Q1 2024 Earnings Call Transcript")

")

More Than Just A Fun Get Together

I have often referred to the Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) annual meetings as a fun time for shareholders to get together and shop but not necessarily receive new information about the company in the marathon Q&A session. The 2024 meeting was different in that regard. With the passing of vice chair and Warren Buffett’s best friend Charlie Munger, the stage was occupied by Warren and Greg Abel, the future CEO and non-insurance vice chair. Insurance vice chair Ajit Jain was also present for the morning session. With Warren himself recognizing the limitations to his tenure and capabilities and Greg on deck to take over, we got more clarity than ever before about how things at Berkshire will change in the future.

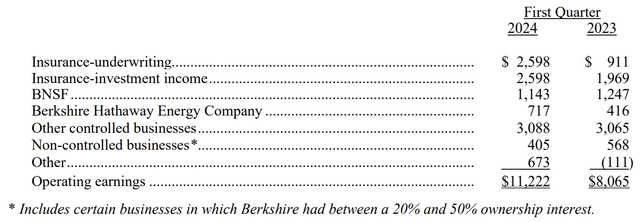

Prior to the meeting, Berkshire released Q1 2024 results. On an overall company basis, they were excellent, with operating income of $11.2 billion, up 39% from Q1 2023. At $5.20 per B share equivalent, the results beat analyst estimates for the quarter by $0.29, although neither Warren nor most Berkshire shareholders focus on that metric.

Berkshire Hathaway

The drivers of this result should be familiar to those who follow Berkshire closely or read my quarterly articles on the company. Insurance had strong underwriting performance, helped by premium raises and lack of major catastrophic losses in the quarter. BNSF railway continues to lag its peers. Berkshire Hathaway Energy had an OK quarter, which beat last year mainly because no new charges were taken for the PacifiCorp wildfires, although the problem is definitely not yet behind them. Other businesses were in line, with manufacturing surprisingly strong and Service and Retail starting to show signs of consumer weakness.

While I usually like to focus on the operating companies in my analysis, many of the results we saw in Q1 are similar to recent quarters. Rather than rehash them, I will start with a review of Berkshire’s investment portfolio and capital allocation, where there were several new headlines coming out of the Q1 earnings and annual meeting. I will then touch on the businesses briefly, focusing on discussions from the meeting. Finally, I will update my valuation model. Last quarter, I rated Berkshire a Hold, due to valuation. This was a good call, with the stock down a little more than 2% since then. Book value has come up nearly 2%, while my estimate of intrinsic value is almost unchanged. The slightly wider discount to fair value, along with positive changes likely under Greg Abel’s future leadership deserve an upgrade to Buy.

Investment Portfolio

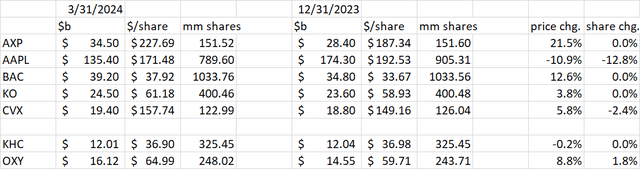

Berkshire’s biggest move in the past quarter was revealed before the meeting, where we saw from the 10-Q that the company sold about 116 million shares of Apple (AAPL), or 12.8% of its position. This accounted for nearly all of the $20 billion of stock sales in the quarter. Among Berkshire’s top 5 holdings, the only other sales were a continued trimming of Chevron (CVX) at the same time adding to Occidental (OXY), although Chevron remains the larger holding of the two energy companies.

Author Spreadsheet

Discussing the Apple sale during the meeting, Warren let his views on general market valuation and macro conditions come out a bit, an increasingly rare occurrence. He stated that he “did not mind at all” raising cash in the current market environment. He also didn’t mind paying 21% corporate tax on the capital gain because he expected the tax rate to be higher in the future. Towards the end of the meeting, Warren mentioned his worry about the US government fiscal deficit, suggesting it is not sustainable in the long term.

