")

Dear readers,

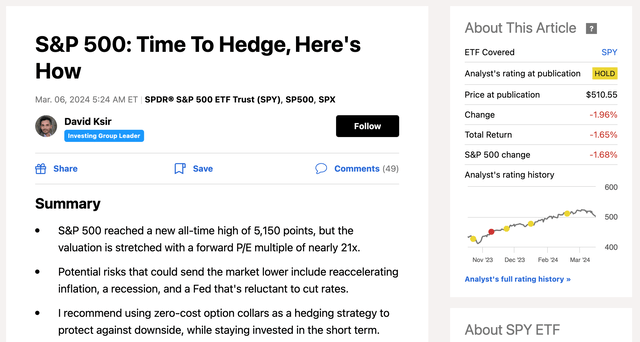

Last time I wrote an article on the S&P 500 (NYSEARCA:SPY), the index stood at 5,150 points. My view on the index had been short-term positive since November, mainly due to momentum, but because of a relatively expensive valuation at a forward P/E of nearly 21x, I remained medium to long-term bearish. My last article focused on potential risks that could result in a potential sell-off, including a risk of re-accelerating inflation, recession and a Fed reluctance to cut rates.

SA

I proposed a hedge by using a zero cost option collar. In particular, I hedged my downside at 5,050 points by buying a July 19th PUT. Simultaneously, I funded the position by selling (shorting) a July 19th CALL at a strike price of 5,400 points, and consequently gave up upside beyond this point. The hedge capped my downside at around 2%, while allowing for up to 5% of upside – a very favorable risk-reward.

Since that article, however, a couple of things have changed. Most notably, (1) we now have two more CPI reports (February and March) to look at, (2) the predicted timing of the first rate cut has moved to a substantially later date, and (3) the index has sold off to 5,022 points as of the time of writing this article – below the threshold of my PUT.

Why I’m bullish

Recent developments, which have caused the index to fall, have actually made me more bullish.

Here’s why.

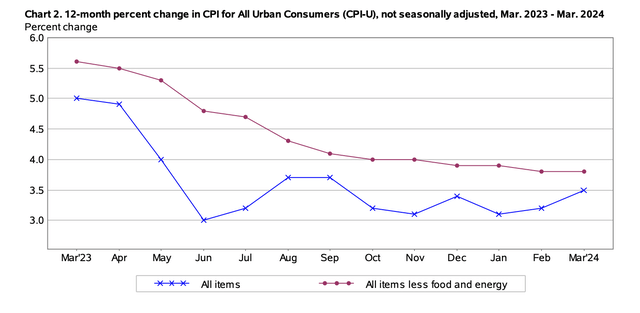

The latest March CPI came in (slightly) hotter than expected and marked the third report in the row that missed expectations. CPI in March came in at 3.5%, up from 3.2% in February. Core CPI which excludes the volatile food and energy prices came in at 3.8%, flat from the month before.

Bureau of Labor Statistics

The fact that CPI missed expectations and stubbornly remains above the Fed’s 2% target is obviously not great news, but if we look below the surface, we’ll see that we are actually quite close to declaring victory on inflation.

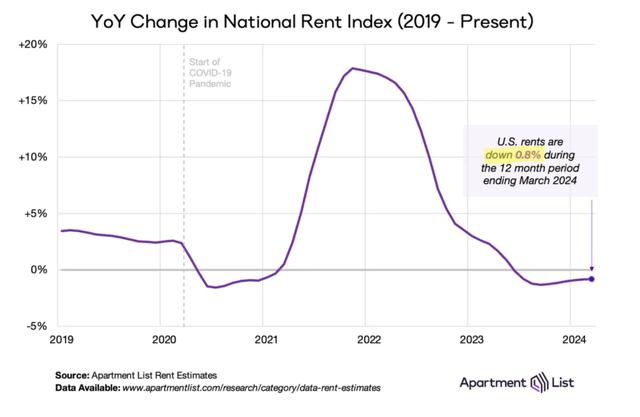

First off, and we’ve discussed this point many times, CPI continues to be skewed upwards due to shelter. Shelter CPI, which accounts for 36.2% of the overall weighting, was most recently reported at 5.7%.

Bureau of Labor Statistics

But the problem is that this measure is lagging and most real time measures of housing and rent prices are clearly showing little to no inflation in shelter. First, take rents, which the Bureau of Labor Statistics reports at 5.7% inflation while the National Rent Index shows a 0.8% decline in prices over the past 12 months.

Apartment List

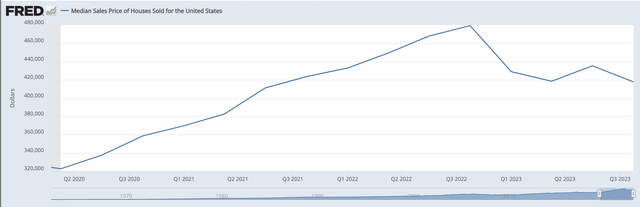

And second, home prices also fell on average over the past 12 months by about 2.5% YoY from a median price of $429,000 to $418,000.

