")

")

As the U.S. dollar’s value becomes less attractive from nearly $35 trillion in mathematically unpayable Treasury debt, investors should be searching for ways to diversify their portfolios overseas. One of my top foreign picks right now is the Ambev S.A. (NYSE:ABEV) ADR, the largest beer brewer in South America and the 3rd biggest brewer in the world for volume sold, next to parent company Anheuser-Busch InBev (BUD), which owns 61% of ABEV, and Europe’s Heineken N.V. (OTCQX:HEINY) (OTCQX:HINKF).

My thinking is Ambev’s clear undervaluation setup currently, crossed with a weaker U.S. dollar over time, could support a dramatic increase in the share quote over 2-3 years priced in our local currency. Don’t laugh, but a double or triple in price, producing a far better total return with today’s high 6.5% dividend payout, is worthy of serious investor consideration.

In my research and trading experience, owning a stock supported by two understandable catalysts reduces the long-term risk of being wrong. And, having two horses pulling in the same direction multiplies your chances for outstanding future investment performance. Let’s review the Ambev buy proposition.

Ambev Website – Beer Brands, April 28th, 2024

Weak Dollar Argument to Own Foreign Equities

Last year, the BRIC nations (Brazil, Russia, India, China) were rumored to be close to creating a new trading-bloc currency backed by gold to compete with the U.S. dollar. My view is dedollarization in international trade will be a continuing theme over the next decade, especially since the U.S. government remains uninterested in cutting oversized deficit spending (unable to actually).

As I have explained for several years, I am worried any well-meaning effort to raise taxes or cut federal spending will only INCREASE the deficit, as the economy is now dependent on massive government support. It’s almost mathematically inevitable a government plan to reduce the deficit will backfire with a recession. That’s how bad our fiscal position has become. In the end, America is now stuck between (1) rising inflation and regular dollar devaluations to soft default on our debts (pay back Treasury debt with more worthless currency each year), and (2) the risk of a hard default (miss interest payments or maturity deadlines for debt repayment), including a depression in economic activity from which America many never fully recover. How would you choose if these are truly the last two options on the table?

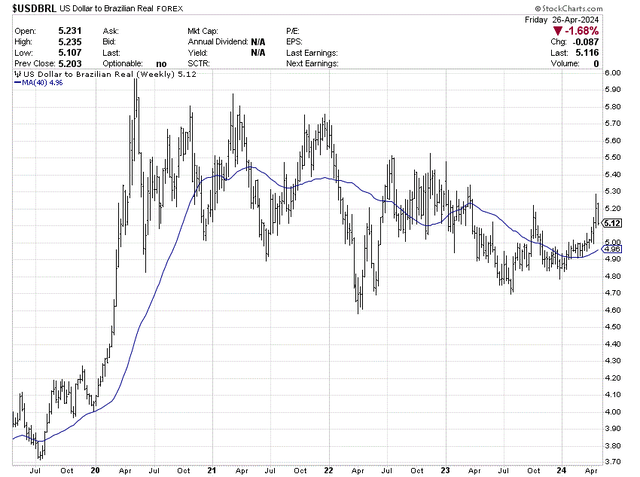

Already, the Brazilian Real (or Reais) currency has been steadily gaining ground on the dollar since the height of pandemic fears in the middle of 2020. Below is a chart of the dollar losing ground to Brazil’s currency over the last four years, following substantial dollar advances during the early days of COVID economic shutdowns. In the end, a weakening U.S. dollar may be the best macro excuse to own assets outside of America, denominated in overseas currencies. Today, $1 USD is exchanged for $5.12 BRLs.

StockCharts.com – U.S. Dollar vs. Brazilian Real Currency, Weekly Exchange Rate, 5 Years

Ambev’s Bargain Valuation

Ambev’s operations are not growing much. So, investors have slowly retreated from ABEV shares. Today, the company is sitting at one of its cheapest valuations in the past 20 years, similar to the recession lows during 2009 and 2020. In addition, the trailing dividend yield of 6.5% is the highest in the brewery and distilled beverage industries globally and represents the greatest positive spread ever vs. the S&P 500 index’s cash yield.

