")

")

Written by Nick Ackerman, co-produced by Stanford Chemist.

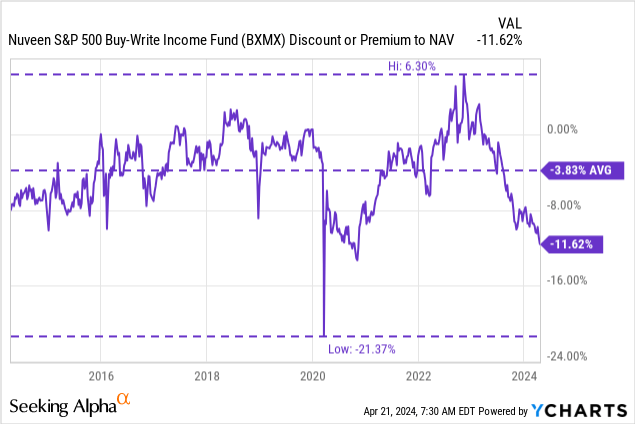

We last covered the Nuveen S&P 500 Buy-Write Income Fund (NYSE:BXMX) in August of last year. At that time, the fund’s discount was opening up, but it wasn’t anything too exciting. Since then, the fund’s discount has now widened substantially, and the share price is pushing to a double-digit discount to its net asset value.

BXMX Basics

- 1-Year Z-score: -1.58

- Discount: -11.62%

- Distribution Yield: 7.59%

- Expense Ratio: 0.92%

- Leverage: N/A

- Managed Assets: $1.526 billion

- Structure: Perpetual

BXMX’s investment objective is to “seek attractive total return with less volatility than the S&P 500 Index…” They intend to achieve this through “…investing in a global equity portfolio that seeks to substantially replicate the price movements of the S&P 500 Index and by selling index call options covering approximately 100% of the Fund’s equity portfolio value with a goal of enhancing the portfolio’s risk-adjusted returns.”

Performance – Discount Provides Tempting Opportunity

The performance of BXMX in terms of total returns has been lagging the S&P 500 Index significantly.

BXMX Performance Since Prior Update (Seeking Alpha)

To be fair, in any bull market, a call writing fund will lag the direct index they are looking to track. BXMX is a fund that targets a 100% overwrite of its portfolio, and that means the upside can generally be quite limited. This is because when the market is rising rapidly, these written calls are generally losing money. They are cash-settled since an index can’t be owned directly, but thanks to mirroring the index in its underlying portfolio, that means that at least the losses are essentially capped.

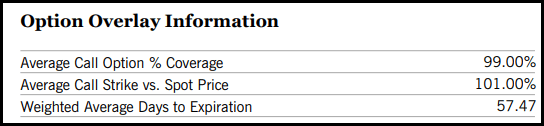

A call-writing fund will lag to some degree, but it’s especially true because the fund writes index calls right at the money. With the average call strike versus the spot price of 101%, it means the fund is further limiting its upside. On the other hand, it also means the fund would be receiving more options premium upfront.

Another interesting note on this fund is that the weighted average days to expiration is 57.47 days, while most other call writing funds generally focus on writing monthly or less. The S&P 500 Index has daily options available, so really, any period of time can be selected as long as it is a weekday. With a longer average day to expiration, the fund is receiving a larger premium, but is also trading that for more uncertainty due to the longer period of time.

BXMX Option Stats (Nuveen)

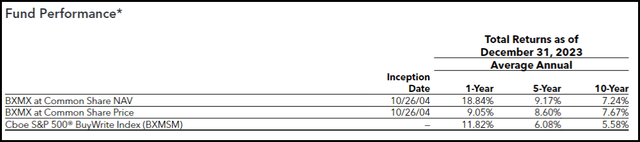

Therefore, a vanilla benchmark like the S&P 500 Index as a benchmark may not be the most appropriate. The fund provides its own historical annualized breakdown against the CBOE S&P 500 BuyWrite Index, which is more appropriate.

