")

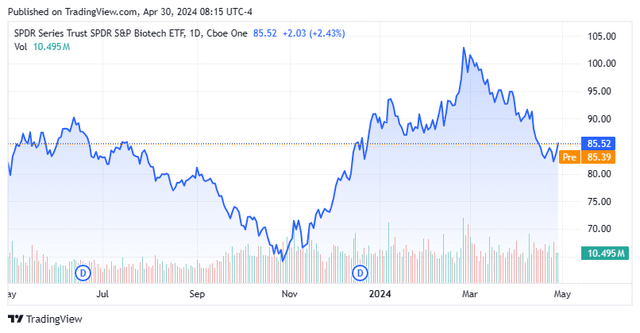

It has been a wild ride for investors in small and midcap biotech names over the past nine months. This can be seen in the chart around the SPDR® S&P Biotech ETF (NYSEARCA:XBI) below.

Seeking Alpha

The exchange-traded fund, or ETF, is up a little over four percent (as of Monday’s close) from where it traded a year ago. It has had some major moves along the way to return around the same as the “risk-free” return from the 10-Year Treasury (US10Y) that provided considerably less angina. It should be noted that the biotech sector always provides a higher beta than the overall market, but recent trading action has been marked by significant volatility.

There are two key things to watch that will determine whether biotech can move significantly higher in the months and quarters ahead. They are highlighted below.

Higher M&A Volume:

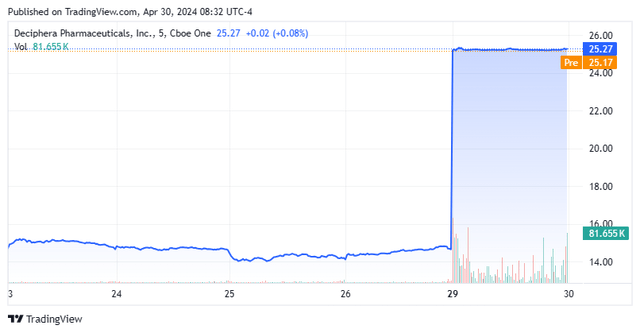

Nothing ignites the “animal spirits” more in this part of the market than acquisitions. We got an example of this on Monday when Deciphera Pharmaceuticals, Inc. (DCPH) was purchased in a $2.4 billion all-cash deal for $25.60 a share. This offer contained more than a 70% buyout premium. I profiled Deciphera and recommended a starter position in the name last week. Not coincidentally, the XBI rose just over 2.4% in trading on Monday and was one of the strongest-performing sectors in the market.

Seeking Alpha

There are several good reasons to believe that the next year should be supportive of solid deal volume in the biotech space. First, Big Pharma is flush with cash and was estimated to have some $700 billion of cash on its balance sheet as of last summer.

In addition, the industry always has to deal with patent expirations, which bring in generic competition and crush margins on previously blockbuster drugs. Finally, many large drugmakers such as Pfizer Inc. (PFE), Moderna, Inc. (MRNA) and Gilead Sciences, Inc. (GILD) have seen revenues from Covid-related vaccines and treatments fall off a cliff as the pandemic has become endemic. That provides some urgency to upgrade product portfolios and pipelines to replace those dissipating sales. In March, I put out two articles (I, II) on some small and midcap biotech/biopharma companies that made logical acquisition targets. The bottom line is if M&A volume picks up, the sector will likely move significantly higher. If it ebbs over spring and summer, it will be a headwind for performance.

Lower Interest Rates:

Rising interest rates impact all high beta parts of the market negatively, as the discount rate used to estimate future earnings and cash flows increases, lowering the value of these types of stocks. It is particularly harmful to biotech stocks, as not only earnings, but revenues might be many years down the road.

In addition, most developmental companies consistently have to raise new capital to provide the funding to advance their pipelines. If they do this via new debt, this results in higher interest rates and/or lower conversion levels (on convertible debt). The more popular form of raising funding is via secondary offerings. Higher interest rates usually mean that capital is raised at lower equity trading levels as well, needing additional warrants attached to these efforts, both of which are more dilutive to existing shareholders. Debt used in takeovers also becomes more expensive as well.

10 Year Treasury YIeld (MarketWatch)

It is no coincidence that biotech plunged 20% from early August to October 19th as the yield on the 10-Year Treasury went from 3.96% to five percent. Nor was it unrelated that XBI gained just over 50% from the market’s recent trough in October to the end of February as the 10-Year Treasury yield (US10Y) dropped below 3.9%. The XBI has given back just over 15% as the yield has risen since then to nearly 4.7%.

So, in summary, investors who want to know and profit from where biotech is heading need to pay attention to how M&A volume trends in the months ahead and where interest rates head from here. My guess is that the biotech sector and thus SPDR® S&P Biotech ETF will be directionless, but with volatility, until the Federal Reserve starts to cut rates. The time frame for Fed Fund decreases has been consistently moved back here to 2024, it should be noted. However, if current futures are correct, 1-2 cuts should happen towards the end of the year. That may bode well for a yearend rally in the sector.

")

")

(NASDAQ:SOUN)")

J.P. Morgan 52nd Annual Global Technology, Media and Communications Conference (Transcript)")