")

")

All financial numbers in this article are in Canadian dollars unless noted otherwise.

Introduction

It’s time to talk about a more than 100-year-old company that is still a dividend growth stock.

That company is the Canadian National Railway Company (NYSE:CNI).

Founded in 1919, the company is the result of the combination of several railroads that had gone bankrupt and become part of the Canadian government.

On November 17, 1995, the company was privatized, turning into one of the most diversified Class I railroads in North America. This included major M&A projects, like the Illinois Central Railroad and the Wisconsin Central.

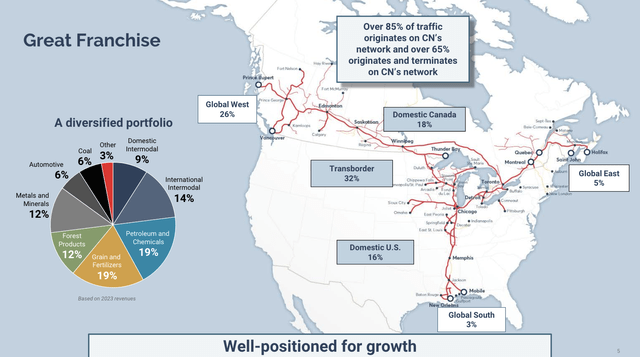

Excluding partnerships to gain access to the Mexican market, the company’s own railway operations span both Canada and the United States, with most of its revenue coming from high-margin goods like forest products, agriculture goods, and chemicals. Slightly less than a quarter of its revenues come from consumer-focused intermodal goods.

Canadian National Railway

The company, which generated close to $17 billion in revenue last year, has access to seven major ports and the benefit of long hauls, as the average length of its trips is north of 700 miles.

It’s also one of the few companies that I have been bullish on for many years without buying it. That is based on my investments in three other railroads, including its Canadian peer, Canadian Pacific Kansas City (CP), which serves all three North American nations through its own network after acquiring the Kansas City Southern Railroad, which Canadian National tried to buy as well.

My most recent article on the stock was written on January 26, when I went with the title “Canadian National Railway: A Great Buy On Weakness.”

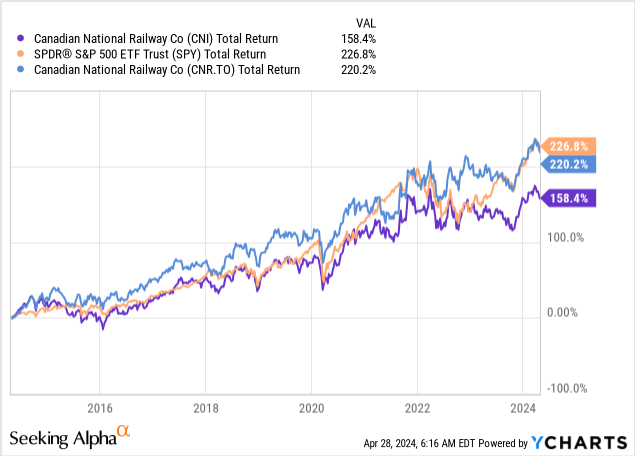

Back then, I went from a Bullish rating to a Neutral rating due to its stock price surge and clouding economic indicators. Since then, shares have risen 1%, lagging the S&P 500 by roughly 330 basis points.

Over the past ten years, New York-listed CNI shares have returned 158%, lagging the S&P 500 by more than 60 points. However, Toronto-listed CNR shares have beaten the S&P 500 by slightly more than six points.

In this article, I’ll update my thesis, using its latest quarterly earnings and my long-term view on the company’s ability to provide both consistent capital gains and steadily rising income.

So, let’s get to it!

Strength In Challenging Times

Current times are not easy for railroads. Demand is weak in certain areas, pricing has become an issue, including an unfavorable lag in fuel surcharges, and persistently sticky inflation is pressuring margins even further.

