")

")

SunCoke Energy, Inc. (NYSE:SXC) recently provided information about a new coke contract with Cleveland-Cliffs (CLF), potential completion of the foundry coke expansion project, and long-term contracts. Given the recent increase in EPS expectations delivered by several analysts, 3.69% dividend yield, and recent debt reduction, SXC could bring surprises in the coming years. There are risks from changes in the environmental laws and changes in the price of coke, however I think that SXC is cheap at its current price mark.

SunCoke

With more than 60 years of activity dedicated to the exploitation and manufacture of carbon coke on the American continent, SunCoke is an independent company that currently has five high-voltage furnace facilities for the treatment of coal and the manufacture of coke.

Added to these facilities are the design and operation rights that it maintains with ArcelorMittal Brasil S.A. (MT) for the manufacture of coke in Brazil, adding additional 1.7 tons to its annual production capacity. Additionally, the company operates a logistics business related to the trade of steel, coke, and products used in electric power generation and coal processing, with terminals located in the Gulf Coast and East Coast regions.

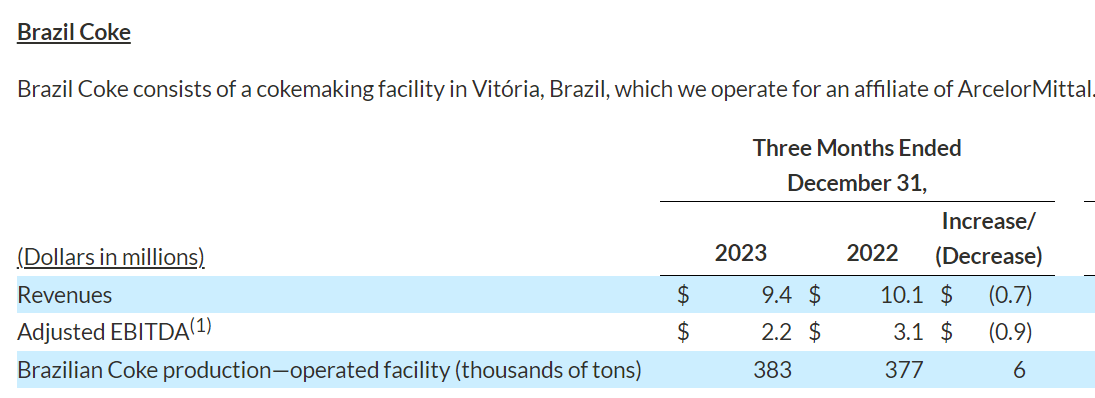

In Brazil, the entire production is destined for a single client, ArcelorMittal Brasil, with whom it maintains an agreement for the management of coal processing facilities for the production of coke in the hands of the Brazilian company. I believe that ties with ArcelorMittal may bring the interest of investors as it is a well-known player in the industry.

Since the agreement with the Brazilian company for the administration of the Coke production facility in this region, the company’s segments have been divided into three. One segment responds exclusively to the activity in Brazil, another segment responds to the activity in the United States and its five processing plants, and the third segment is intended for the management of the logistics business.

In the last quarter, SunCoke reported an increase in the Brazilian coke production, but quarterly revenue did not increase. I am not concerned about these figures because I believe that the expectations of market participants and guidance, which I am discussing in this article, do not appear pessimistic.

Source: Press Release

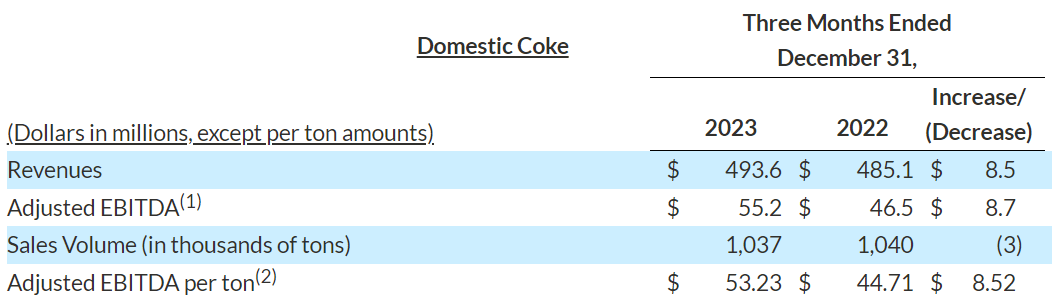

Without a doubt, the segment dedicated to domestic coke processing is the largest in the company, and has the particularity that some of its facilities maintain contracts with other companies for the sale of their total production capacity on an annual basis. In the last quarterly report, SunCoke reported an increase in the Adjusted EBITDA per ton as well as quarterly revenue.

