")

")

Introduction

Park Hotels & Resorts (NYSE:PK) is a lodging REIT that has significantly outperformed the sector Vanguard Real Estate Index Fund ETF (VNQ) year-to-date:

PK vs VNQ in 2024 (Seeking Alpha)

This should come as no surprise since Hotel REITs have been one of the top performers recently, delivering robust revenue per available room, or RevPAR, growth.

Going forward, I see Park Hotels & Resorts tracking the REIT sector’s performance, with the market cap rate of about 4.4% below peers despite similar growth prospects. Even if the REIT returns adjusted EBITDA to 2019 levels, its market cap rate would only be in line with peers. As such, I rate the shares a hold.

Company Overview

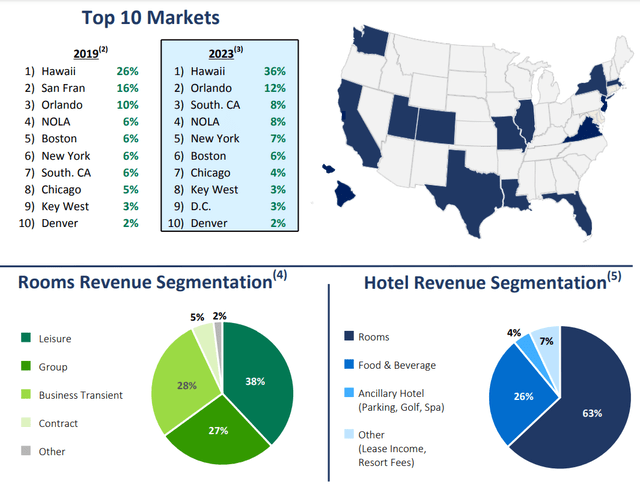

You can access all Park Hotels & Resorts results here. The REIT operates 43 hotels offering some 26,000 rooms, focusing on the luxury and upper-scale segment (86% of all rooms). The largest markets for the company are Hawaii and Florida, accounting for about 51% of 2023 hotel adjusted EBITDA:

Top markets & revenue drivers (Park Hotels & Resorts March 2024 investor presentation)

Operational Overview

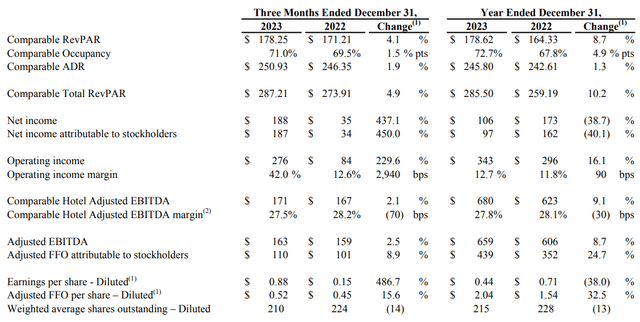

Comparable occupancy increased 1.5% Y/Y to 71% in Q4 2023 (2023: +4.9% to 72.7%), while the average daily rate grew 1.9% in Q4 (2023: +1.3%). The combined effect on RevPAR was a 4.1% Y/Y increase in Q4 (2023: + 8.7%).

Adjusted EBITDA grew 2.5% Y/Y in Q4 and 8.7% for the full year, while adjusted FFO per share was $0.52/share in Q4 2023, up 15.6% (2023: $2.04/share, +32.5%):

Q4 and 2023 Results Overview (Park Hotels & Resorts Q4 2023 Results Press Release)

2024 Outlook

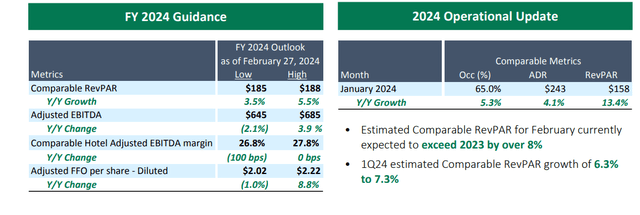

As you can tell from the data in the operational summary, the REIT largely experienced a slowdown in growth in the final quarter of 2023. Looking ahead, the trend is set to continue, with RevPAR and adjusted EBITDA growing 4.5% and 0.9% respectively in 2024, while adjusted FFO is set to increase by about 3.9% to $2.11/share:

2024 Outlook (Park Hotels & Resorts March 2024 investor presentation)

That said, Q1 2024 guidance is for RevPAR growth of 6.8% Y/Y, implying a slowdown in growth for the remainder of 2024.

