")

Harrow, Inc. (NASDAQ:HROW) has built a best-of-breed business in a small niche. Their legacy compounding business, ImprimisRx, has grown rapidly to become the largest ophthalmic compounding pharmacy in the US in only 9 years. Roughly 35% of compounded ophthalmic pharmaceuticals in the US are sold by Imprimis, a market share that dwarfs competitors. Customers are very satisfied, with net promoter scores in the 80s and 90s in recent years.

In a bold move, Harrow pivoted in 2023 into the much larger FDA approved branded pharmaceutical product [BPP] market and is using its impressive distribution and large customer base to sell BPPs to the same customer base it already sells its compounded products to. The shift includes a number of smaller drugs and 4 major drugs. Two of these major BPPs, Iheezo and Vevye, have now been launched, and the results so far are impressive. The long-term future of HROW seems very bright.

However, in February 2024 a cyberattack on Change Healthcare [Change], which operates the largest clearinghouse for medical claims in the U.S., massively disrupted drug reimbursement in the US, affecting many healthcare companies, including Harrow, and caused financial turmoil for physician practices across the country. Although this issue should be sorted out during the second quarter of 2024, HROW’s 1H 2024 will be negatively impacted as a result, which has created the potential for a short-term bear thesis on the stock.

HROW will miss Q1 2024 earnings estimates

I want to be really clear on this point, up front. HROW will definitely miss Q1 2024 sell side earnings estimates. Sell side has not adjusted for Change, and has completely unrealistic numbers out there, $37M in revenue. I will be happy if they beat $27M for Q1 2024!

It’s not clear to me whether sell side understands the issue and simply hasn’t gotten around to updating their models – they are overworked and HROW is not the most important stock they cover – or whether they just don’t know. Either way, everyone familiar with the company knows HROW will miss Q1 earnings estimates. This is not a controversial statement, and for those new to the story, I want to pound the table on this point.

HROW is a growth company

Before I dive in with the bull thesis, it’s worth noting that HROW has grown revenue enormously for many years. All numbers are in $millions, and 2024 is management’s guidance.

| Year | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Revenue | 9.7 | 19.9 | 26.8 | 41.4 | 51.2 | 48.9 | 72.5 | 88.6 | 130 | 180 |

The Bull Thesis

The bull thesis is that HROW will use its dominant position in compounded ophthalmic drugs to expand into the much larger and more lucrative BPP space. Compounded drugs are ubiquitous but low-priced. HROW has guided to $88M of revenue in its compounded segment in 2024 – a pittance by pharma company standards – but has at least some relationship with roughly 50% of ophthalmic prescribers with tens of billions of dollars of buying power. This relationship allows HROW to have considerable insight into their customers’ wants and needs, and new products can be cost efficiently marketed to their existing customer base. The move into BPPs makes a lot of sense, for this reason, and HROW is not reinventing the wheel. Both Allergan and Alcon began as compounding pharmacies, followed the same playbook, and today are 100 times the market cap of tiny HROW.

The company’s first two major drugs are Iheezo, with a total addressable market [TAM] of almost $7B, and Vevye, with a TAM of $20B. Both drugs are off to an excellent early start, implying more than $100M revenue in 2025 each if the early pace is maintained. A third major drug, Triesence, is expected to launch in Q4 of 2024, and will likely contribute $150M in 2025 if the company can execute the launch on this timetable. If we add in contributions from the legacy compounding business and smaller BPP drugs, $500M of revenue in 2025 is within reach, as is the company’s $1B guidance for 2027.

The numbers are impressive, to say the least. The company has guided to more than 80% gross margins and SG&A is unlikely to exceed $200M in 2025 in my view. At $500M revenue, this implies $200M of EBITDA and fully taxed FCF of more than $4 a share in 2025 and more than $10 a share in 2027, and then up from there! A triple digit share price will result, at least $100, but possibly quite a bit more.