Source: Press Release

On the other hand, the logistics segment is intended for the transportation of merchandise associated with this industry as well as offering the mixing service of some products. It has a hybrid model between truck transportation, train transportation, and ship transportation. In this sense, the company has some advantages since, for example, in the case of the Indiana terminal, it has direct access to railways with a transport capacity of 15 tons annually.

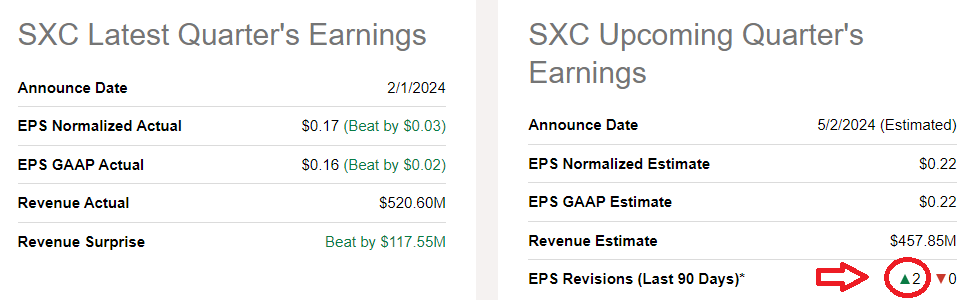

Recent Earnings Surprise And 2024 Guidance Appear Optimistic

In the last quarter, SunCoke reported better than expected EPS GAAP and net sales better than anticipated by analysts. I also appreciate quite a bit that the new EPS revisions in the last 90 days included increases in future expected earnings. In sum, I believe that analysts expect 2024 to be a beneficial year. Hence, I believe that it is a great time to review the company’s business valuation.

Source: Seeking Alpha

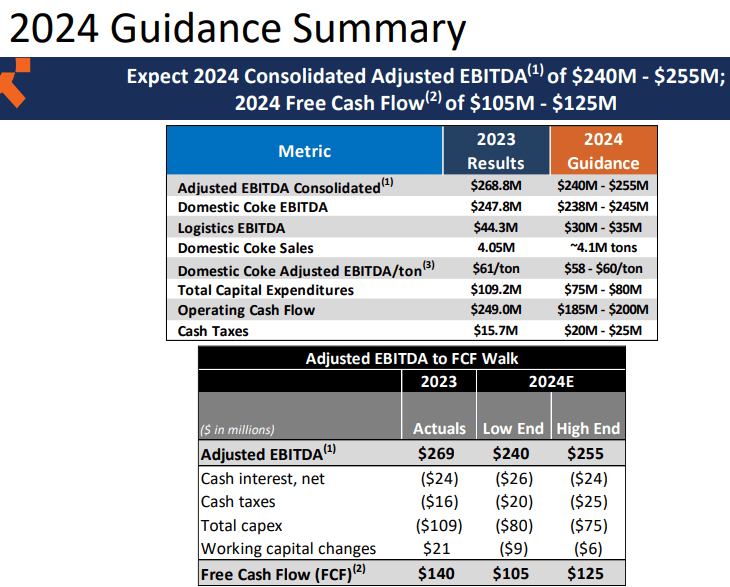

Guidance given for 2024 includes 2024 adjusted EBITDA close to $240-$255 million, CFO of about $185-$200 million, and 2024 FCF of about $105-$125 million. I did not use the same figures in my financial model, but my income statement expectations in my base case scenario include figures that are not far from those given by SunCoke.