BXMX Annualized Performance Vs. Benchmark (Nuveen)

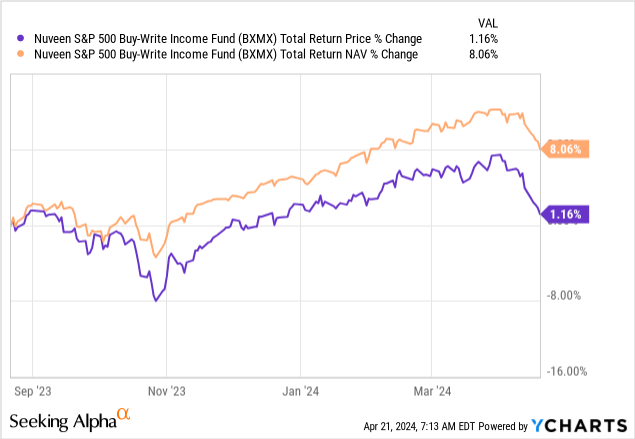

Another factor during this time, and one of the main points I wanted to highlight with this fund, is that the fund’s total NAV returns were actually doing significantly better during this period. Yes, again, it lagged the vanilla S&P 500 Index during a period where it was mostly a bull market but still looked much more respectable compared to the total share price return.

Ycharts

Of course, when this occurs, it provides the natural result of a closed-end fund’s discount getting wider. At this point, BXMX is trading at a deep discount on an absolute basis, pushing into a double-digit level and also on a relative basis. This means that it is now cheap against its own historical levels, which makes it a much more interesting candidate to consider today than when we previously took a look at the fund.

Interestingly, this fund has had several periods of time where it traded at a premium, and that really brought up the fund’s average. We are now trading around Covid pandemic discount levels (excluding the sharp panic drop that occurred on March 18 and pushed the fund’s discount to over 20%.)

Ycharts

The current pullback in the market, causing some added volatility and uncertainty going forward, is likely a contributing factor. Investors could be pushing this fund to a larger discount as they move out of equities as they expect the market to continue to experience some turbulence.

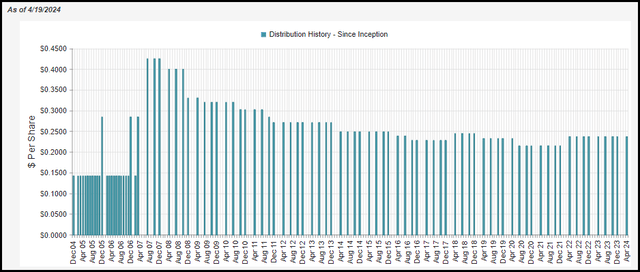

Distribution – 7.59% Paid Quarterly

One of the benefits of option writing funds is that they can bring in more cash flow through receiving these option premiums. These option premiums, plus the underlying dividends paid from the holdings of the fund, help to contribute to a higher relative distribution rate. One gripe may be from income investors that it is a quarterly distribution schedule rather than monthly like many of its peers.

BXMX Distribution History (CEFConnect)

Currently, the fund’s share price shows a 7.59% distribution rate with a 6.70% NAV rate. The lower NAV rate is thanks to the fund’s discount and is relatively low compared to other call-writing peers, which may be a good thing in this case. If one is expecting more downside risk ahead, it might be that BXMX is more likely to avoid cutting its distribution if that is the case.

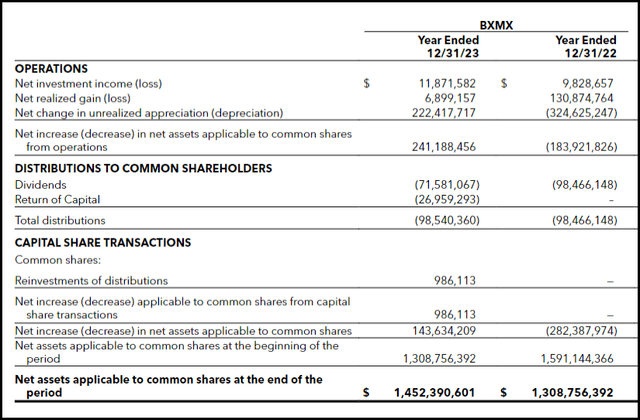

Either way, the fund is an equity fund and will require capital gains to fund its distribution. As we can see, the underlying dividends received from the portfolio were only enough to put net investment income coverage at ~12%.

