(SP500)")

")

With Property & Casualty (“P&C”) peers like Progressive Corp. (PGR) and Allstate Corp. (ALL) recently making new highs, I thought it may be timely to revisit United Fire Group (NASDAQ:UFCS), to see if its business fundamentals are also on an upswing.

Overall, bad underwriting results from the industry due to high inflation negative impacting claims is leading to a hard market, as insurers have been renewing policies at double-digit premiums. This bodes well for United Fire’s upcoming results.

However, I prefer to be conservative with respect to United Fire, as the company has underachieved in the past. For now, I am maintaining my hold recommendation.

Brief Company Overview

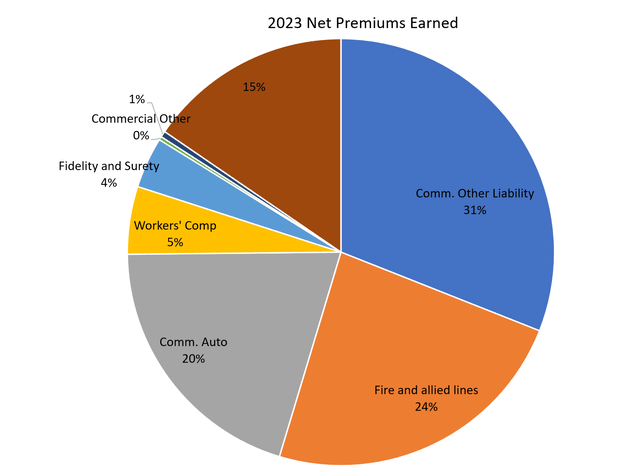

For those not familiar, United Fire Group is a small-cap P&C insurer that primarily provides commercial insurance like Commercial Property, Liability, Inland Marine and Workers Compensation insurance. By Net Premiums Earned (“NPE”), Commercial insurance accounted for 90% of total premiums, split between Commercial Other Liability (31%), Fire and allied lines (24%), Commercial Auto (20%), and Workers’ Comp (5%) (Figure 1).

Figure 1 – UFCS 2023 NPE by Business Line (Author created with data from 2023 10K report)

Underwriting Results From Bad To Worse

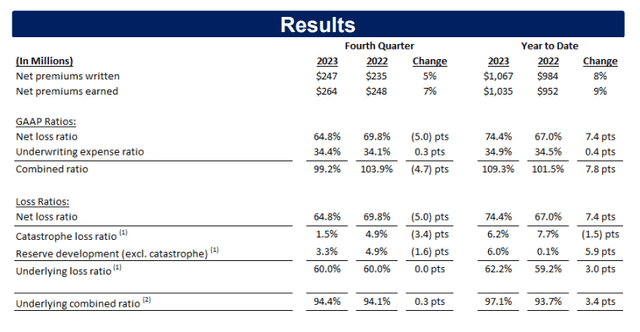

Although 2023 NPE grew 8.7% YoY to $1.04 billion, underwriting results at United Fire went from bad to worse, as UFCS reported a combined ratio of 109.3%, 7.8 pts worse than in 2022 (Figure 2).

Figure 2 – UFCS underwriting results (UFCS investor presentation)

In fact, this was the second worse underwriting result from UFCS in the past 6 years, reversing the prior two years’ trend of near breakeven underwriting.

Inflation Was The Main Issue

The main issue for UFCS in 2023 was prior period reserve developments, which is insurance industry jargon for when an insurer had done a poor job of estimating losses initially and now must take additional charges to ‘true up’ to the actual claims.

In my initiation article, I warned one of the key risks to UFCS was surging inflation as “insurers take on insurance policies in today’s dollars and pay out claims at a future date. If inflation is very high (for example the material and labor costs to fix a car) and the insurer did not take that into consideration when setting the policy rate, then actual loss ratios could be higher than expected” in future years.

