Q1 2024 Earnings Call Transcript")

(NYSE:TWLO)")

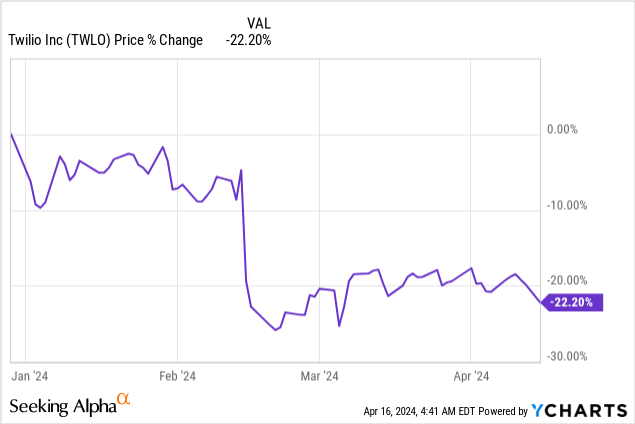

Twilio (NYSE:TWLO), despite seeing slowing top line growth in FY 2023, also achieved a small improvement in its dollar-based net potential rate, a vital monetization figure that indicates potential for organic revenue growth. Twilio’s shares skidded 22% year-to-date after the cloud-based communications platform presented its Q1’24 revenue guidance and they have not yet recovered. Considering that Twilio is still growing its enterprise customer base, seeing an uptick in its dollar-based net expansion rate and that the valuation is now much more attractive than during the pandemic period, I believe Twilio has potential for a rebound in FY 2024!

Previous rating

I rated shares of Twilio a hold in November 2023 because the company saw headwinds to its top line growth which fell into the single-digits: Twilio Has A Growth Problem. While slowing revenue growth is a problem, obviously, the company in the fourth-quarter saw a slight increase in the dollar-based net expansion rate which is a key monetization figure for Twilio. Considering that Twilio is also seeing growing gross profits and the company’s valuation multiple has compressed down to a more sensible range, I am changing my rating from hold to (speculative) buy.

Revenue trajectory and outlook for FY 2024

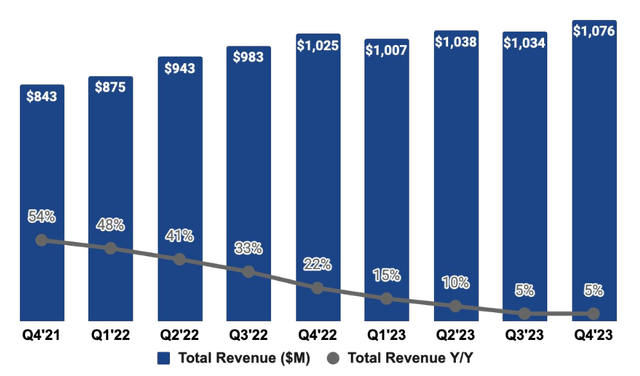

Twilio’s shares were crushed after the cloud company presented its outlook for the first-quarter in February which disappointed investors at the time and shares of Twilio still have not recovered from this sell-off. Twilio generated 5% year over year top line growth in Q4’23 and guided for total revenues of $1.025B to $1.035B in the first-quarter — implying a year over year growth rate of 2-3% — indicating that the post-pandemic slowdown is expected to continue. With a continual slowdown in its top line growth expected for the first fiscal quarter, investors have grown even more concerned about the communication platform’s growth trajectory. However, Twilio is seeing positive growth in its gross profits and has seen an encouraging uptick in its dollar-based net expansion rate.

Twilio

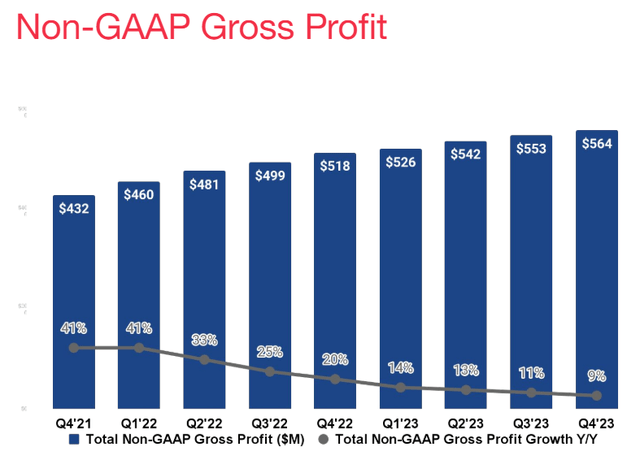

While Twilio’s revenue growth is slowing, its gross profits are growing. In the fourth-quarter, Twilio’s gross profit grew to $564M which implies a 9% year over year growth rate. Although this was the slowest quarterly gross profit growth in years, a growing gross profit trajectory shows healthy underlying business trends, especially because Twilio’s enterprise customer base is growing. At the end of FY 2023, Twilio had more than 305k customers using its products and services which compares against a total customer count of approximately 290k at the end of FY 2022.