Source: Quarterly Presentation

Balance Sheet

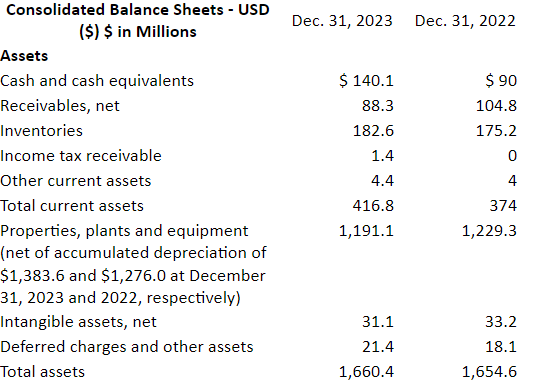

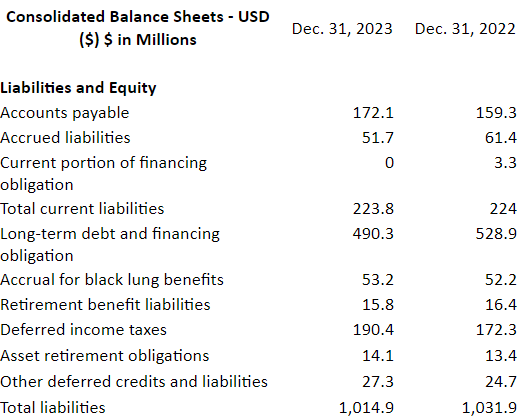

SunCoke reported an increase in cash in 2023. As of December 31, 2023, cash and cash equivalents stood at close to $140.1 million. Besides, inventories increased to close to $182.6 million, with total current assets of about $416.8 million. The current ratio stands at more than 1x, so I believe that there is not a liquidity problem. The largest asset is presented by properties, plants, and equipment, which stood at $1191.1 million, with total assets of about $1660.4 million.

Source: Press Release

I believe that the most interesting thing about the balance sheet is the recent reduction in debt, which SunCoke noted in its most recent quarterly report.

We are pleased with the progress we made on our capital allocation goals in 2023, notably reducing gross debt by approximately $44 million and increasing our quarterly dividend by 25%. Source: Press Release

Right now, long-term debt and financing obligations stand at $490.3 million, with retirement benefit liabilities close to $15.8 million as well as asset retirement obligations of $14.1 million. Finally, total liabilities stand at about $1014.9 million, and the asset/liability ratio is close to 1.6x. Hence, I believe that the balance sheet appears quite stable.

Source: Press Release

Assumption 1: Net Sales Growth From The Metallurgical Market May Enhance Future Net Sales Growth Under My Base Case Scenario

Given that the company has assured the distribution of its products from all its facilities during the year 2024, I expect that management may maintain an operation similar to that of 2023, also supported by the growing metallurgical industry in the United States and globally. According to experts, the metallurgical market could grow at close to 3.8% in the coming years. Under my base case scenario, I assumed that SunCoke would grow thanks to the growth of the market. I expect median revenue growth to be close to 7%. In my view, half of that revenue growth may be explained because of the growth of the market.

The global metallurgical equipment market size was USD 13120 million in 2020 and the market is projected to touch USD 16580 million by 2027, at CAGR of 3.6% during the forecast period. Source: Businessresearchinsights

The global metallurgical coke market is estimated at US$ 218.4 billion in 2024 and is projected to reach a size of US$ 325.78 billion by 2034-end, advancing at a CAGR of 3.8% between 2024 and 2034. Source: Factmr

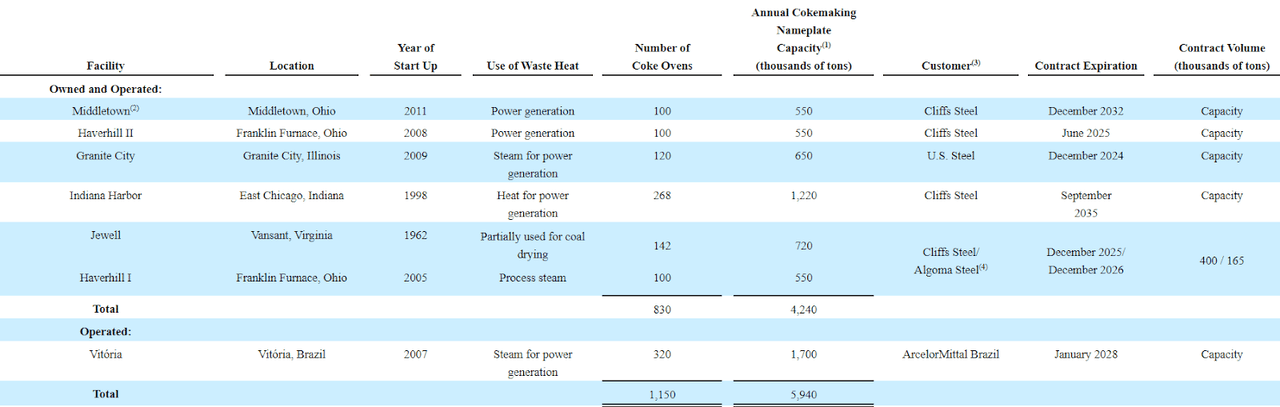

Assumption 2: Long-Term Contracts With Large Clients May Bring Consistent Net Sales

SunCoke reports long term agreements with many customers, assuring that the future production may be sold. The following is a table offered in the most recent 10-K.

