")

")

An appealing growth story clouded by competition and balance sheet risk

TH International (NASDAQ:THCH) or Tim’s China has drastically grown its revenue from just $7.5 million in 2019 to $222 million in 2023. The acquisition of the exclusive rights for Popeyes in China has given it an additional growth driver going forward. Even though Tims China promises attractive growth rates in the upcoming years, it is currently facing tough challenges in the form of intense competition from rivals as well as a weak balance sheet. There is plenty of upside from today’s share price if the management team is able to navigate this situation successfully. Regardless, the downside risks are too significant to warrant an investment right now, and I consequently prefer to wait on the sidelines with a Neutral stance.

Tims China’s growth story

As the master franchisee of the Tim Horton’s coffee shops in China, Tim’s China has seen rapid growth since opening their first store in 2019. This write-up by Seeking Alpha contributor Catalyst Capital delves extensively into Tim China’s growth prospects that are fueled by China’s increasing coffee consumption. Additionally, in March last year, the company acquired the rights to exclusively develop and sub-franchise the Popeyes brand in China. At the end of 2023, the company had a total of 912 stores, which included its owned and sub-franchised stores as well as 10 Popeye’s stores.

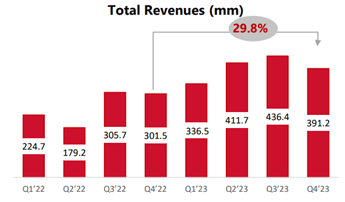

Company presentation

The company continues to show strong revenue growth, with almost 30% year-over-year growth reported in Q4 2023, as represented above. It also has a rapidly growing loyalty club with over 20 million registered loyalty club members, a number that Starbucks (SBUX) only reached last year in China.

A recap of the progress in recent quarters

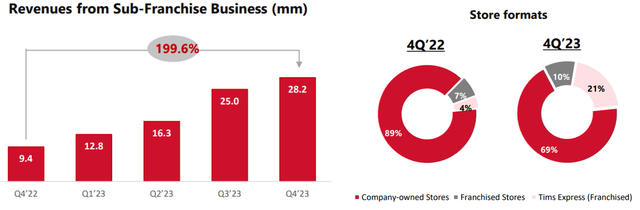

After a very capital intensive phase of building out its owned and operated stores, Tims China has recently been able to rely on its less capital intensive sub-franchise business to drive growth. Sub-franchise revenue is highly profitable for the company as it is an expense free percentage of gross revenue that it receives from the sub-franchise stores.

Company presentation

According to the graphic above from its Q4 2023 earnings report, it can be seen that sub-franchise revenue growth is strong with quarterly revenue contribution of 28.2 million RMB (or $3.91 million). This represents roughly 7% of Tims China’s total revenue. As also depicted above, new stores are increasingly more franchisee operated, and therefore investors can expect future contribution from sub-franchise revenue to become much more significant. Moreover, Tims China has been successful in signing leading and well established franchise partners which include convenience store chain Easy Joy, real estate company Century 21 and snacks retailer Bestore.

Created based on company data

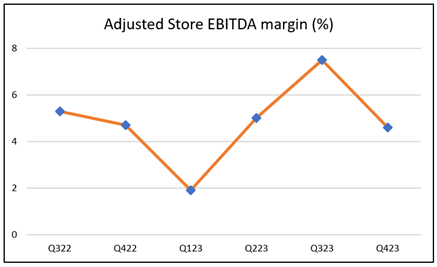

When it comes to their owned and operated stores, the company has faced huge challenges in driving growth in store level EBITDA margins. As shown in the chart above, its margins of around 5 to 6% pale in comparison to its initial targets in 2021 which were above 15%, as well as to peers such as Yum China (YUMC) which also have margins in the mid teens range. Tims China’s management needs to execute on their plans to drive this margin higher so that it is able to reach a position where its existing stores produce sufficient cash to fund the company’s future growth.

Competitive threats

The major issue that the company faces with regard to increasing its profit margins is the intense competition among the players in the Chinese coffee market. Tims China faces steep competition from rivals such as Starbucks, Luckin Coffee (OTCPK:LKNCY) and Cotti Coffee. Large levels of discounting by its rivals in an effort to gain market share has resulted in average selling prices dropping by almost 30% in 2023. On their recent earnings call, CEO Yongchen Lu had this to say regarding competition.

There is now a price war going on, which we do not believe is sustainable though. We do see some market disruptions. However, in the long run, this does not seem to be a profitable way to operate a business. Despite a price war leading to strong revenue and unit growth, margins will inevitably get compressed.

With regard to how Tims China differentiates itself from the competition, he said:

Our differentiated product offering, at compelling prices with fresh food options, is so good that we don’t really compete directly with those brands. And we take some share from the market.

The impact from the ongoing price war between the players can be seen in Tims China’s same store sales growth for company owned and operated stores, which was -0.4% and 2.5% in Q3 and Q4 2023 respectively. This is a significant deceleration compared to the prior two quarters of the year which showed increases of 8.0% and 20.4% in Q1 and Q2 2023.