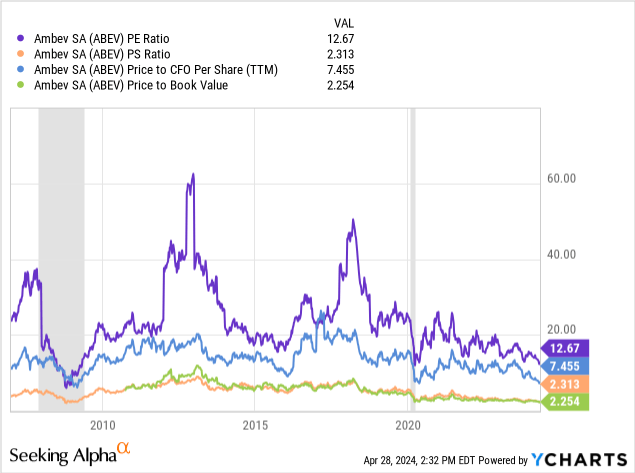

Below is a chart of several basic financial ratios, looking at price to trailing earnings (12.7x), sales (2.3x), cash flow (7.46x), and book value (2.26x). For a similar valuation backdrop, you have to go back to the depths of the 2020 and 2009 recessions.

YCharts – Ambev, Basic Valuation Stats, Since 2007, Recessions Shaded

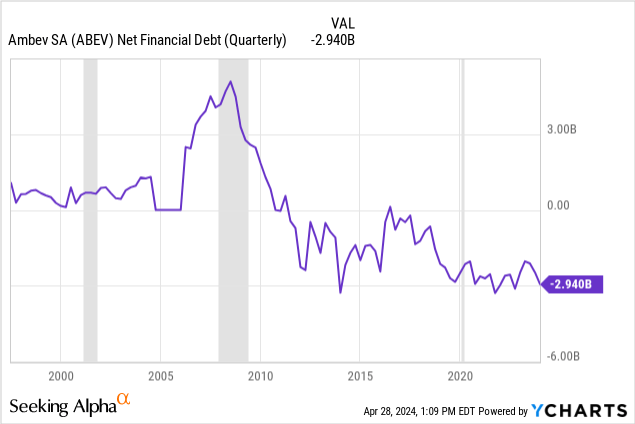

When we include the fact Ambev is conservatively run, with more cash than debt (net US$3 billion in cash), the enterprise valuation stats are even more eye-opening on ABEV’s bargain situation for new investment.

YCharts – Ambev, Net Financial Debt, Since 1997

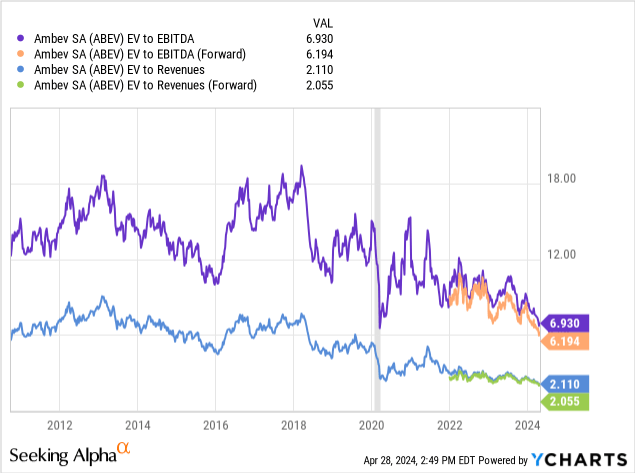

On EV to “forward” cash EBITDA (6.2x) or Revenues (2.06x), Ambev is selling at a 10-year low, beneath the 2020 pandemic-bust valuation, while approaching 2009 Great Recession levels! Where else can you find a blue-chip company in the world, with a conservative balance sheet and stable business model, selling as cheaply? Answer: they are hard to find.