Unfortunately, the inflation rooster had come home to roost for United Fire, as negative reserve developments added $68 million to 2023 losses or 6.0 pts to the loss ratio.

Overall, the P&C insurance industry is estimated to have recorded an underwriting loss in 2023 with combined ratio of 103.9% due to elevated losses.

Bad Times Lead To Hard Markets

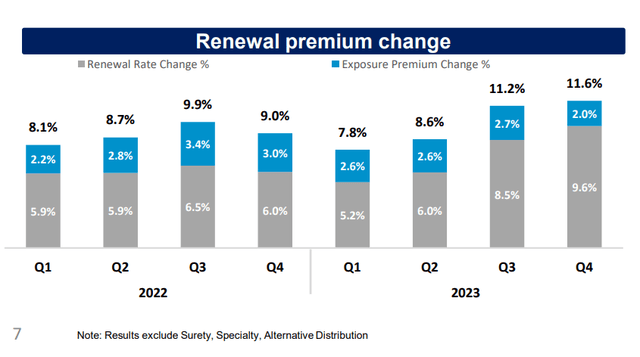

The bright spot for P&C insurers like UFCS is that bad times typically lead to hard markets, industry jargon for better pricing. Due to elevated loss ratios, many insurance companies have been renewing policies with double-digit increase in premiums (surging insurance premiums were called out in the recent CPI report). In 2023, UFCS’s commercial policies were renewed with almost double-digit increases (Figure 3).

Figure 3 – UFCS has been renewing policies at double digit premiums (UFCS investor presentation)

For UFCS, this is translating into better underwriting performance, with the company reporting a Q4/23 combined ratio of 99.2%, suggesting United Fire may finally be getting a handle on surging claims costs and repricing its policies appropriately. However, negative reserve developments still added $8.8 million or 3.3 pts to the Q4 loss ratio.

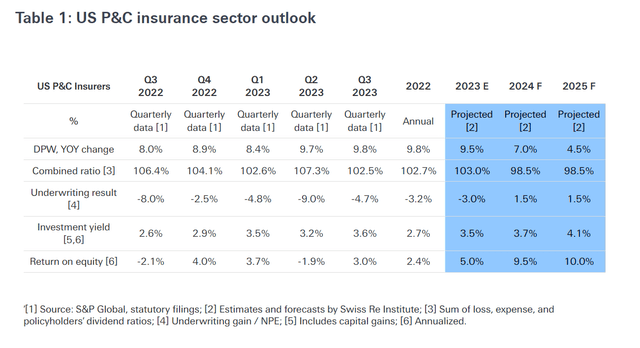

Looking forward, the insurance giant Swiss Re is forecasting U.S. P&C insurers to return to underwriting profitability in 2024 and 2025, which bodes well for UFCS (Figure 4).

Figure 4- Swiss Re expects industry to return to profitability (Swiss Re)

Higher Interest Rates Boosted Investment Income

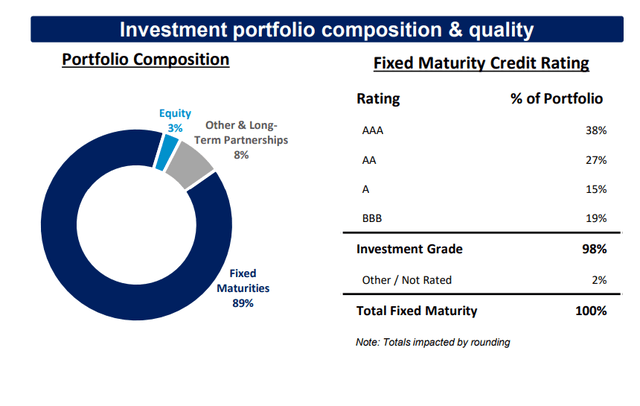

On the investment side, higher interest rates have benefited UFCS’ net investment income, as 89% of the company’s investment portfolio is fixed income (Figure 5).