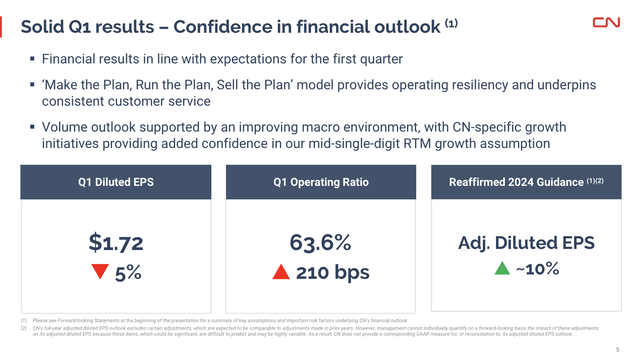

Based on that context, despite seeing flat year-over-year volumes in the first quarter, there was a marginal decrease of roughly 1% in revenues.

Operating income totaled around $1.5 billion, which marks a 7% decrease.

As a result, the operating ratio increased to 63.6%, up from 61.5%, which is an increase of 210 basis points and one of the reasons why diluted EPS dropped by 5% to $1.72.

Canadian National Railway

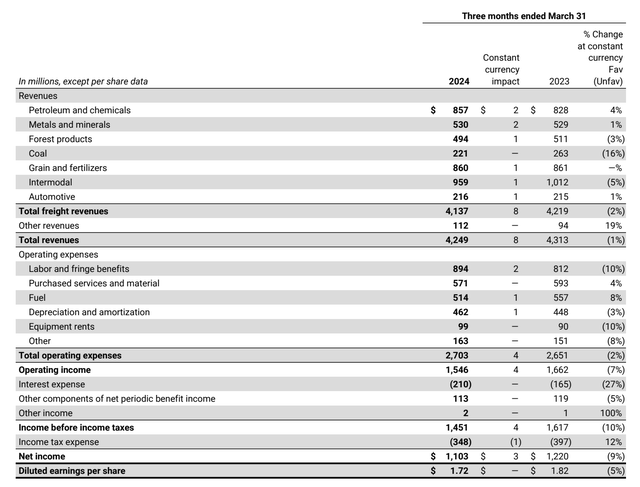

Generally speaking, underlying factors were the aforementioned unfavorable fuel surcharges and higher operating expenses, which were attributed to factors like 10% higher labor costs due to a higher headcount and higher wages.

Canadian National Railway

Diving a bit deeper into the company’s operating segments, the petroleum and chemicals sector saw a 6% increase in RTMs (revenue-ton miles), driven by record volumes in refined products and natural gas liquids.

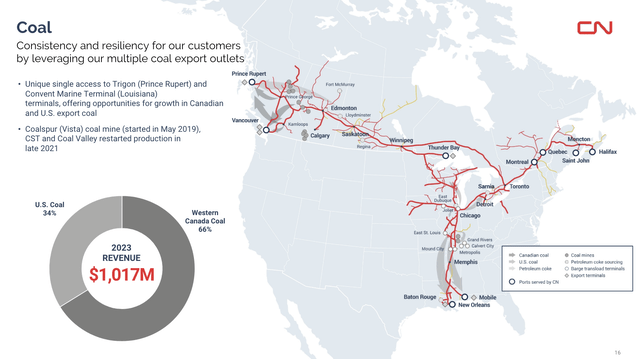

Meanwhile, challenges persisted in the bulk sector, particularly with coal transportation. Canadian coal volumes dropped by 20% due to production issues, while U.S. coal volumes fell by 23% due to weak export demand for thermal coal.

This is very common in this environment, as very low natural gas prices pressure both coal demand and pricing.

Canadian National Railway

Grain and fertilizer volumes remained steady overall, with strong potash growth compensating for softer grain volumes.

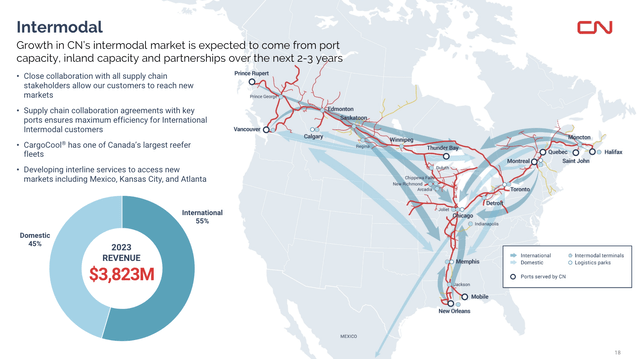

International intermodal volumes increased by 5%, driven by consistent growth since the previous quarter.