And with the business model fully proven with 3 major drugs, more drugs will be added, and HROW will be in a position to replicate the success achieved by pharma giants Alcon and Allergan. That’s the bull thesis.

The Bear Thesis

There is no credible long-term bear thesis on HROW in my view – I will discuss this more later – but there may be a viable short-term thesis. During Q1 2024, the US healthcare reimbursement system suffered a massive cyberattack on its largest clearinghouse for medical claims, Change Healthcare. An American Medical Association survey revealed the huge impact of the attack:

About 1,400 individuals responded to the AMA’s survey, which was conducted between March 26 and April 3… More than three-quarters of respondents reported losing revenue from unpaid claims, and 85 percent of respondents have had to devote additional staff and resources to completing revenue cycle tasks… 55 percent of respondents have had to use personal funds to cover their practice’s expenses, and 31 percent were unable to make payroll.

Emphasis mine. Any high price drug, including HROW’s Iheezo, relies heavily on a functioning reimbursement system to generate sales. Iheezo’s list price is $544 a dose, which is fully reimbursable and therefore ultimately free of charge to end users, but with the reimbursement system offline, many Iheezo users are likely turning to cheaper drugs, at least temporarily. As a result, Iheezo sales are down dramatically. Based on Bloomberg data, I estimate Iheezo sales in Q1 2024 are only half what they were in Q4 2023, or about $4M. What’s more, HROW’s other branded drugs – I estimate these generated $10M of revenue in Q4 2023 – are also likely impacted. If they are as hard hit by Change as Iheezo, this would result in another $5M of lost revenue in Q1 2024.

Revenue in Q4 2023 was $36M, but I estimate only $27M of revenue in Q1 2024 – down 25% – because of the impact of the cyberattack, when the trend would otherwise be up and to the right. The company strongly implied lower Q1 2024 revenue in its Q4 2023 letter to shareholders:

IHEEZO sales in the first quarter of 2024 have been impacted by the Change Healthcare (“Change”) cybersecurity attack… Change has been unable to process medical claims through its primary platforms, and this has had a downstream impact on ASCs and physician offices for some buy-and-bill products, such as IHEEZO. The attack has created a delay in overall cash collection for our customers and is throwing a wrench in their revenue cycle (we’ve heard credible stories of some practices having to take out short-term loans to meet payroll while this is being worked through)… we expect the quarterly revenues to be stronger during the second half of 2024… Given… the temporary disruption resulting from the Change cybersecurity incident, Harrow stockholders should expect quarterly revenue fluctuations…

I think HROW is clearly calling out a downward “fluctuation” in revenue in Q1 2024, and while I can only estimate the size of the impact, it’s my view that it will be substantial.

The cyberattack is well known, and widely reported in the press, and called out by HROW during the latest earnings call. Q1 2024 is almost certainly going to be substantially down from Q4 2023. It’s completely obvious. And yet sell side estimates do not reflect any impact from Change at all, which is the first element of the bear thesis. When HROW reports Q1 2024, it will be reported that they missed sell side revenue estimates. Perhaps sell side analysts don’t know this, and estimates are simply stale, but either way the estimates are there, and they are too high. A miss is never a good look for any stock, and it is certainly plausible that the stock might trade down as a result.

The second leg of the bear thesis is that there is some chance HROW will have to lower guidance for 2024. Guidance is $180M, up 38% from 2023 and more than 100% from 2022. Growth is strong, to say the least! But with at least a $10M hit in Q1, and then more revenue lost in Q2 – Change is still not all the way fixed – and with potential new customers playing defense for at least a while… it’s plausible that change will wind up costing HROW $20M of revenue or more in 2024. Even if the original guidance was somewhat conservative, that might be too much to overcome, and it’s possible that the company will be forced to lower guidance at some point this year. The company acknowledged the challenge but still believes they will meet guidance, saying this in the Q4 2023 letter to shareholders:

Given… the temporary disruption resulting from the Change cybersecurity incident, Harrow stockholders should expect quarterly revenue fluctuations; however, at this time next year, when we look back at the entirety of the calendar year, we believe our guidance will have been met.