Figure 5 – UFCS investment portfolio overview (UFCS investor presentation)

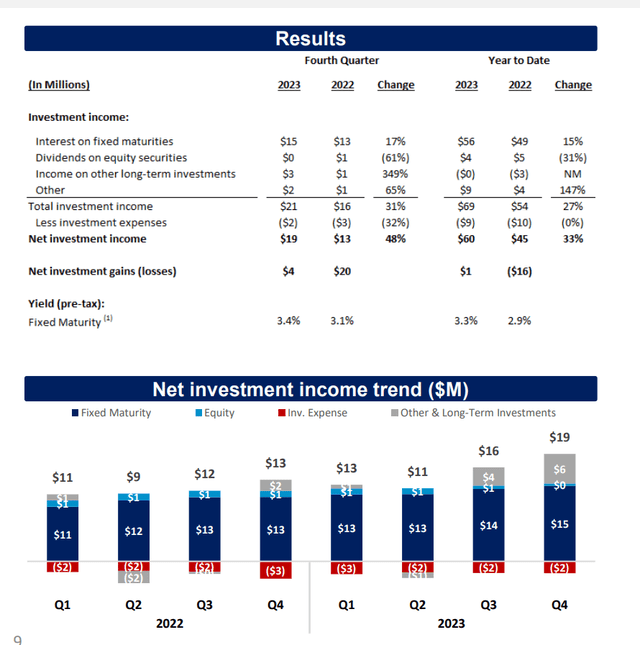

This has allowed the company to report net investment income of $60 million in 2023, 33% higher than 2022’s $45 million (Figure 6).

Figure 6 – UFCS investment results (UFCS investor presentation)

With the Fed expected to keep interest rates ‘higher for longer’ in a ‘no-landing’ scenario, investment income will likely continue to be strong in 2024.

Financial Performance Expected To Significantly Improve

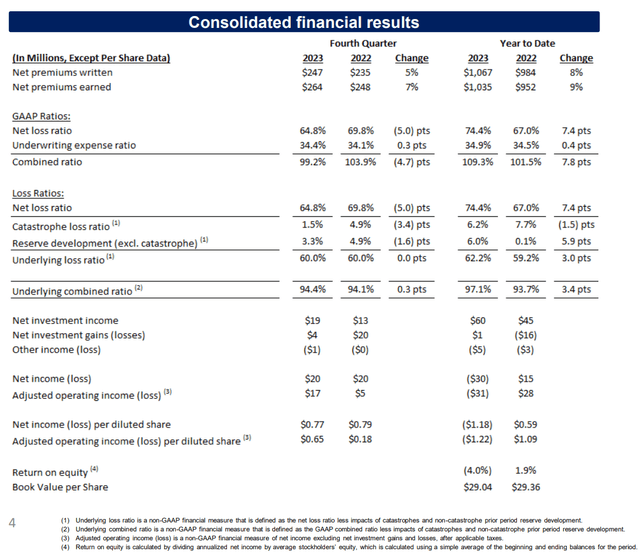

Putting it all together, improving underwriting results and strong investment income should lead to improved financial performance for UFCS in the coming year. In 2023, UFCS reported an adjusted net operating loss of $31 million or $1.22/share, compared to an adjusted net operating income of $28 million or $1.09/share in 2022 (Figure 7).

Figure 7 – Consolidated financial results (UFCS investor presentation)

Assuming underwriting results is near breakeven for UFCS in 2024 and the company once again earns ~$60 million in net investment income, I believe UFCS can earn higher returns than 2022’s $1.09 / share in adj. net operating income.

As a point of reference, Wall Street analysts expect UFCS to earn $1.10 / share in 2024 and $1.50 / share in 2025 (Figure 8).