Domestic intermodal volume declined by 3% due to ample trucking capacity. This, too, is common, as lower economic growth has made it tougher to compete with lower truck rates.

Canadian National Railway

The good news is that the company expects continued support from the North American economy and a gradual recovery in domestic intermodal markets, with tailwinds in grain, potash, and intermodal transportation.

However, challenges persist in sectors like coal due to low global demand.

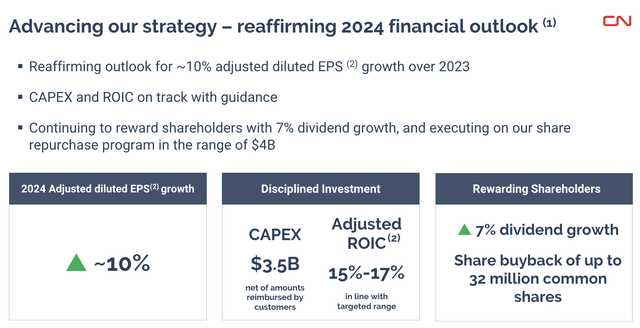

As such, it reaffirmed its 2024 financial outlook, which aims for 10% adjusted diluted EPS growth.

Canadian National Railway

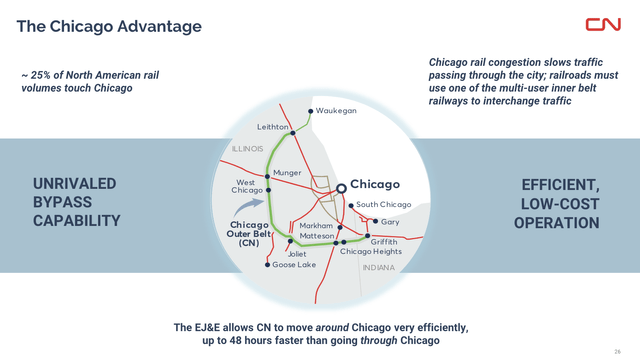

On top of this, the company is consistently investing in its network, including investments in key corridors through “no regret capital” projects. These initiatives include completing additional double track along the Vancouver to Chicago corridor and extending sidings in British Columbia.

Essentially, by expanding capacity in critical corridors, CN aims to support growing demand and reduce congestion, providing efficient and reliable transportation services for customers.

After all, 25% of North American rail volumes move through Chicago, which puts an emphasis on operating efficiencies.

Canadian National Railway

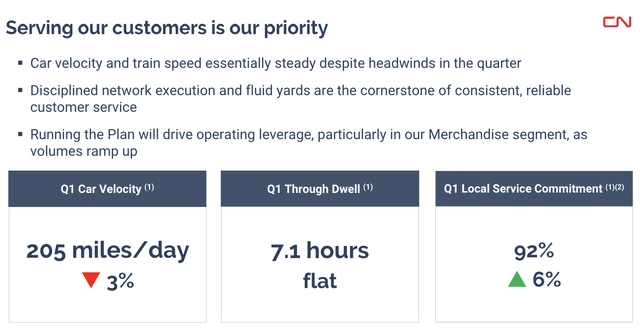

Speaking of service levels, in 1Q24, the company improved its local service commitment while its dwell time was kept flat.

Canadian National Railway

The mix of a good outlook, network investments, and better service levels bodes well for investors.

There’s So Much Value In CNI

In the first quarter, the company generated roughly $530 million of free cash flow, which is a slight decrease compared to the previous year.

This decline was mainly attributed to higher capital expenditures during the period, although it was partially offset by higher net cash from operating activities.