A smaller sale in Q1, but not previously reported, was the exit from Paramount (PARA) at a loss. Warren took “100%” responsibility for this trade. It was not done by Berkshire’s investment managers Todd Combs and Ted Weschler. Warren was a big admirer of Tom Murphy of ABC Capital Cities, which in my opinion gave him some false confidence that he understood the media business. Today’s environment with cord cutting and fickle streaming customers who churn from platform to platform is much more difficult than Tom Murphy’s world of 30 years ago.

The shareholder meeting had a large percentage of questioners from outside the US, several of whom asked Warren about Berkshire’s interest investing in their home country. Warren’s responses suggest that he lacks the interest and energy to pursue foreign opportunities. The Japanese trading companies were an exception, in my opinion because they were a classic value investment – cheap, with high free cash flow and return on equity. Warren was diplomatic to a Chinese investor, although it is clear from his past actions like selling Taiwan Semiconductor (TSM) and trimming BYD (BYD) that Charlie was the bigger China bull of the two. Regarding India, Warren acknowledged “there must be a lot of opportunities” but did not feel he had an edge to pursue them. He stated “more energetic management” might pursue those opportunities in the future. Considering Warren’s comments about Greg Abel’s energy level compared to his, it’s a good sign that Berkshire might widen its investment universe under the next administration. With so much foreign interest in Berkshire, as evidenced by the number of non-US questioners at the meeting, it is clear that the company enjoys much goodwill outside the US and could be a bigger player if they want to.

That brings us to another piece of new information from the meeting, that Warren’s view on responsibility for Berkshire’s future investment management has evolved. He now believes the CEO (Greg) should be in charge of capital allocation. The Ted and Todd experiment seems to be ending. After praising them in the early days of their time at Berkshire, we now hear nothing from Warren about them, except for Ted’s management of Geico, where he appears to be making some progress.

It ultimately remains a question for Greg and the board to decide how Berkshire will manage its investment portfolio in the future, but we may see further simplification of the portfolio with continued trimming of small positions and a wider territory for “elephant hunts”.

Capital Management

The cash raised in the Apple and Paramount sales almost matches the growth in Berkshire’s cash and T-Bill position, up $19 billion sequentially to $182.3 billion. The cash now exceeds the insurance float liability, which declined $1 billion sequentially to $168 billion. Warren stated that Berkshire “only swings at pitches we like” and expects the cash hoard to grow above $200 billion this year. This is not a terrible choice at T-Bill rates of 5.5%, but Warren noted he would still maintain the cash hoard if interest rates declined. At some point it becomes value destructive to hold that much cash, especially in an inflationary environment. The prospect of Berkshire widening its investment opportunity set under future management is a positive. Also, during the lunch break, board member Ron Olson noted on CNBC that the board is “not ruling out” a dividend after Warren’s tenure. While the tax inefficiency of a dividend detracts from shareholder value, so does holding cash earning an interest rate less than inflation while the company pays tax on the interest anyway.

Berkshire generated $6.17 billion of free cash flow in Q1, an improvement from $4.98 billion in Q1 2023. Operating cash increased $1.87 billion, while capex also increased $0.68 billion. Berkshire also raised cash by selling or redeeming at maturity $6.6 billion from its bond portfolio. The company used this cash by buying back $2.6 billion worth of Berkshire stock, $2.7 billion in new stock purchases, $2.6 billion on the final tranche of Pilot, and paying off about $4.6 billion of debt.

The share buybacks in Q1 were at a slightly lower pace than FY 2023. If annualized, they represent 1.2% of Berkshire’s market cap. So far in Q2, buybacks have been minimal, at just 454 A share equivalents, or 0.03% of market cap. It is notable that from December through March, the buybacks have been in the form of A shares only. As discussed during the meeting, just before and after the lunch break, Berkshire is buying blocks of A shares from long-time shareholders who are then making large donations for philanthropic purposes.