And that’s it, the bear thesis in a nutshell. HROW is a mighty growth company, but they will report revenue down perhaps 25% in Q1 2024 compared to Q4 2023. Headlines will read that they missed revenue estimates. And it will be harder for HROW to meet its 2024 guidance than it would have been without the cyberattack.

Over the long term, this is irrelevant. $4 a share of FCF in 2025 and $10 in 2027, and up from there… it will be a blip. Even by Q2 2024, or Q3 at the latest, it will likely be overwhelmed by the huge ramp in sales of Iheezo and Vevye, and hopefully news of the upcoming launch of Triesence. But over the short term, it may be that the market will ignore the future, and focus on what is likely to be a very weak Q1. That’s the bear thesis, as I see it.

Iheezo

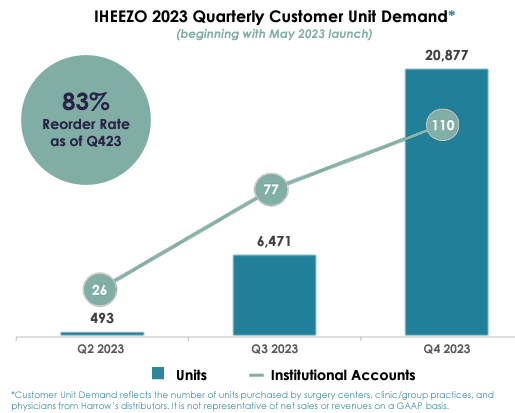

There are 3 major drugs in play in 2024, Iheezo, Vevye, and Triesence. Iheezo is likely a better drug for patients, and it’s good for workflow, but I want to focus on the financial aspect of it. To begin with, Iheezo sales have ramped up nicely in 2023 from the May launch, as the company shows in its Q4 2023 investor presentation:

HROW investor deck

Iheezo net revenue to HROW is about $400 per unit. At $400 per unit, that’s $200k in Q2 2023, $2.6M in Q3, and $8.3M in Q4. At that growth rate, Iheezo would deliver more than $50M of revenue in 2024 and more than $100M in 2025, an excellent start. And yes, it was disrupted by Change, and Q1 2024 will be way down, and Q2 will be impacted as well. But one might reasonably assume $15M or more of Iheezo revenue in Q4 2024, as Change is sorted out and new customers are brought in.

But here’s the thing. All of this progress so far is almost entirely in the cataract market. And on March 19, 2024 the company received game changing good news from CMS:

On the afternoon of March 19, 2024, Harrow, Inc. (the “Company”) received communication from a representative at the Centers for Medicare & Medicaid Services (“CMS”) that the inclusion of J-Code 2403 (IHEEZO’s J-Code) in CMS’s April 2024 quarterly drug pricing file of the average sales prices (ASP) of some Medicare Part B-covered drugs and biologicals confirms that IHEEZO is separately payable in the physician office setting.

This ruling from CMS effectively unlocks the much larger intravitreal injection Retina market for Iheezo use. How important is that? Well, here’s what CEO Mark Baum had to say about it on the Q4 2023 earnings call:

the confirmation from CMS that, in fact, IHEEZO will be paid for separately in the physician’s office setting is, without a question, the most positive consequential event, I think, that has happened to our company since I founded it…

OK, the best thing that’s ever happened to the company. Those are some pretty bold words! Let’s dig into why it’s such a big deal.

To begin with, there are 10.5M intravitreal injections per year in the US, compared to 4.5M cataract surgeries. It’s a larger TAM, but just as important, it’s a much more concentrated market. There are roughly 3k retina specialists in the US, compared to 10k cataract surgeons. This means each retina doctor represents about 7.5x as much potential business as each cataract surgeon. HROW is a tiny company with only 50 Iheezo sales reps, and they can’t possibly reach out to every doctor at their current size. Increasing marketing effectiveness by 7.5x is a big deal. Everything else equal, one might expect Iheezo revenue – once Change is sorted out – to inflect sharply higher, on this basis alone.