Source: 10-k

In my view, long-term contracts mean recurrent net sales, which financial forecasters appreciate quite a bit. As a result, I believe that demand for the stock may increase as soon as more analysts review future production agreements. Under my base case scenario, demand for the stock may help lower future cost of capital.

Assumption 3: The Foundry Coke Expansion Project May Bring Economies Of Scale, More Capacity, And Net Income Growth

In the last press release, the company noted incoming increases in the foundry business, market participation expansion, and a new coke contract with Cleveland-Cliffs. Under my base case scenario, these increases in capacity and a new contract will most likely bring net income growth and dividend increases.

We continued to advance our foundry business by completing the foundry coke expansion project and expanding our market participation. Additionally, the extension of our Indiana Harbor coke contract with Cleveland-Cliffs for an additional 12 years positions our largest coke plant favorably for the future. Source: Press Release

Assumption 4: Research And Development Expenses May Improve Net Sales Growth

Considering the total amount of R&D activities noted by SunCoke and recent patents obtained, I would be expecting new innovations in the coming years. As a result, I believe that we could expect increases in net revenue. Under my base case scenario, I assumed that median net sales growth could increase in the coming years, close to 3%, thanks to R&D.

Our research and development program seeks to improve existing and develop promising new cokemaking technologies, including new product development, and enhance our heat recovery processes. Over the years, this program has produced numerous patents related to our heat recovery coking design and operation, including patents for pollution control systems, oven pushing and charging mechanisms. Source: 10-K

Base Case Expectations Based On Previous Assumptions And Successful Initiatives Initiated By SunCoke

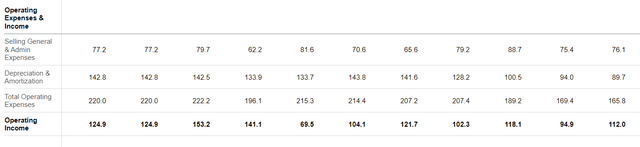

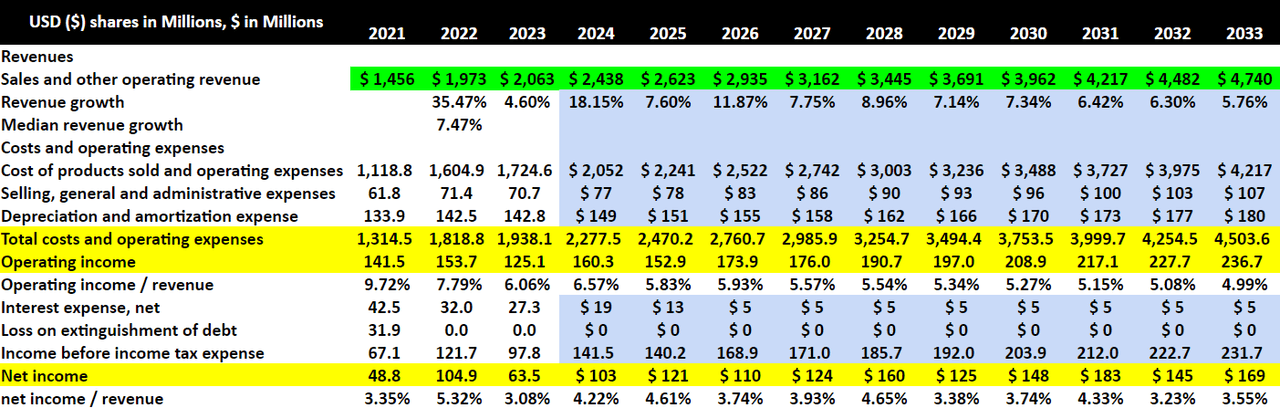

Under this scenario, I included 2033 sales and other operating revenue close to $4740 million, with cost of products sold and operating expenses of about $4216 million as well as selling, general, and administrative expenses worth $106 million. My figures are in line with the revenue estimates offered by other analysts, but I believe that I am bit more pessimistic.

Source: Seeking Alpha

In addition, taking into account 2033 depreciation and amortization expenses of $180 million, total costs and operating expenses stand at $4503 million. Finally, operating income is close to $236 million, and the operating income/revenue ratio stands at about 4.99%. Note that my figures under this case scenario are not far from that reported by SunCoke in the past. The operating income/revenue included in my financial model is close to that reported by SunCoke recently.