Figure 8 – Wall street analyst expect improvement in earnings (Seeking Alpha)

Valuation Suggests Modest Upside

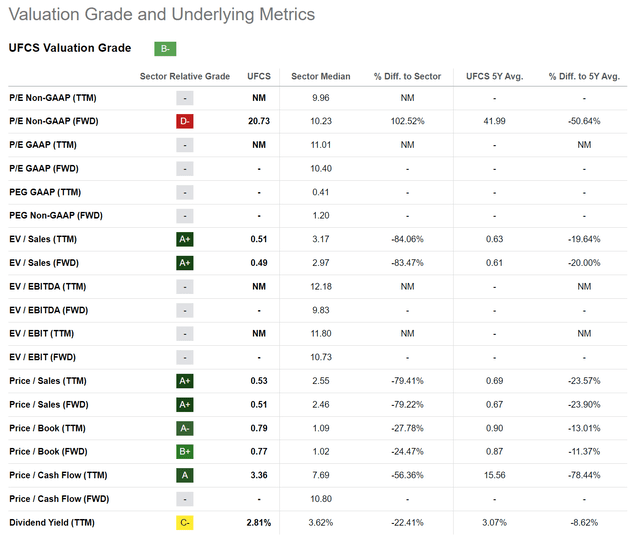

Based on my expectation that UFCS can return to profitability in 2024, I believe the company’s shares may have modest upside, as they are currently trading at only 0.79x Price-to-Book Value (Figure 9).

Figure 9 – UFCS valuation is at a discount (Seeking Alpha)

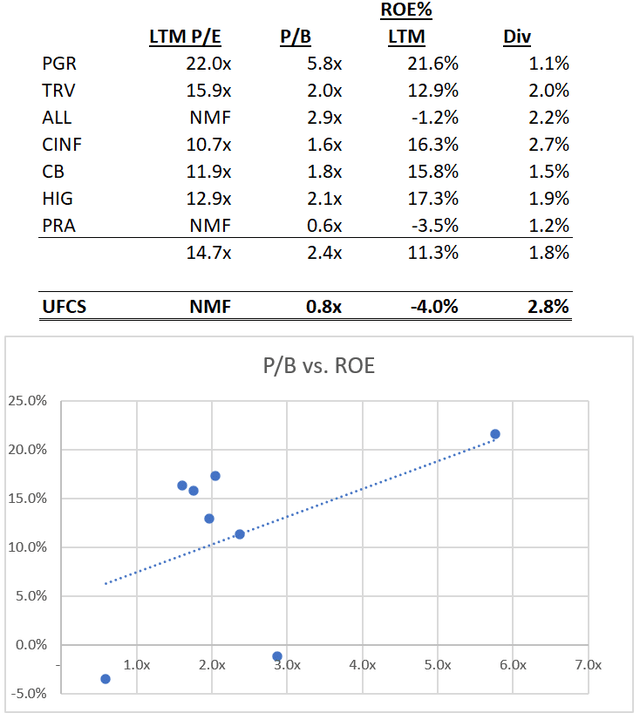

If the company can return to positive ROE, a re-rating to 0.9x to 1.0x book value is possible, judging by a regression analysis on P&C insurers’ ROE vs. P/B valuation (Figure 10).

Figure 10 – Regression analysis suggests upside for UFCS (Author created with data from tikr.com)

However, I am not yet ready to assign a higher valuation multiple to UFCS until the company can demonstrate sustained underwriting improvement. Having been burnt once by the company when I initiated with a buy rating in 2022 only to cut it a few short months later, I prefer to be conservative with the perennial underachiever.

Conclusion

Poor underwriting results in the past few years due to high inflation is leading to a hard market for P&C insurers, which bodes well for industry profitability. For United Fire, I believe the company should return to profitability in 2024, with net operating income likely higher than the results from 2022. This suggests a modest re-rating is possible.

However, until the company can demonstrate sustained improvements in underwriting performance, I prefer to be conservative and rate the company a hold.

Q1 2024 Earnings Call Transcript")

")