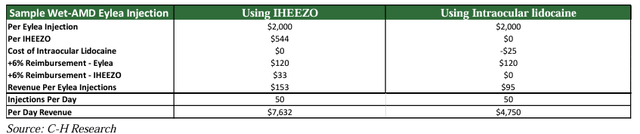

But it gets even better. The financial incentive provided to retina doctors to use Iheezo is, well, epic. Here’s an example put forth by the sell side firm Craig-Hallum on April 11, 2024:

Craig-Hallum

In this example, the economics to the physician for Eylea injections is explored. Eylea injections are used to treat macular degeneration, and people’s sight is at stake. In 2023 there were roughly 3M Eylea injections in the US, corresponding to a $1.2B TAM for Iheezo just by virtue of being paired with Eylea.

Eylea, like Iheezo, is a “buy-and-bill” product. That means the learning curve to adopt Iheezo is minimal. Every Eylea procedure already uses buy-and-bill, so this just adds another drug to a process they already use. Inertia is a big deal in medicine, so anything that makes it easier to adopt a new drug is important.

And then there’s the financial incentive. The way buy-and-bill works is that Eylea is bought by the medical provider for $2,000 a dose and the claim is then billed to CMS for that amount plus 6%. The medical provider is typically offered at least 30 days, same as cash payment terms, so from their POV this is just $120 net coming in the door for each procedure as long as the reimbursement system is functioning normally. However, the provider is responsible for paying out of pocket for anesthesia. In this example, they are using Lidocaine at $25 per unit, and the net revenue to the provider is therefore $95.

But Iheezo is another buy-and-bill product, just like Eylea. And that means, first of all, it’s free. There’s nothing out of pocket, and that saves $25 per procedure. And second, the medical provider is able to bill CMS the extra 6%, just like they do for Eylea, which in the case of Iheezo is another $33. In total, Eylea plus Iheezo works out to $153 per procedure, net to the medical provider, compared to $95 for Eylea plus Lidocaine. That’s a 60% increase!

Does this move the needle? It sure does. The average retina doctor performs 3500 injections per year. At an extra $58 each, that works out to an extra $200k per year, per doctor.

And that’s why Baum said this:

the most positive consequential event… that has happened to our company

The TAM is 2.3x larger, the concentration is 7.5x greater, the customers are all already familiar with buy-and-bill, and the financial incentives to adopt Iheezo are compelling.

How much Iheezo will HROW sell in Q4 2024? Well, maybe $15M in the cataract market is a good guess. And Retina sales are going to be much larger than that. I can’t say with any precision, but I would guess at least $30M, and maybe more like $50M, in Q4 2024. And in 2025 I would be shocked if Iheezo sales did not exceed $200M, and Iheezo as a $1B drug at some point seems highly probable.

Can you think of any reason it isn’t? Please let me know if you can. And none of that “stuff could happen” nonsense. I already know that stuff can happen. I mean, an actual reason why this isn’t the right way to bet. If there’s a reason this is wrong, I would love to hear it?

Triesence

Another major drug in play, potentially as soon as 2H 2024, is Triesence. Triesence is well known among ophthalmologists and is in very high demand. However, despite being in production for nearly 10 years, Triesence production was allowed to lapse by its former owner, Novartis, and it has been unavailable for about 5 years. The reason for the lapse is that Triesence is difficult to manufacture, and it’s too small a drug for a giant company like Novartis to spend much effort sorting it out. Worse, the old price of $175 per unit could not be raised without approval from regulators, and the economics of a hard to manufacture drug at a low price, well, that just wasn’t worth their time.

But HROW bet that they would be able to get approval to raise the price, agreed to acquire Triesence, and then succeeded in pushing a price increase to $944 per unit:

One of our objectives was to complete the transfer of the NDA for TRIESENCE, enabling us to implement a reasonable price adjustment of the product to $944 per unit.