Twilio

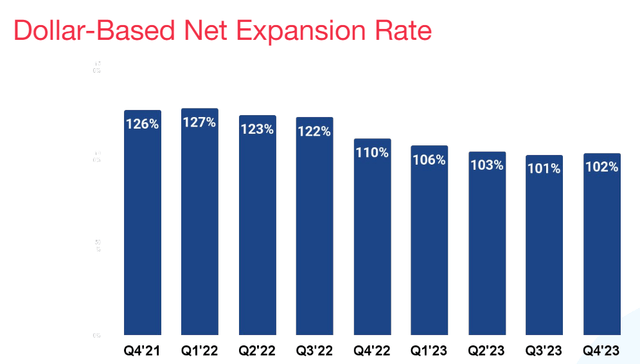

One metric that improved slightly in the fourth-quarter and which is the reason for my rating change, together with the massive price drop this year, is that the company’s dollar-based net expansion rate has seen a slight uptick in the last quarter. The dollar-based net expansion rate is a key monetization figure that shows companies by how much an existing customer cohort is increasing platform spending over time.

The DBNER figure is a key performance metric and is used to judge a company’s organic revenue prospects: a dollar-based net expansion rate below 100% obviously means that the company’s revenue base is shrinking, which would be a major red flag. In Q4’23, Twilio broke a down-trend in its DBNER figure and the company saw a 1 PP improvement to 102%. Continual growth in the DBNER measures could be a key catalyst for shares of Twilio going forward.

Twilio

Twilio’s valuation

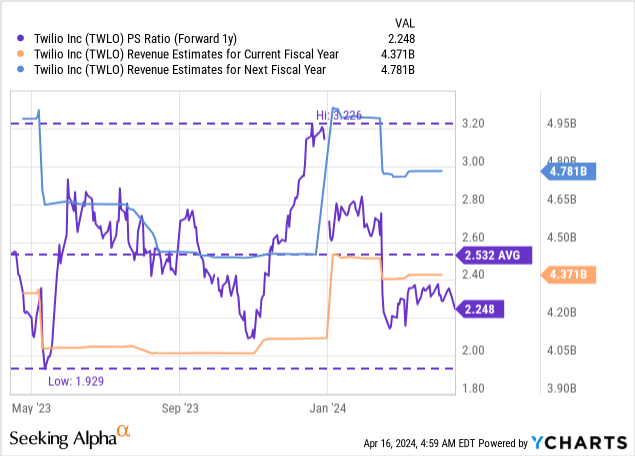

Cloud-based companies are not cheap as they are valued chiefly based on their potential for future revenue growth (which is why I am using a price-to-revenue ratio to value Twilio). Since Twilio’s top line growth rate has consistently moderated after the COVID-19 pandemic, however, investors are now in a position to buy into Twilio at a much more sensible valuation. Twilio is expected to generate $4.4B in revenues in FY 2024 and $4.78B in FY 2025 which implies top line growth rates of 5% and 9% year over year. Shares of Twilio are therefore valued at a forward P/S ratio of 2.2X which is below the 1-year average P/S ratio, indicating that the February drop may have gone a bit too far.

I believe shares of Twilio could easily revalue to 2.5X revenues which implies 13% upside revaluation potential. I believe this revaluation could take place under the condition that gross profits keep rising and that the company continues to repurchase shares: Twilio announced a $1.0B buyback last year and has been steadily buying stock in the open market. With a 2.5X P/S ratio, shares of Twilio have a fair value of $67. This is a dynamic number and it may rise or fall based off of Twilio’s progress in terms of growing its top line and improving its DBNER figure.

Risks with Twilio

The biggest commercial risk for Twilio, as I see it, relates to the company’s organic revenue potential as well as its net expansion rate. A drop of the DBNER figure below 100 percent would indicate serious organic revenue headwinds in which case the company’s valuation factor would likely also take a major hit. If the DBNER trend reverses in the next several quarters, the company may face more serious top line challenges.

Final thoughts

Twilio’s shares have not yet recovered from the fourth-quarter earnings-related drop. However, Twilio is still growing its revenues, expanding its footprint in the enterprise market and it has seen a 1 PP rebound in the dollar-based net expansion rate in the fourth-quarter. Together with a growing gross profit trend this is encouraging. Given that shares are now selling at a much more sensible valuation factor compared to the pandemic period, I believe the risk profile has improved considerably since February and I rate shares of Twilio a (speculative) buy!

")

")