Source: Seeking Alpha Source: Seeking Alpha

My figures also included interest expense of about $5 million and net income of about $168 million. The net income / revenue ratio stands at close to 3.5%, which is not far from the figures reported in the past.

Source: My Expectations

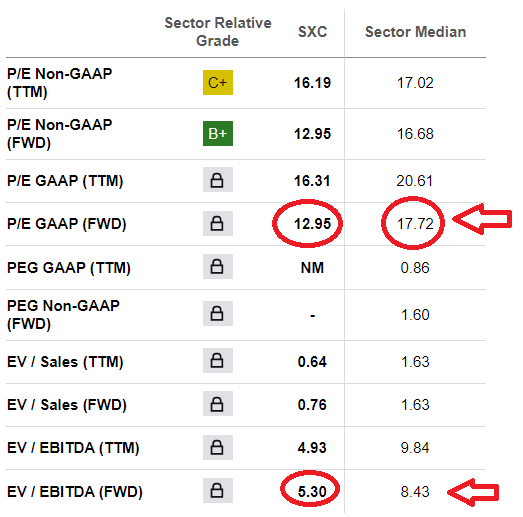

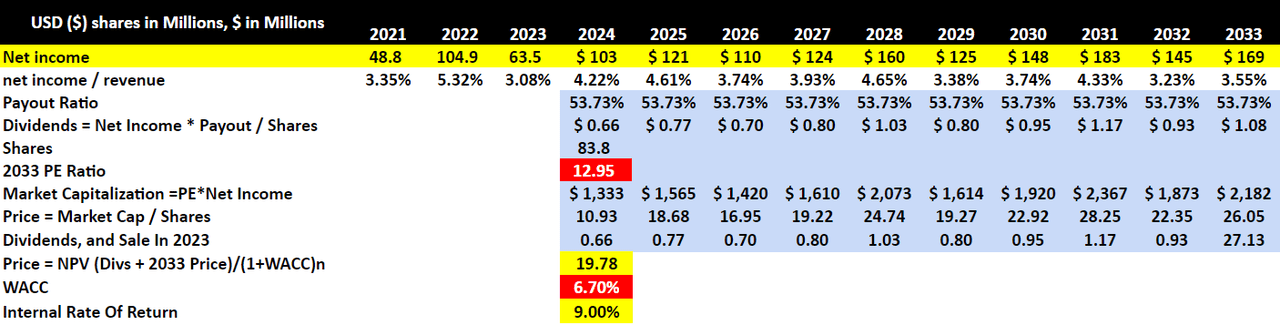

I am using a dividend discount model and a PE ratio to obtain the terminal value. For the assessment of the PE multiple, I took a look at the expectations of other market analysts and the current multiple. With these figures in mind, I believe that a PE ratio of 12.95x makes sense.

Source: Seeking Alpha Source: Seeking Alpha

If we also include a payout ratio of 53%, which is close to the current payout ratio reported, 2033 dividend would be close to $1.08. Hence, I am assuming an increase in dividends. By summing the future sum of dividends and the terminal value, I obtained an implied fair price of close to $19 per share. SXC is currency trading at $11, so I believe that there is upside potential in the stock valuation.

Source: My Expectations

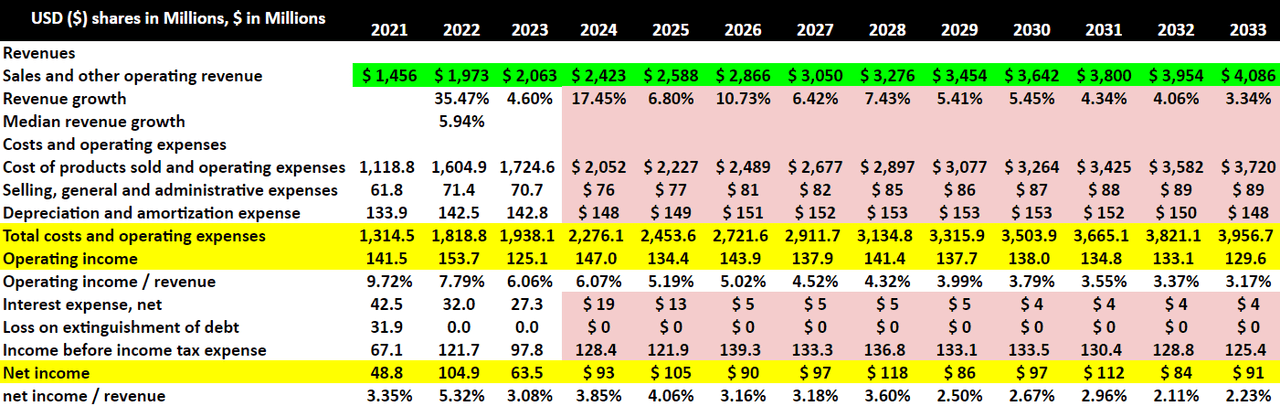

My Worst Case Scenario Includes Failed Initiatives Developed By SunCoke And Failed Assumptions