With the economics now in place, HROW can afford to spend what it takes to sort out the tricky manufacturing issues, likely providing incentives to the manufacturer that could not economically be paid at a lower price. And progress is being made, as the following comments on the Q4 2023 earnings call highlight:

because of the progress that we’ve made, there is no one in our organization, whether they’re an employee or a consultant, who does not have a high degree of confidence that we’re going to have Triesence made successfully and very soon.

The company went on to say that there may be as many as 90k units available for sale in 2H 2024 if things go well. This works out to more than $40M of incremental EBITDA this year if they succeed, and more than $50M of incremental revenue. And the numbers go way up from there, with the company saying:

Although about 86,000 TRIESENCE units were sold in 2018, the most recent annual period for which TRIESENCE was intermittently in stock, we estimate the current U.S. total addressable market exceeds 500,000 units annually.

If things go well, Triesence could contribute $200M or more in revenue at some point, perhaps even as soon as 2025.

What are the odds that they will succeed at selling Triesence if they are able to manufacture it? Probably as close to 100% as one ever gets in this sort of thing. Triesence is a well-known drug, and it’s in very high demand. That’s easy to confirm by speaking with ophthalmologists.

Will they succeed in manufacturing it? Well, to me, the obvious bet is that yes, they will. Even if one ignores comments from management about how they are getting close – I don’t ignore those comments! – but even if one did, consider that Triesence was manufactured for more than 10 years. The human race has lost the ability to manufacture it because of… what, exactly? Malicious gremlins? Or, alternatively, the price incentive wasn’t there, and the old owner gave up on it. And now there’s a new owner, with a new price that’s more than 5x the old price. And the human race can, in fact, produce Triesence, but new people are involved, skills need to be mastered, and progress is being made, but that takes time. That makes way more sense to me than the alternative gremlin-based argument.

And so the right way to bet, in my view, is that Triesence will be available at some point. And the only question is when. This is obvious, right?

Vevye

Vevye is one of two new drugs to treat Dry Eye Disease [DED]. There are 16M patients diagnosed with DED in the US, of which 9M have a diagnosis of moderate to severe DED. With a targeted price point of roughly $200 per dose per month, this is an incredible $20B TAM. Previous generations of treatments, such as Restasis, Cequa, and Xiidra, are far from satisfactory, with side effects often outweighing the benefits. As a result, most DED sufferers don’t treat their disease, with less than 10% of them using prescription medication, and roughly an equal number relying only on over the counter medications.

And it’s not as if these patients aren’t willing to give the drugs a try! The first of them, Restasis, peaked at over $1.5B in annual revenue before it went off patent, despite the fact that 90% of patients who tried it decided not to renew their prescriptions after 4 months. It’s not the case that the DED isn’t serious. It is. And it’s not the case that patients don’t seek relief. They do. The old drugs just suck, and for most patients, the benefits don’t outweigh the side effects.

The new drugs, Vevye and Miebo, are vastly better, with minimal side effects and improved effectiveness. Both were developed by Novaliq, with HROW then acquiring Vevye and Bausch + Lomb (BLCO) acquiring Miebo. Miebo was launched first, in September 2023, and Vevye launched in mid-January 2024.

The prediction of the bulls for these drugs – me among them! – is that they will not only split the current DED market between them, but they will also drive many DED patients who have given up on the older drugs to come back and treat their disease. If this prediction is correct, we should be seeing the overall DED prescription drug market increase even as use of the older drugs decreases. And of course, we should see both Vevye and Miebo get off to a great start.

And so far, that is exactly what we see. BLCO just reported Q1 2024, and Xiidra declined from $106M in Q4 2023 to $79M in Q1 2024. One point against the old drugs, and a point in favor of the bull thesis. And yet, the overall prescription DED market has increased by 10%, according to IQVIA data (IQVIA data is unfortunately not public data but was published in a note by Wells Fargo). So, add another point for the bulls. And Miebo – only 28 weeks after launch! – is already more than 10% of the total DED prescriptions. The bulls are ahead three to nothing.