Operating Businesses

As I mentioned at the start, many of the operating trends in Q1 have been similar to the past several quarters, so I refer you to my earlier articles for more details. The most interesting thing out of the shareholder meeting about management of the operating businesses is that Warren rarely takes calls from operating managers anymore. These now go straight to Greg or Ajit. Also, in contrast to Warren’s former boasts of “laziness” when it comes to addressing performance issues in the businesses, he noted that Greg is more likely to address operating managers “coasting”. This is another positive for the future of Berkshire. We only got one question about BNSF in the meeting, which yielded slightly more details on the railroad, but still not enough. Greg noted that following the supply chain disruptions of 2022, BNSF was slow to trim costs in line with changing demand. These cost cutting efforts are underway, though the low demand growth is also a problem that was not discussed. Looking at the other three US-based Class 1 railroads, CSX (CSX) and Union Pacific (UNP) had much less of a revenue decline than BNSF and Norfolk Southern (NSC). When it comes to profitability, BNSF declined less than the two eastern railroads, but lost ground to its western peer Union Pacific.

Author Spreadsheet

At Berkshire Hathaway Energy, operations continue to be overshadowed by litigation over wildfires in Oregon with plaintiffs looking for a big payout:

As of March 31, 2024, amounts sought in the complaints and demands filed in Oregon and in certain demands in California approximated $7 billion, excluding any doubling or trebling of damages included in the complaints and those settled.

Again, I strongly encourage rating Note 23 of the 10-Q for all of the new developments in these cases, which Berkshire plans to contest vigorously.

During the meeting, Warren and Greg made clear that it is unsustainable for governments to hold utilities 100% responsible for fire damage and expect them to continue operating in their jurisdiction.

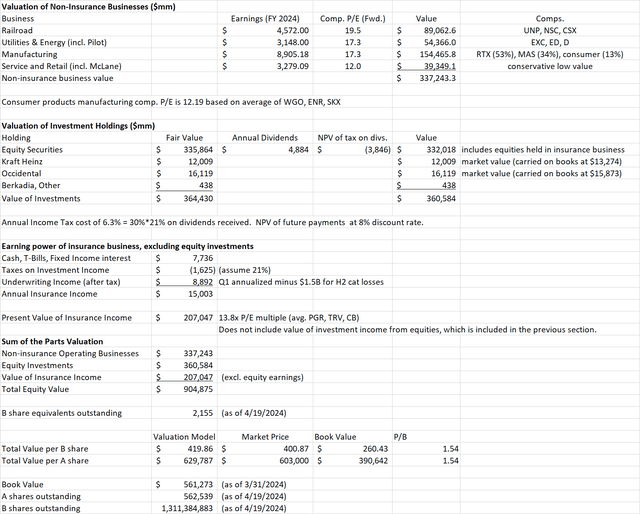

Valuation

My regular sum of the parts model has been updated. I am now using annualized Q1 results as estimates for FY 2024 segment earnings, however I have subtracted $1.5 billion from the annualized insurance underwriting income to account for large catastrophic losses like hurricanes in the second half of the year. (There have been zero cat losses so far this year. There were about $1 billion in 2023 and $2 billion each in 2021 and 2022.) In the non-insurance businesses, I recognize that annualizing the Q1 results may be conservative, but given the problems at BNSF and BHE, I think this approach is warranted.

Author Spreadsheet

While the value of the non-insurance business has come down and the value of the insurance business has come up, there was almost no change in the overall valuation. This came out to $419.86 per B share, compared to $419.17 last quarter.

Looking at price/book ratio, the slight increase in book value since last quarter combined with the slight drop in share price has taken P/B down to 1.54. This is back under the 1.6 threshold where I consider the stock richly valued.

Conclusion

Perhaps the passing of Charlie had focused Warren more on preparing for the future of Berkshire, but this year’s annual meeting provided more insight than usual about what investors can expect. Greg Abel will be a more active manager than Warren has been, taking more responsibility for investment management than previously thought. Greg may even venture more into international investment opportunities to give Berkshire a better chance to deploy the still-ballooning cash hoard. Greg is also taking a more active role in managing the operating businesses. We are gradually seeing more candor about problems at BHE and BNSF but solving them could be a multi-year effort.

Berkshire share price has declined slightly over the past quarter, while my estimate of intrinsic value has stated the same and book value has increased slightly. This is enough to nudge Berkshire stock back into Buy territory, along with the prospects of more engaged upper management in the future.

")