Looking forward in 2024, the broader situation does not seem to be improving. According to Starbucks’s latest quarterly report for the first three months of 2024, its revenue from China declined 8%, driven by an 11% decrease in same store sales. On its earnings call, Starbucks CEO Laxman Narasimhan highlighted multiple headwinds that the company was facing in China, saying:

Turning our attention to China. Macro pressures resulted in traffic contraction this quarter. Performance was impacted by a decline in occasional customers, changing holiday patterns, a highly promotional environment and a normalization of customer behaviors following last year’s market reopening.

Several factors pointed out as impacting Starbucks, are indeed very relevant to Tims China, and I therefore expect 2024 to also be another challenging year for it to navigate.

Capital requirements and balance sheet risks

Profitability concerns

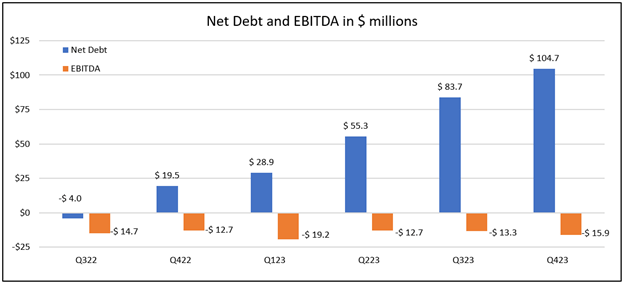

Tims China’s rapid revenue growth has come at the expense of rising levels of debt. Since being in a slight net cash positive after raising capital during its SPAC IPO in September 2022, its net debt has grown above $100 million in Q4 2023 as shown below. The company has continued to be unprofitable on an EBITDA basis, though management has guided to achieving breakeven later this year.

Created based on company date

Rising debt levels and interest costs

Even if the company reaches its target for EBITDA breakeven later this year, it is unlikely that they will be break even on a cash flow basis until late 2025. This means investors should expect the company’s net debt levels to rise even further in upcoming quarters, which will further weaken its balance sheet. It is a concern that its total liabilities of $371 million on the balance sheet are much higher than the total assets of $312 million at year end 2023.

The company’s borrowings are mainly in the form of bank loans as well as a $50 million convertible note which is due in December 2026. The convertible note carries slightly lower risk than normal since it is provided by one of the company’s main shareholders. As per its Annual report for 2023, it can be seen that this shareholder has in March 2024 provided the company with further financing of $20 million through junior promissory notes bearing an interest rate of SOFR+8%. This latest funding implies an interest rate above 13% which is far less appealing to the company compared to its existing bank borrowings which are stated in its Annual report to have interest rates between 2.75% and 4.6%.

The company’s interest expenses were also sharply higher last quarter, prior to receiving their recent funding. Interest expenses had risen to $2.9 million in 2023 compared to $2.1 million in 2022. Interest payments associated with the latest junior promissory note would further increase interest costs by another $2 million on an annual basis. More cash spent towards servicing the debt would result in less cash being available to fund its growth.

Valuation and risk-reward analysis

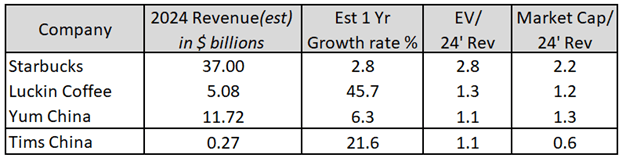

Tims China is still in its early stages of growth and has a long runway ahead in China’s coffee market as well as the fast food segment through Popeyes. Since it is still unprofitable, I have chosen to value it on a revenue basis versus its peers. As shown in the valuation comparison table below, at today’s share price of $1.1, Tims China is attractively valued in comparison to its peers such as Starbucks, Luckin Coffee and Yum China when considering its growth rate and maturity level. I think the main reason for the large discount is Tims China’s lack of profitability and high level of debt, and it seems justified presently.

My valuation comparison

If the company can prove that it can reach profit margins that are on par with its peers, I believe there is significant potential for its valuation multiple to rise to levels closer to its peers. However, considering the risks due to its unprofitability thus far and its weak balance sheet, I believe the risk-reward is not favorable to initiate an investment now. I instead recommend carefully following the company’s progress in the upcoming quarters to figure out if it is heading in the right direction.

What investors should look for in upcoming quarters

Store level EBITDA margins in company owned and operated stores is a crucial metric to follow. This should trend toward double-digit percentages this year so that Tims China’s existing stores can produce sufficient cash flow to fund the growth of new stores.

Another crucial number to look out for is the sub-franchise revenue growth, and ensure that its contribution increases from around 7% of total revenue last year towards 15% this year. This will significantly support the company’s target of breakeven EBITDA.

I am interested to see if the company can replace their high cost debt with cheaper options, thereby reducing their cash expenses towards interest payments. Otherwise, I would not be surprised if the company chooses to raise more cash through a secondary offering.

Conclusion

Despite its appealing growth prospects and attractive valuation, Tims China finds itself in a tough spot due to its high debt level. A highly competitive market has made it harder for profit margins to rise, thereby delaying the company’s ability to self-fund its growth. The bull case hinges on the rapid increase in sub-franchise revenue which should help the company reach breakeven EBITDA at the end of this year, and subsequently cash flow positive next year. However, until the company proves that it is on a sustainable path to grow profitably, I think investors are best served to stay on the sidelines.

")

Q1 2024 Earnings Call Transcript")

")