YCharts – Ambev, Enterprise Valuations, Since 2011, Recession Shaded

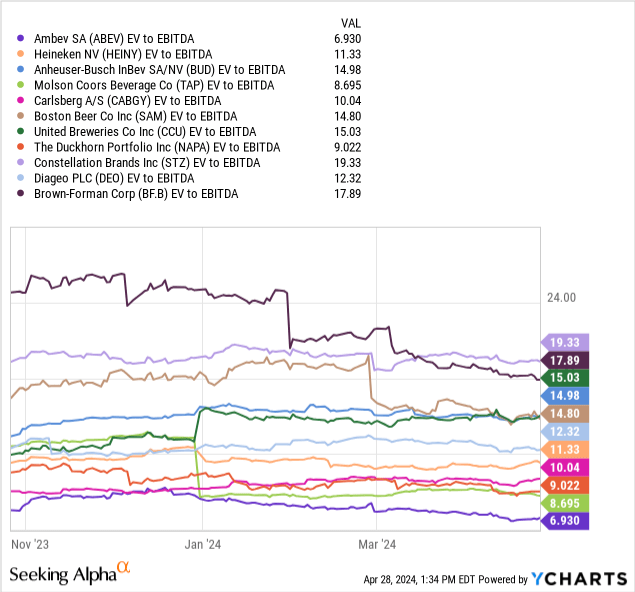

Using trailing enterprise valuation data, ABEV is far and away the least expensive beer brewery or liquor distiller of the major investment alternatives around the world. My sort group includes Heineken, Anheuser-Busch InBev, Molson Coors (TAP), Carlsberg A/S (OTCPK:CABGY), Boston Beer (SAM), Compañía Cervecerías Unidas S.A. (CCU), The Duckhorn Portfolio (NAPA), Constellation Brands (STZ), Diageo plc (DEO), and Brown-Forman (BF.B).

YCharts – Ambev vs. Major Breweries & Distillers, EV to EBITDA, 6 Months

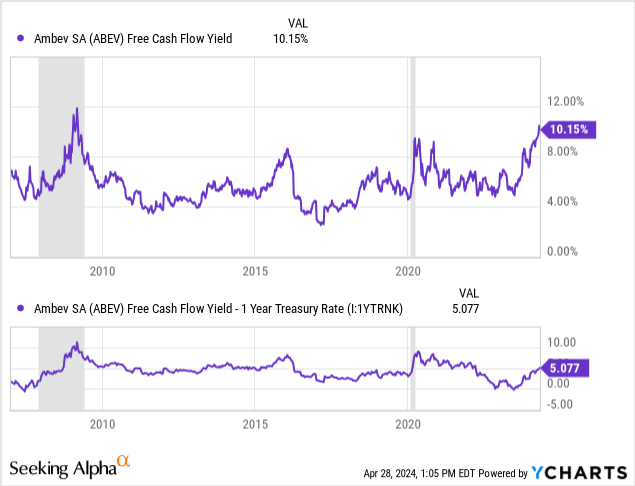

Even better news for investors, free cash flow yields above 10.1% from an old-school blue chip are incredibly rare to find in April 2024. This number is again the highest equivalent yield since the 2009 global recession. Plus, against 5%+ cash investment yields on CDs and U.S. T-Bills, Ambev’s free cash flow return on investment number is well within acceptable ranges. On the contrary, most U.S. large caps are selling for free cash generation yields at or under the 5% level. I’ll take a hard pass on those ideas. [Note: Brazil’s inflation rate is under 4% YoY currently and falling for a trend.]

YCharts – Ambev, Free Cash Flow Yield vs. U.S. 1-Year Treasury Rate, Since 2007, Recessions Shaded

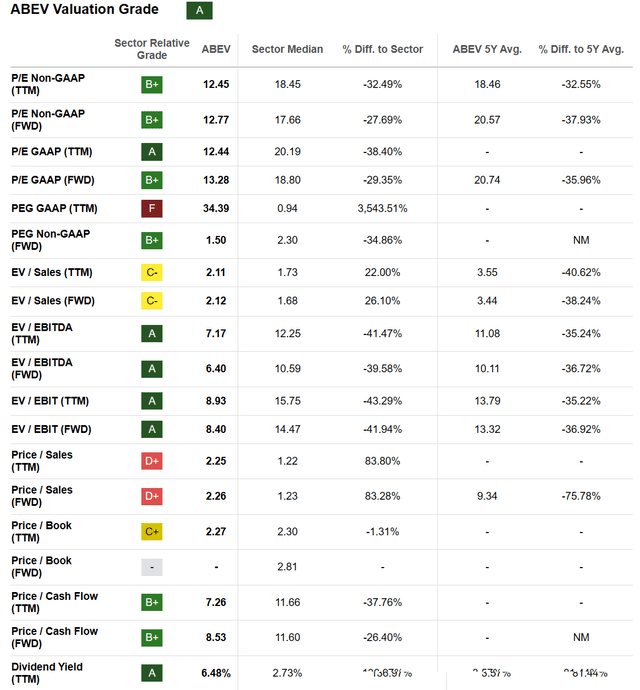

Seeking Alpha’s computer ranking system gives ABEV an “A” Quant Valuation Grade. I would argue an A+ score might be more appropriate, after taking into account minor financial debt vs. large cash holdings on the balance sheet, with impressive gross profit margins of 50%+.

