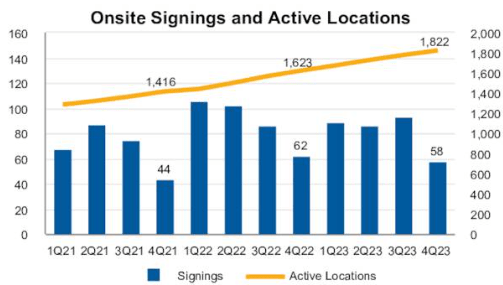

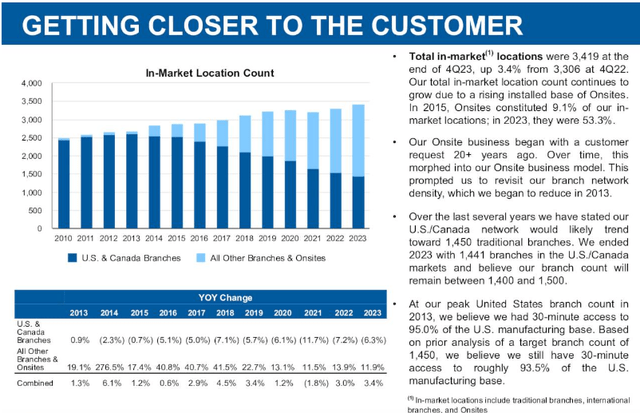

As mentioned in the previous section, the company’s MRQ performance illustrates the company’s strategic acumen seen in its improved business model and its commitment to efficient resource utilization. Let’s dive deeper here. To begin with, is the company’s strong business model. FAST strengthened its business model through the expansion of its Onsite locations and the inclusion and growth of larger customers. In Q4 2023, the company signed 58 Onsites and they ended the quarter with 1,822 active sites a growth of 12.3% from Q4 2022. For the entire year 2023, FAST signed 326 Onsites and their 2024 goal is between 375-400 locations.

FAST Q4 2023 Presentation

While the company is growing its onsite locations and larger customers, it is even making it better by eyeing customer convenience through getting closer to its customers. In my view, this improving convenience will translate to improved customer satisfaction hence a loyal and growing customer base which will be crucial in the company’s growth trajectory.

FAST Q4 2023 Presentation

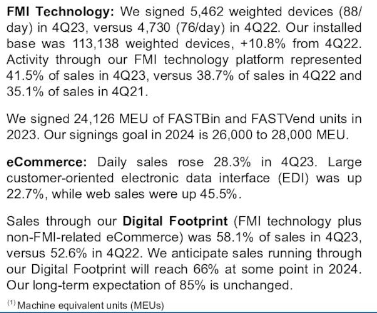

The other growth catalyst is the digital strategy. FAST has adopted digitization which I see as a major growth catalyst. Its digitization has enhanced the company’s market presence as well as customer engagement. Just to highlight how digitization has impacted the company’s performance, in Q4 2023, daily e-commerce sales increased by 28.3% YoY. Its FMI technology on the other hand represented 41.5% of sales compared to 38.7% in Q4 2022. Sales of the entire digital footprint represented 58.1% of total sales in Q4 2023 compared to 52.6% in Q4 2022. The company is projecting to achieve 66% of digital sales in 2024 and about 85% in the long run. Looking at these numbers, I see a bright future because it is apparent that the company’s digitization is paying off.

FAST Q4 2023 Presentation

Lastly is the company’s efficiency measures. FAST is actively adopting strategic measures to contain costs, especially product and transportation expenses. The measures in place to achieve efficiency include warehouse automation, delivery efficiency through the trucking network, and selling more of the high-margin products to improve returns. The cost control measures appear to have started yielding given that the gross margin improved by 20bps in the MRQ to 45.5% and that operating expenses as a percentage of revenue decreased to 25.3% from 25.7%. In my view, should the company keep implementing its control measures effectively, then I am optimistic that margins will keep improving in the future.

Given the FAST growth catalysts, I have a bright outlook for this company’s top and bottom lines. The company’s improving efficiency ratios lend credence to my optimism, especially given the company’s expectations to keep investing in growth areas such as technology and Onsites.

