")

Baker Hughes (NASDAQ:BKR) is well-positioned for the next wave of energy production as global energy interests shift away from a resource mindset to a focus in emissions control. Baker Hughes offers a wide array of services that caters to the shift in the growing demand for natural gas and the gradual shift towards hydrogen fuel. Though Baker Hughes may experience some headwinds as operators turn away from heavy drilling programs to enhanced oil recovery, I do believe the firm offers the infrastructure necessary to cater to these needs. I provide BKR shares with a BUY recommendation with a price target of $45.70/share at 10.29x eFY25 EV/aEBITDA.

Operational Paradigm Shift

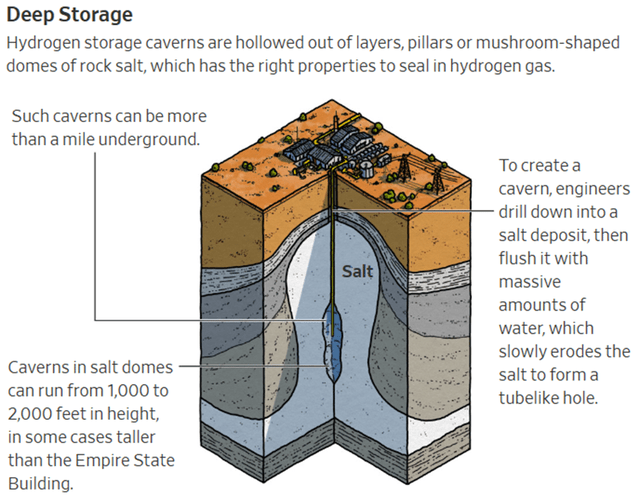

Baker Hughes is entering a major paradigm shift in resource production as international producers seek to adjust their focus from liquids to gas production. This shift was also seen by Schlumberger (SLB), who voiced similar changes in customer demand in their q1’24 earnings call. By and large, each company appears to be aligned with the infrastructure and chemicals needed for the next generation of oil and gas production. This has led to a 3x order improvement for Baker Hughes in their gas tech business and has led management to forecast a 50% y/y increase in segment orders for eFY24. I anticipate non-LNG gas tech to continue to realize growth in the coming years as EMEA producers focus more heavily on generating cleaner fuel sources as they have found that attempting to jump directly to renewables from coal has only led to more coal dependency. I believe this fallacy can and will be corrected through increased investments in natural gas infrastructure and strategic investments in hydrogen fuel. Considering foreign investments in hydrogen electrolysis technology developed and utilized by companies like FuelCell (FCEL) and domestic investments by New Fortress Energy (NFE), and NextEra Energy (NEE), and the demand for hydrogen and ammonia by industrial and chemicals manufacturers, I anticipate continued growth across this fuel source with the presumption that domestic legislation loosens up. Exxon Mobil (XOM) and other potential hydrogen producers have voiced concerns with the stringent IRA regulations relating to how hydrogen must be generated in order to receive government incentives to make production profitable. This may also affect the above-mentioned names that are seeking to generate hydrogen and ammonia and may inevitably stump the industry. The Wall Street Journal reported an interesting use case relating to hydrogen on April 19, 2024, as a potential store of renewable energy. The idea behind this use case would be to leverage renewable energy sources to generate hydrogen through electrolysis technology, which is very energy-intensive, and store the hydrogen in salt caverns for future use. Though I believe that this is just another step in the energy production lifecycle that will likely result in wasted energy through transmission, the technology has the ability to benefit Baker Hughes on multiple fronts. One major advantage Baker Hughes has with their hydrogen turbines is that they can be used with either natural gas or hydrogen. This can become a major cost-savings benefit to utilities as dual generators will not be required to transition from one fuel to the other, let alone eliminate replacement costs if natural gas-fired plants were to be decommissioned in favor of hydrogen fuel. In short, Baker Hughes’s technology can be scaled for natural gas power generation and transitioned to hydrogen when the market is ready.