Seeking Alpha Table – Ambev, Quant Valuation Grade on April 27th, 2024

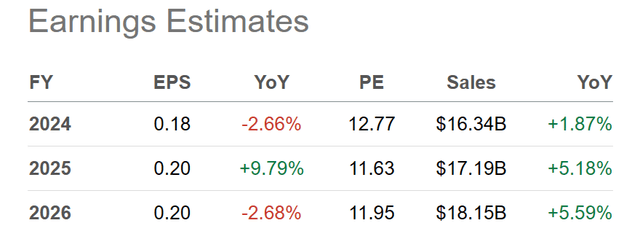

Ambev’s low valuation setup can partially be blamed on stagnate growth forecasts, which you can review below. However, unless individuals quit drinking beer in Brazil, the company’s stable future is quite desirable if the world economy hits recession soon, or market volatility forces investors to move money into defensive food/beverage names.

Seeking Alpha Table – Ambev, Analyst Consensus Forecast for 2024-26, Made April 27th, 2024

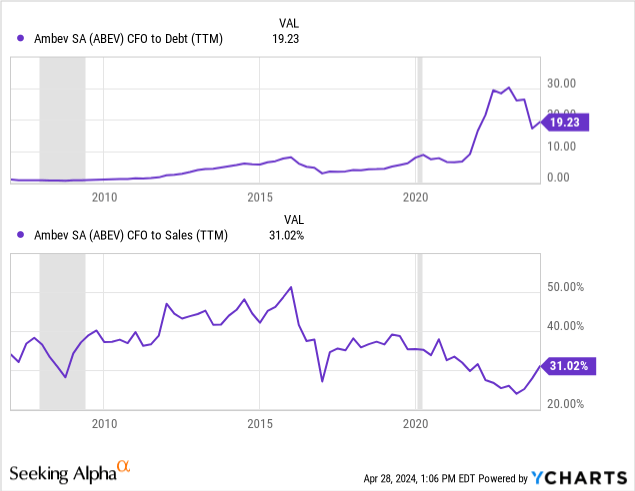

Other statistics to weigh include the positive financial flexibility provided by high cash flow generation vs. total debt, alongside the negative development of slightly less (and sliding) cash flow on sales over time.

YCharts – Ambev, Cash Flow to Debt & Sales, Since 2007, Recessions Shaded

Appealing Dividend Story

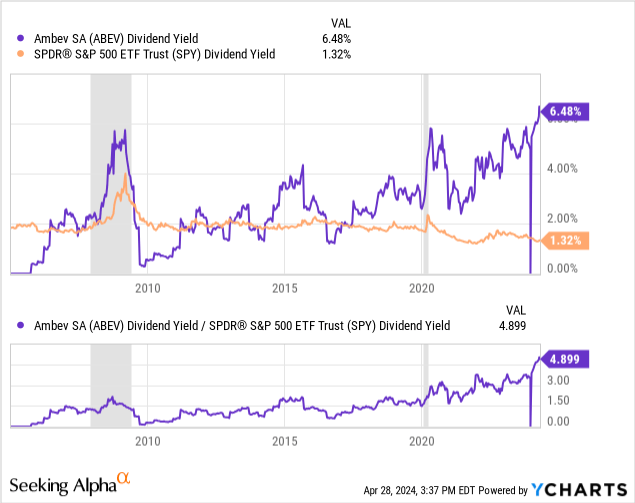

Perhaps the main attraction for me is Ambev’s robust dividend payout. At 6.48% for yield, the cash distribution over the last year on today’s share price is the best nominal rate since the company began paying dividends in 2006. It’s also the strongest yield proposition on a “relative” spread basis to the S&P 500 index. ABEV’s yield is almost 5x the prevailing rate of the U.S. blue-chip equity market. Both ideas are presented below.

YCharts – Ambev Trailing Dividend Yield vs. S&P 500 ETF, Since 2005, Recessions Shaded

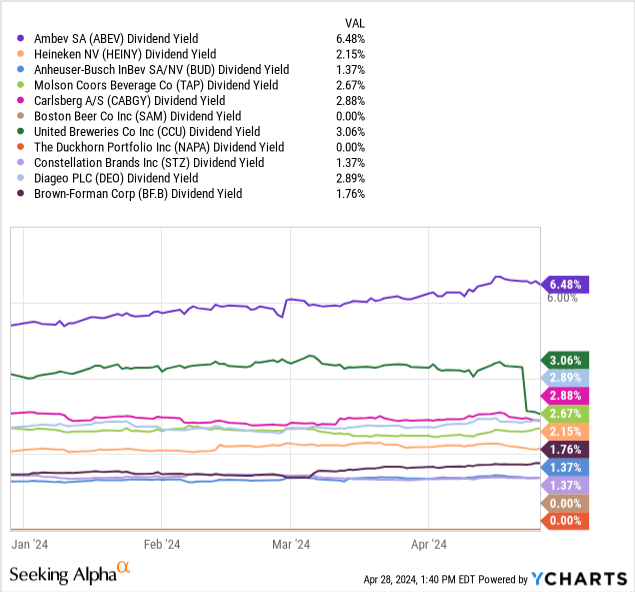

Not to be outdone, Ambev’s yield is also the highest of the peer brewery and distiller group. If you are searching for a great income investment, with sales originating outside the U.S., a sound balance sheet, terrific profit margins (final after-tax margin of 18% on sales presently), and popular beverage brand names for products, ABEV stands out today as a real bargain with future investment win potential.