FAST Q4 2023 Presentation

Why I’m Banking On The Onsite Model And Digitization

While I have highlighted that the Onsite business model and digitization are major long-term growth drivers and provided the MRQ contributions of each of them, here are my thoughts on why exactly I believe they will keep delivering. Let’s begin with the Onsite business model. In this model, I find several benefits which I believe serve as competitive advantages. The first one is customization. It should be noted that the shift from the traditional model to the new model was aimed at providing more customized products and the focus was to fulfill the daily needs of its customers. By so doing, the company can offer tailored products to meet specific customer needs in each onsite facility hence improving customer satisfaction. A good example of this tailored product is its custom fasteners.

The other advantage of this model is aggregation. As mentioned earlier, this new model offers tailored products and services. This implies that the company offers all the products its target market needs at the vending center. In other words, it offers a one-stop solution that saves customers’ transaction costs as well as improving convenience.

The other benefit is innovation. Through the new model, FAST has been able to adopt new technologies such as automated supplies, IoT, and data analytics. Through these new technologies, the company has been able to achieve higher efficiencies as evidenced by the low operating costs even at a time when inflation was historically high among other benefits. Besides the adoption of new technologies, the new model has enabled the company to be innovative by adopting the Vending program something which has enabled them to customize inventory hence improving its distribution by meeting a more diverse and unique product by getting closer to the customers.

In summary, the onsite business model has several competitive advantages which are helping the company to improve customer satisfaction, improve its distribution, and improve its efficiencies something I expect to drive the long-term success of this model.

The second aspect is digitization. For digitization, besides enhancing sales channels which is demonstrated by the substantial growth in digital sales as illustrated in the previous sales, it is also playing other roles that will see this company achieve long-term and sustainable growth. Firstly, it is improving the company’s operational efficiencies. Through the adoption of digital channels, FAST can improve its product visibility, especially through e-commerce. Further through its tracking system, the company has improved its product traceability therefore reducing risks in shipment and creating ordering and fulfillment efficiencies.

Secondly, the adoption of technology is improving customer flexibility. The company is offering its customers several avenues to make their orders such as self-service web shops and vending machines. This flexibility alludes to convenience depending on customers’ preferences.

Lastly is data utilization. There is no doubt decision-making based on empirical data is more accurate. For this reason, I am made to believe that FAST uses the data in its digital platforms to make informed decisions. For instance, I believe in customizing its products to meet specific needs, it relies on its sales data to identify which products should go to which target market therefore achieving a higher degree of accurate distribution and supplies.

Following the adoption of this model and digitization, FAST has been characterized by consistent growth both in its top and bottom lines with both profit and revenues growing consistently in different time horizons as shown below.

Seekig Alpha

From this data one feature of the company’s business model is clear, and that is resilience. Over the last couple of years, there have been several hurdles such as the Covid 19, the Ukraine war, and inflationary pressure. Despite these adversities, FAST has been able to withstand the rough seas and registered growth both in its revenues and profits something which affirms how resilient its business model is. The most attractive part of this model which I believe summaries all its advantages and benefits and this is where my future optimism stems is its scalability without incurring significant additional costs.

To put this in perspective, the company has grown its Onsites from 1114 in 2019 to 1822 in 2023 marking a growth rate of 63.6%. In the same time frame, it has grown its revenue from $9.3 billion to 14.3 billion marking a growth rate of 53.5%. Most interestingly it has reduced its total cost as a percentage of revenue from 16.03% in 2019 to 13.66% in 2023. This not only shows this business model is scalable but also it’s scalable while achieving better operational efficiencies. For this reason, I expect the projected expansion plans to grow the company’s revenues and profit margins while reducing the operation expenses as a percentage of revenue.

Dividend

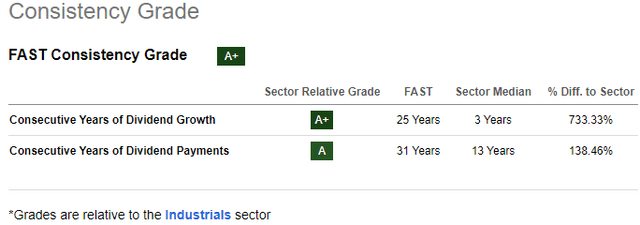

Based on several parameters, I find FAST to be a great dividend stock. To begin with, the company has paid dividends for 31 consecutive years compared to the sector median of 13 years and it has grown its dividend for 25 consecutive years compared to the sector median of 3 years. Given this background, there is no doubt that FAST is a reliable and consistent income generator.