Under my worst case scenario, I assumed that the company would deliver lower net sales growth than that in the previous case scenario. Under this case, the assumptions made previously would fail, and the initiatives of SunCoke may also not be successful.

I included 2033 sales and other operating revenue of $4086 million, with median revenue growth of 5%, cost of products sold and operating expenses of about $3719 million, and selling, general, and administrative expenses close to $89 million.

Besides, with depreciation and amortization expense worth $148 million and total costs and operating expenses of about $3956 million, 2033 operating income would stand at $129 million.

The operating income / revenue ratio would stand at 3.1%, and with interest expense of $4 million, 2033 net income would be close to $91 million. Finally, the net income / revenue ratio would stand at 2.2%.

Source: My Expectations

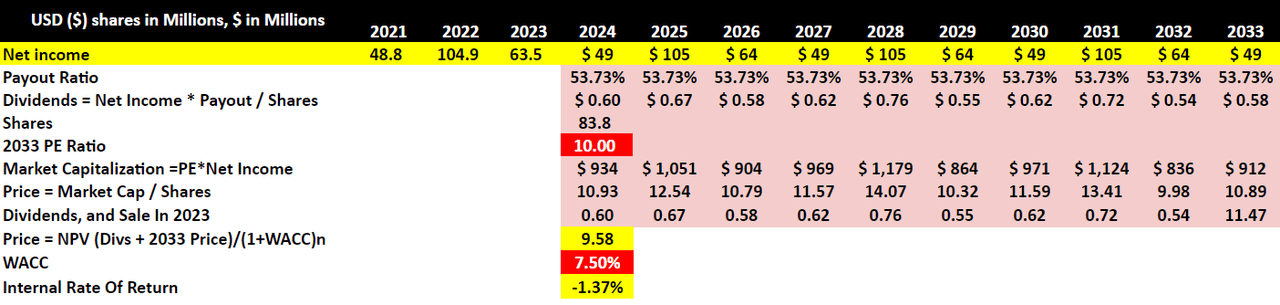

With a payout ratio of about 53%, I also included a 2033 PE ratio of 10x, which I believe is conservative. Note that under this case scenario, investors may sell shares, which may lower the demand for the stock, and lead to a lower PE ratio. I also included a WACC of 7.5% because lower demand for the stock could lead to an increase in the cost of capital. The results of my dividend discount model would include an implied price of $9.5 per share.

Source: My Expectations

Competitors

Regarding the domestic market, the company has great competitive advantages. It is the only company to build and remodel ovens for the treatment of Coke in the last 30 years, and during 2023, according to the last 10-K, 37% of the domestic market of Coke was in the hands of the company. Furthermore, due to the type of operation it maintains on the contracts, it currently has no competition for the sale of its products, although it will find it in the negotiation of future contracts when they reach their expiration date.

Risks

The concentration of clients that the company currently maintains is undoubtedly a risk factor since the loss of any of these would considerably affect its collection and the circulation of its product. On the other hand, it must be added that a large number of regulations are expected in the long term regarding pollution and environmental conditions around the activity that could affect current operations of the company.

Beyond the risks involved in maintaining an open acquisition strategy and the search for new assets to expand the company’s net income, I consider that there are no major risks in the short term if we rule out a possible economic crisis in the future. With that, the domestic market of the United States could lead to drop in demand mainly with regard to the logistics business, which is a small part of SunCoke.

Conclusion

SunCoke is currently working on a new coke contract with Cleveland-Cliffs and is completing the foundry coke expansion project. These developments could bring new capacity and may bring new recurrent revenue. If we also keep in mind the recent reduction in debt, the dividend payout, and the issuance of new patents, SunCoke appears to be a must-follow stock. Under my dividend discount model, I believe that the shares could be worth much more than the current valuation. Yes, even considering risks from new environmental regulations or changes in the price of coke, I believe that there is significant upside potential in the stock valuation.

")

")

Q1 2024 Earnings Call Transcript")