Debt and Capital Structure

Park Hotels & Resorts ended 2023 with a net debt of about $3.4 billion, excluding $0.7 billion associated with two hotels in receivership (the REIT decided in June 2023 to stop making interest payments on a non-recourse mortgage loan secured by two San Francisco hotels). With a market cap of circa $3.6 billion, debt accounts for 49% of the REIT’s enterprise value.

All of the debt is fixed rate, carrying an average interest rate of 5.24%, while interest on the unutilized floating rate revolver is 7.44%. With no significant maturities in 2024 and just 17% of the debt maturing in 2025, the company is well-positioned to ride out the current elevated interest rate environment.

Market-implied cap rate

The exact cash flow figure used to calculate the market-implied cap rate will greatly influence the result. For 2024, the REIT forecasts an adjusted FFO of about $446 million, which I will reduce downward by $17 million in share-based compensation and $300 million in capex spending (in line with 2023 and slightly ahead of deprecation). Furthermore, Park Hotels & Resorts is set to pay about $180 million in interest in 2024.

Combining all the aforementioned moving parts (446 – 17 – 300 + 180), we arrive at a post-capex cash flow to enterprise value of about $309 million. With a current enterprise value of $7 billion, the market-implied cap rate is roughly 4.4%. On the one hand, it already incorporates significant capital expenditures which will boost RevPAR in the future. On the other hand, the 4.4% market cap rate is quite low on an absolute basis.

For comparison, RLJ Lodging (RLJ), which I covered here, offers a higher 5.6% market cap rate with similar RevPAR growth in 2024.

Recovery to 2019 levels

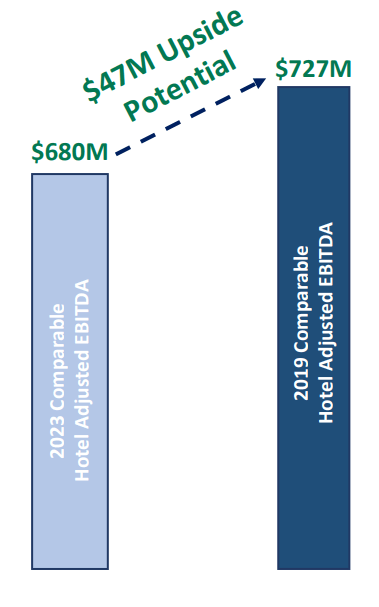

Across the hotel submarkets the company operates in, only Resort 2023 adjusted EBITDA is above 2019 levels ($52 million higher), with Urban, Airport, and Suburban submarkets still delivering lower results in 2023 relative to 2019 ($99 million lower). As a result, a potential catchup in these submarkets could boost adjusted EBITDA by circa $47 million, or even $99 million if the recovery is 100% and the Resort subsegment keeps delivering higher results:

EBITDA catchup potential (Park Hotels & Resorts March 2024 investor presentation)

Using my $309 million enterprise-level cash flow and 4.4% market cap rate assumption, we see that an incremental $47 million cashflow would boost the market cap rate to 5.1%, while a full recovery with $99 million higher cash flows would result in a 5.8% market cap rate.

Conclusion

After delivering a RevPAR increase of 4.1% in Q4 2023 and 8.7% for the full year, RevPAR growth is set to continue at about 4.5% in 2024. The company’s debt is entirely fixed rate, insulating it from the current elevated rate environment. Indeed, by the time it has to refinance its loans, odds are interest rates will be lower than today, and as a result, Park Hotels & Resorts will likely see no significant interest rate expense increases in the coming decade.

The valuation of the company from an enterprise level appears elevated to peers, and a recovery to 2019 levels in the company’s lagging hotel submarkets would be necessary to bridge the valuation gap. As such, despite the strong growth prospects, I rate the shares a hold.

Thank you for reading.

")

Q4 2023 Earnings Call Transcript")

")