Seeking Alpha

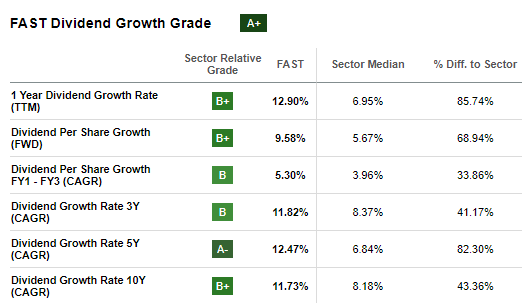

It is even more interesting to look at the growth history in different time horizons. Using this approach FAST is undoubtedly a dividend growth machine especially when compared to the sector medians.

Seeking Alpha

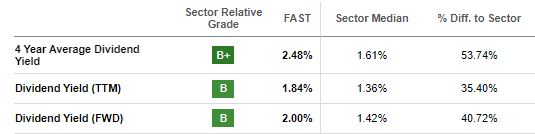

Further, considering the dividend yield, this stock is attractive with its 4-year average, tailing and forward dividend yields being above the sector medians by double digits percentage.

Seeking Alpha

While its growth, consistency, and yield are attractive, its sustainability is the other most important aspect. With a dividend payout ratio of 69.31%, I find this dividend to be sustainable because it is adequately covered by earnings.

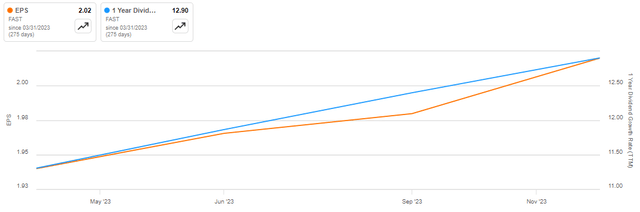

Lastly are my expectations on the dividend in the future. Looking at the dividend trends, it appears that the company’s dividend has been increasing with an increase in earnings.

Seeking Alpha

Guided by this trend, I expect its dividend to grow in the future given that FAST I is projected to grow by 7.6% in the next three years. In summary, FAST is a great dividend stock with an impressive dividend history and an attractive yield. Its dividend is sustainable with a future growth potential.

Above all, the safety of this dividend policy is in its strong balance sheet. FAST has a net debt of about $313.7 million which is 0.29x the company’s levered FCF of $1.06 billion. With a trailing operating cash flow of $1.43 billion, it is clear that this company has a solid ability to generate enough cash flows to meet its obligations and therefore it is in a strong position to sustain its dividend policy.

Valuation And Technical Take

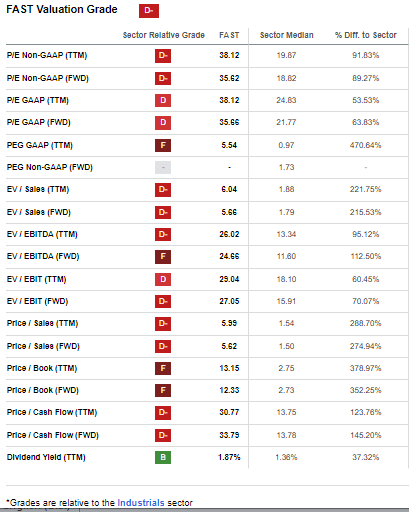

In this section, I will consider the relative valuation metric to complement my technical analysis to recommend the appropriate investment decision. To begin with, FAST is trading at a trailing PE ratio of 38.12 which is significantly above the sector median of 24.83. In addition, its trailing PS ratio of 5.99 is way above the sector median of 1.54. This implies that this company is overvalued based on its earnings and sales. To say the least, FAST is trading at a premium in all its relative valuation an indication that this stock is not a good value investment at the moment for potential investors.