BXMX Annual Report (Nuveen)

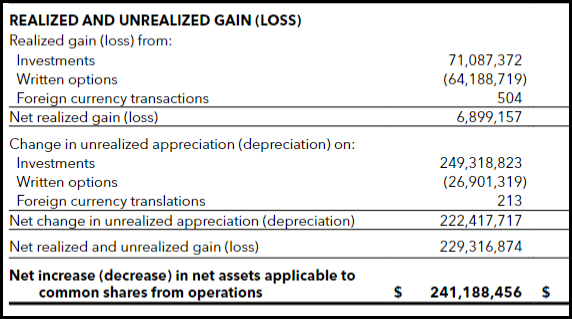

Those capital gains would need to fund the rest of the shortfall, but that doesn’t matter if it’s from the underlying portfolio or from the written options.

BXMX Realized/Unrealized Gains/Losses (Nuveen)

With 2023 being such a solid year for the overall equity market, it resulted in the fund’s written options ultimately realizing a loss through the year. The realized gains from its underlying portfolio were more than enough to offset those losses. The unrealized gains the portfolio experienced were massive, and that’s what helped push for the overall increase in net assets and, ultimately, the driver of the ~19% total NAV returns seen in this fund for 2023

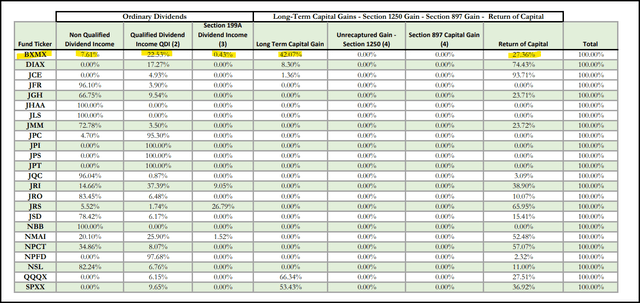

For tax purposes, the breakdown characterization will generally reflect the reliance on those capital gains needed to pay out shareholders. In 2023, it was a reflection of that, with the fund’s distribution characterized as ~42% LTCG. However, the fund also saw some return of capital.

BXMX Distribution Tax Classification (Nuveen (highlights from author))

We already noted that the fund’s NAV returned ~19% in 2023, but there was ROC anyway. This can happen if the fund doesn’t realize enough gains, which is precisely what happened. The fund realized gains, but it was largely offset by the realized losses from the options writing. Net realized gains for the fund came to less than $7 million when they would have needed nearly $87 million in realized capital gains to ‘cover’ the distribution. Since the NAV did rise, it wouldn’t be considered destructive ROC.

BXMX’s Portfolio

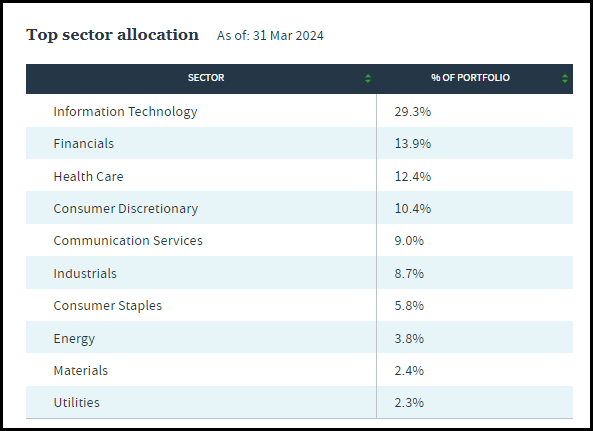

For the most part, BXMX’s portfolio is what you would expect an S&P 500 Index-focused fund to be; they list 99.49% of the portfolio as being invested in large caps and with a significant weighting to the technology sector. Of course, the significant, oversized weighting to the tech sector is merely a reflection of what the S&P 500 Index has become itself.