FRED

This means that the lag in shelter effectively adds about two full percentage points (36%*5.7%) to headline CPI. In other words, taking real time shelter inflation of zero would yield overall CPI of 1.7%, well within the Fed’s target.

And there’s more. Another component that has, in my opinion, skewed the headline number is auto insurance. A weighting of 2.85% may not seem significant, but with a 22.2% year-over-year increase in prices, it’s enough to contribute a further 0.6% to headline CPI.

Bureau of Labor Statistics

And once again, the problem here is that the reported measure is lagging. The price of insurance is dependent on used car prices. The more expensive the car, the pricier the insurance. Used car prices have skyrocketed in 2021, but this increase has only started to translate into higher insurance prices recently because most insurance contracts are signed for a period of one or sometimes two years. As a result, auto insurance prices are amongst the most lagging in terms of inflation.

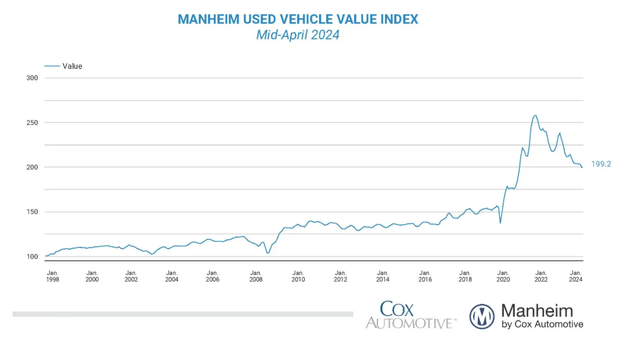

Manheim

And since we know from the latest CPI report that used car prices are actually declining, with a 2.2% YoY drop in March, it’s easy to predict that auto insurance rates will also decline, or at the very least stop increasing.

Bureau of Labor Statistics

Similarly to shelter, I believe that it’s only a question of time before auto insurance inflation trends towards the real-time measure, which is likely near zero. In the process, we should see headline CPI decline by a further 0.6% or as low as 1.1% subtracting the impact of shelter and auto insurance.

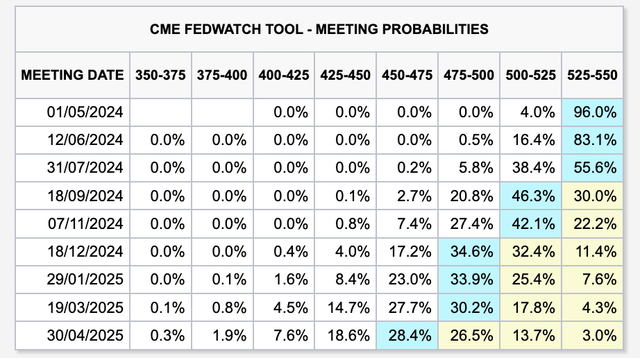

Recent misses of CPI expectations have spooked the market and also the Fed, which has moderated their interest rate cut expectations. Not long ago, many were expecting the first-rate cut as soon as March, but now trading activity implies that we are unlikely to see the cut before July (45% chance of a cut) or September (70% chance of a cut).

Fed Watch Tool

Given what we know about CPI being very likely to decline as low as 1.1%, I think the market has overreacted and as CPI declines further, cuts might actually come sooner than the market expects. This makes me quite bullish over the rest of the year, which makes me want to amend my hedge here to avoid giving up upside above the 5,400 points level.

I have little doubt that CPI will reach the 2% target this year, but even if it doesn’t, we should also not forget that following the change of the Fed’s mandate to FAIT (flexible average inflation targeting) the Fed could very well justify cutting rates above the 2% target.

How I’m modifying my hedge

Given my increased level of bullishness, I upgrade the S&P 500 to a BUY here at 5,020 points.

I also took advantage of the selloff to get rid of the short CALL from my zero cost option collar in order to keep all of my upside.

Author’s IBKR account – position from last article

Therefore, I buy a July 19th CALL with a strike price of 5,400 at a $41 premium. And, because I want to make the modification zero cost, I simultaneously sell (short) a July 19th PUT with a strike price of 4,580 at a $42 premium.

This transforms my initial hedge to the following (still zero cost) position:

- Long PUT at 5,050

- Short PUT at 4,580

Essentially protecting my downside between 5,050 and 4,580 while keeping all of my upside. The tradeoff is that below 4,580 my downside is not protected, however, given my increased bullishness, I’m more than willing to trade this for unlimited upside.

Note: please be careful when trading options as it can be risky!

Bottom Line

I do think that CPI is headed lower as we work through the lag in shelter and auto insurance inflation. I also think that the market has overreacted and has pushed the probabilities of rate cuts too far into the future. This combination of factors makes me bullish in the short term.

But let’s not forget that historically speaking, the S&P 500 continues to trade at an elevated multiple, with a small margin of safety. For this reason, I want to protect at least some of my downside. In particular, I now hold a zero cost hedge which protects me against the first 9% of downside until 4,580 points.

")

")