Seeking Alpha

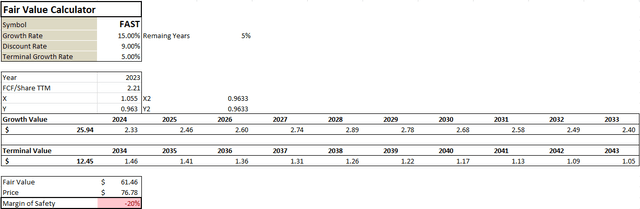

In addition, I will employ a DCF model to estimate the fair value of this stock. In my estimation, I used a growth rate of 15% which is conservative considering the company’s 5-year free cash flow CAGR of 20.39. Further, I used a discount rate of 9% which is the company’s WACC based on my computations. Assuming the trailing FCF/share of $2.21, below is the output of my model.

Author

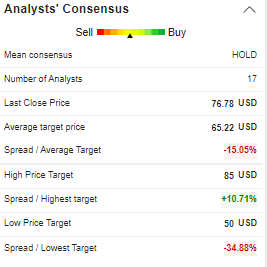

According to my model output, FAST has a fair value of $61.46 meaning it is trading at about 20% premium. My results are in line with 17 analysts’ consensus estimates with an average price target of $65.22.

Market Screener

Based on the above data, it is evident that FAST is overvalued and therefore this is not a good value stock at the moment. I agree with the consensus overall recommendation of a hold decision.

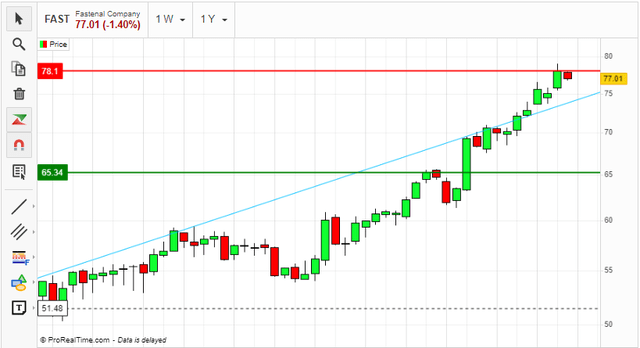

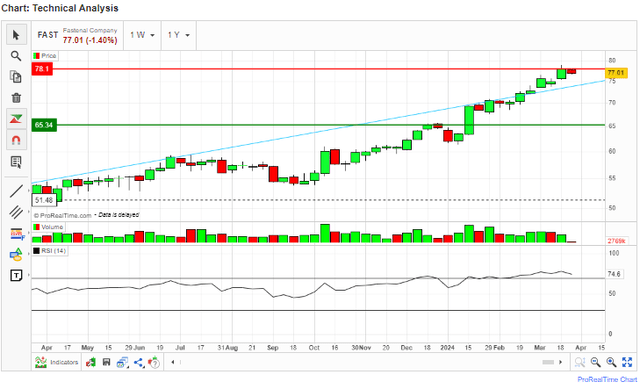

Let’s look at this premium valuation alongside technical analysis for a clear investment direction. Firstly, this stock has been in a strong upward momentum but it appears to have formed a strong resistance at about $78.1 and a bearish candle has formed which could be a sign of a trend reversal. However, this has to be confirmed before we conclude it’s a trend reversal.

Market Screener

I will dive deeper here and look at another indicator to get a clear view here. Looking at the RSI, it is at 74.6 which implies that this stock is in the overbought region where a trend reversal is likely. Considering the premium pricing and this overbought condition, I believe a pullback or a trend reversal is more likely than a major upside potential.

Market Screener

Guided by the valuation and the technical analysis, I believe that a hold decision is justified here because this stock is trading at a premium with a potential trend reversal.

Investment Take Away

Based on my analysis, there is no doubt that FAST is an attractive company with solid growth catalysts. Additionally, its dividend is very attractive. However, from a technical and relative valuation standpoint, FAST is not a good value investment. For these reasons, I recommend patience for value investors until the stock price drops to about $63.34 which is my immediate support zone marked in green in the charts above. For dividend investors, if you’re willing to pay a premium price for a great dividend stock you can consider FAST. Otherwise, you can wait for a pullback and enter the company at a cheaper price, perhaps at about $63.34. In a nutshell, the rule of thumb is a hold until the valuation improves.

")

")

")