BXMX Top Sector Allocations (Nuveen)

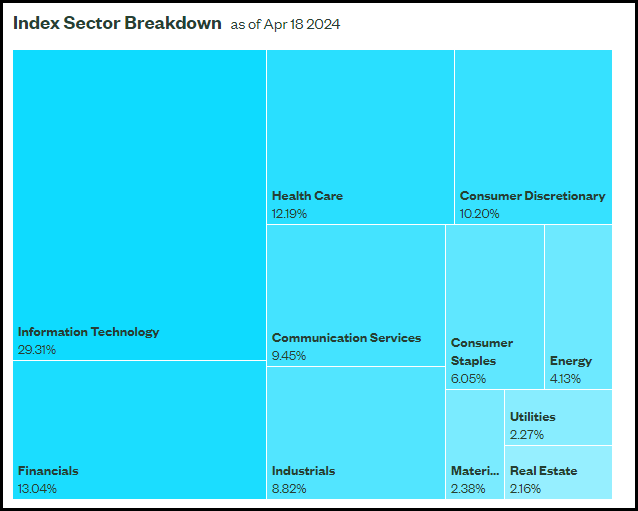

The above compared to the below S&P 500 Index weighting shows that it is highly overlapping, which is exactly what is expected.

S&P 500 Index Sector Breakdown (SSGA)

This helps to ensure the scenario where the fund can be ‘covered’ from unlimited potential losses should the market really start to run higher. The only caveat is that they do it with 249 holdings rather than the ~500 in the index.

Those 249 holdings could significantly underperform the other half of the index, and that could cause a mismatch; however, that’s highly improbable to happen to any significant degree – but not impossible, I suppose. That’s because they hold all the key holdings of the index itself as well.

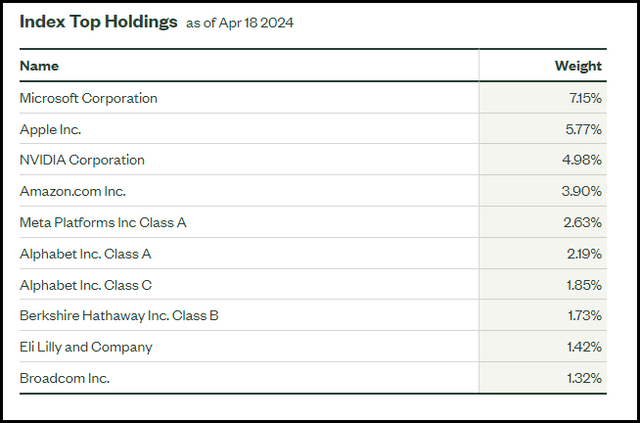

Those positions that have overwhelming control over which direction the index will go are the Mag 6 names (dropping Tesla (TSLA) out of the Mag 7 group), which are the holdings that BXMX overweights as well.

BXMX Top Ten Holdings (Nuveen)

In fact, the top ten holdings listed above for BXMX are nearly perfect mirrors of the S&P 500 Index itself, allowing for some relatively immaterial sway in terms of the percentage weightings. Again, this is exactly what is expected, as the fund can then ‘cover’ its call-writing options contracts.

S&P 500 Index Top Holdings (SSGA)

Conclusion

BXMX is trading at a significant discount, which makes it a much more tempting consideration at a double-digit discount. The overall market volatility is likely a contributing factor, and whatever way the market goes, as measured by the S&P 500 Index, is likely the direction in which this fund will head. If one is expecting more meaningful downside moves and the pullback to turn into a potential correction, then holding off on putting any money to work is likely the ideal move.

The option premiums received from writing calls against the S&P 500 Index are only a slight hedge against downside moves. However, writing call options also means that upside moves will be capped if the market moves steadily higher. As is generally the case with call-writing funds, the fund would benefit from a sideways market on a relative basis. Overall, the fund is more focused on providing higher distributions to investors with this strategy, and that is exactly what the fund does with its 7.59% distribution rate.

Q1 2024 Earnings Call Transcript")

")

")