Wall Street Journal

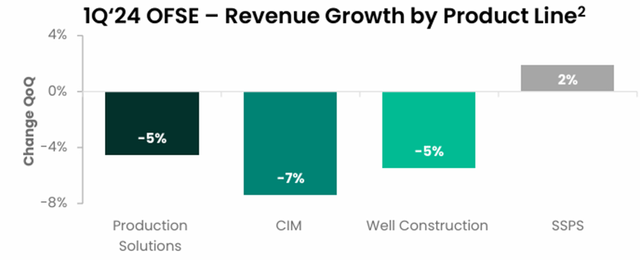

The decline in North American OFSE was expected as domestic rig count has been in steady decline as producers find new ways to optimize well production. As management had alluded to in their Q1’24 earnings call, operators are seeking to squeeze as many liquids out of each well as technologically possible through novel techniques, such as chemicals agitation and CO2 injection. Antero Resources (AR) reported dropping a drill rig at the start of 2024; Occidental Petroleum (OXY) had voiced a shift in focus from land basins to offshore in the Gulf of Mexico is also focusing their efforts in enhanced oil recovery, or EOR, by utilizing their carbon capture technology and pipeline system to inject CO2 in wells to further agitate oil production; Devon Energy (DVN) is testing refracking methodologies to enhance well production in their Eagle Ford assets; and Diamondback Energy (FANG) guided a reduced capital investment program for eFY24 as the firm focuses on building up their DUC inventory. I believe the core focus for these operators is shifting from maximizing production through new drilling programs to enhancing well recovery through well optimization, longer laterals, and CO2 and chemicals injection. I believe this is what management had alluded to when mentioning the shift from CAPEX spend to OPEX spend. Baker Hughes isn’t alone in this change either. Schlumberger is facing the exact same phenomenon and is proactively adjusting their operations to cater to this changing demand by acquiring ChampionX (CHX). Be sure to review my report covering Schlumberger here.

Much of this change can be seen in Baker Hughes’s OFSE segment with the decline in production solutions, completion, and intervention & measurement. On the other hand, Baker Hughes benefited from the strength in offshore in their subsea sub-segment.

Corporate Reports

Two areas in which Baker Hughes experienced significant growth were in their CTS driven by hydrogen and emissions abatement and gas tech services. Considering the long-term outlook for international gas demand and the emergence of hydrogen as a fuel, I anticipate this segment to experience significant growth in the coming years as capacity is built out. As management had pointed out in the q1’24 earnings call, the shift away from energy transition to emissions management will significantly impact Baker Hughes in a positive way as firms seek to reduce carbon and methane emissions. I expect strong tailwinds across their CTS orders going forward. Though this segment is considerably smaller when compared to OFSE, I believe it can become a major driver for Baker Hughes’s future growth outlay in both the domestic and international markets. As this segment scales, I anticipate some EBITDA margin expansion to follow which should help get the firm to their 15.6% eFY24 target.

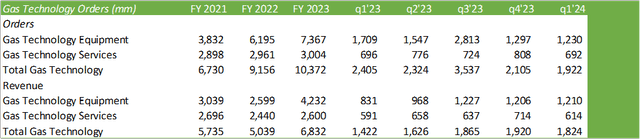

Looking to financials, gas tech orders were up on a y/y basis; however, services declined significantly from the previous year.

Corporate Reports

Revenue within the segment improved on a y/y basis as producers seek to bolster their gas production to cater to LNG trade. I expect this trend to continue throughout the duration of the decade as natural gas becomes a larger proportion of the energy mix.

Corporate Reports

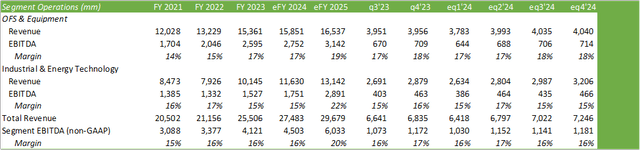

In addition to revenue growth, I anticipate significant improvements to EBITDA margins as the gas tech and new energy segment continues to scale. Given that enhanced oil recovery is becoming a more prominent shift in how operators produce hydrocarbons, this segment has the ability to drive growth over the course of the next decade.

Considering negative risks, I believe that the only real headwind would be the transition to nuclear power generation as renewables, such as solar and wind, have been found to be unreliable in times of stress. In relation to this, I do anticipate solar and wind capacity to continue to be built out; however, I’m a firm believer that these resources are more dependent on sustainable power generation from traditional power sources such as gas, coal, and nuclear. This thesis is aligned with the need for energy security and reliability of the grid.

Corporate Reports

In terms of operations, I anticipate Baker Hughes to realize margin improvement and strong free cash flow going through eFY24-25. I believe that Baker Hughes will experience significant tailwinds in expanding their new energy segment across regions. This should provide strength in generating more durable free cash flow going forward.

Value & Shareholder Value

Corporate Reports

Baker Hughes offers strong shareholder benefits through their dividend and share repurchase program. The firm aims to distribute between 60-80% of their free cash flow back to shareholders. Baker Hughes repurchased $158mm in shares during q1’24 and has $2.1b remaining under their current repurchase program. Given the firm’s low leverage of 0.8x net debt/aEBITDA, I do not anticipate any significant financing restrictions as the firm scales their new energy business.

Given the forward trajectory of the firm, I believe BKR shares can offer significant upside potential as oil recovery becomes a more valued focus for producers paired with emissions control. Given my financial forecast, I value BKR shares at $45.70/share at 8.75x eFY25 EV/aEBITDA and maintain my BUY recommendation.

Corporate Reports

")

")

")