YCharts – Ambev vs. Major Breweries & Distillers, Dividend Yield, 4 Months

Final Thoughts

Ambev represents a unique foreign investment with a defensive and conservative flair. It appeals to both value and income/yield investors alike. The stock’s ultra-low valuation and tailwind of coming U.S. dollar devaluations should support a much higher share price over time, as you collect a tremendous dividend payout while you wait.

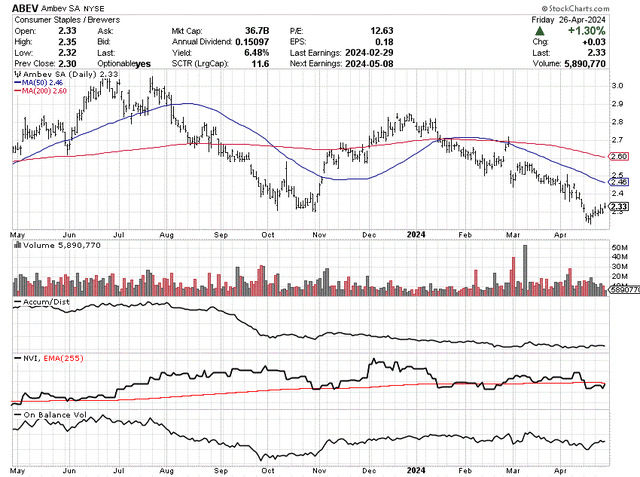

I will say the technical chart pattern for the stock is not very impressive. Slowly declining price has been driving the valuation ever lower, as business results have held their ground. Some bullish trading transition is evolving. Many momentum indicators either bottomed in late October or have held up better since, including the Accumulation/Distribution Line, Negative Volume Index, and On Balance Volume. So, new price lows during April are really not being “confirmed” in my trading trend work. It appears to be a period of smaller retail investors capitulating and leaving shares.

StockCharts.com – Ambev, 12 Months of Daily Price & Volume Changes

What are the downside risks of owning Ambev? The primary bearish catalyst would be a material decline in the Brazilian real currency vs. the U.S. dollar. Basically, the economic outlook and government fiscal spending situation would have to deteriorate beyond what’s taking place in America. Currently, the IMF is projecting Brazil GDP growth of +1.5% for 2024 vs. +2.7% in the U.S. for 2024, and federal spending deficits of 0.6% of GDP in Brazil vs. rates beyond 6% for the U.S.

A second risk to worry about would be the appearance of global financial turmoil and another recession. Such would undoubtedly put pressure on Ambev operating results, while adding sell volumes to share supply. Nevertheless, because the ABEV stock valuation is so cheap and already approaching recessionary levels, I would fully expect any bear market in equities to drive down the pricing for other equities at a dramatically greater pace. In this regard, I am projecting the Ambev setup should nicely outperform the Big-Tech heavy S&P 500 index in a bear market scenario.

I am modeling a worst-case bearish outcome as unlikely to hold price below US$2.00 a share for long. Such would deliver -10% for a total return, including expected dividends, over the next 12 months. All other variables remaining the same, sub-$2 quotes would bring the cheapest valuation since the company was formed in 1999 (when two breweries merged), using the combination of variables discussed in this article.

Conversely, the upside potential for Ambev is quite material. Just to get back to 10-year average financial ratios on earnings, EBITDA, sales, and cash flow, a return move to $4.00 may be in order. At this price, new investors today could achieve a total return close to +80%. Then, if the dollar declines appreciably and the Brazilian economy outperforms the U.S., price targets of $5 or even $6 come into focus a few years out. Total returns of +150% to +200% are not out of the question over 2-3 years.

Putting all the ideas together, risk-reward analysis is now highlighting oversized bullish odds, with minimal downside risk given more bearish economic outcomes. I rate shares a Strong Buy and I am looking to build a position over the coming weeks.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

(WCC)")