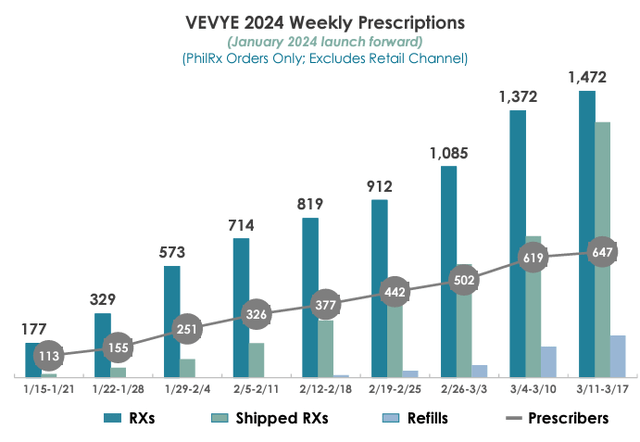

So far, the bull thesis is playing out as expected, at least as far as Miebo is concerned. But what about Vevye? Well, we only have 9 weeks of data since launch. Here it is, from the Q4 2023 investor deck:

HROW investor deck

It’s a pretty picture, but what really matters is that Vevye is tracking at 54% of the launch pace that Miebo is. That’s despite the fact that HROW only has 50 Vevye sales reps and practically no marketing budget, compared to 200 Miebo reps employed by BLCO and correspondingly larger budget.

Drugs tend to have a low rate of adoption in the beginning, which then accelerates, and then levels off. An S-curve, if you will. And in 28 weeks of data with Miebo – again, this is IQVIA data – scripts per week ramped at an average of 266/week in the first 12 weeks and then accelerated to 630 scripts/week in weeks 13 to 28. If Vevye follows a similar pattern, perhaps continuing to hit at 54% of Miebo, the consequences are huge. 54% of 630 is 340 scripts/week per week. So just interpolating the data we have now, Vevye would end 2024 at 15.4k scripts in the final week and would average 42k scripts per week in 2026.

By that time Vevye will presumably be fully insured – at 28 weeks, BLCO estimates Miebo has coverage with 50% of insurers – and net revenue to HROW might be about $200 per script for patients covered by insurance. This works out to $437M of Vevye revenue in 2026. That’s the pace they are on, right now, with only 50 sales reps. And that translates into a ton of FCF. Management has pointed to the eventual sales force size of Restasis – when it was a $1.5B drug – of 400 sales reps. At $250k per sales rep, that would be $100M, if in fact they hire 400 reps. This works out to $5.35/share of full taxed FCF in 2026 just from Vevye alone.

It’s very early days, of course, but so far Vevye is just killing it. It might, of course, accelerate or decelerate from here.

Risks to the thesis

The biggest risk to owners of HROW is the fact that HROW will definitely miss earnings estimates in Q1 2024. Sell side estimates are stale, or the analysts are overworked, or they are missing the impact of Change, or… whatever. But they are wrong. And it’s not HROW’s fault that a third party got hit with a cyberattack, or that sell side numbers have not been adjusted to reflect this. But HROW is going to miss Q1 2024 estimates, and the price action on the stock when that happens might be negative.

Conclusion

The long term bull thesis is more on track now than ever before, and there is no credible long-term bear thesis. Progress on Vevye and Triesence is promising, and recent developments on Iheezo are even more so. A triple digit share price seems all but inevitable.

However, there is a credible short-term bear thesis. The Change cyberattack will have a huge impact on Q1 2024 revenue, and sell side estimates do not reflect this impact. Headlines will likely read that HROW missed earnings estimates, and although everyone already knows – or should know – about the lower revenue in Q1, it might be that the stock will react negatively anyway.