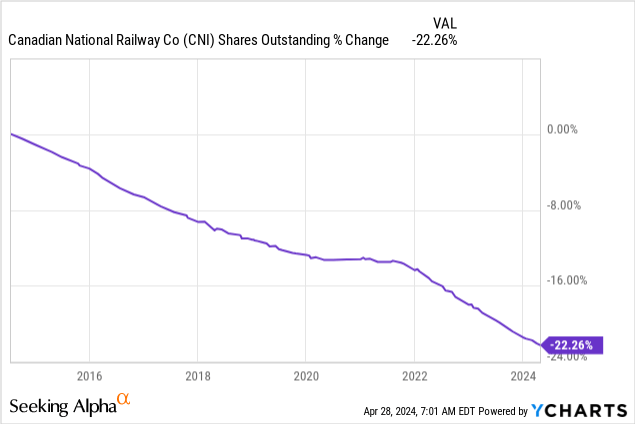

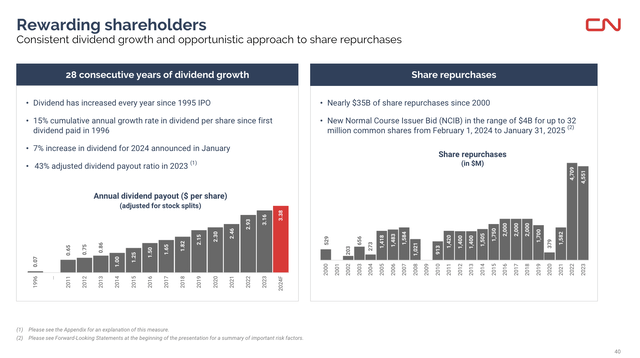

Additionally, the company repurchased close to 3.5 million shares for nearly $600 million under its current share repurchase program.

Over the past ten years, the company has bought back more than a fifth of its shares, which positively contributed to the per-share value of its business and its total return profile.

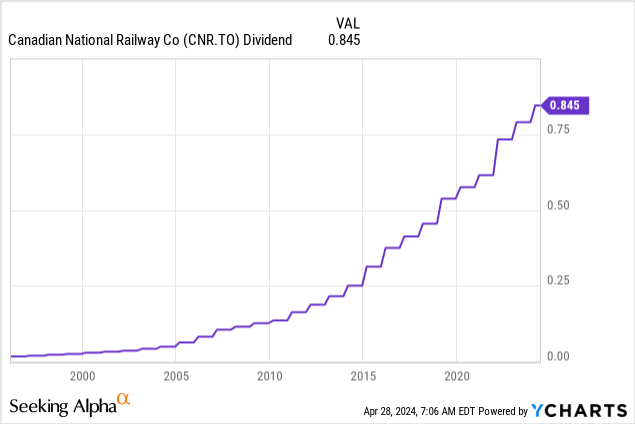

The company also hiked its dividend in the first quarter. On January 24, the Board approved a 7% hike to $0.845 per quarter per share. This implies a 2.0% dividend yield.

This dividend is protected by a sub-50% payout ratio and comes with a five-year CAGR of 10.6%.

CNI has hiked its dividend every single year since becoming an independent company, which obviously includes the Great Financial Crisis and the pandemic.

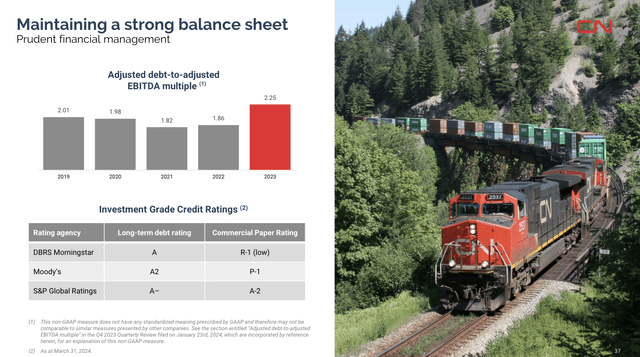

In this case, it also helps that CNI is a very conservatively run railroad that highly values a healthy balance sheet.

In its first quarter, the company ended with a 2.4x net leverage ratio. It has A-range ratings from all major rating agencies.

Even during the pandemic, the company maintained a 2x leverage ratio.

Canadian National Railway

Because of its extremely healthy balance sheet, the company decided to accelerate share repurchases in 2022.

Canadian National Railway

Now, let’s take a look at its valuation.

Valuation

I am bullish on the future of the Canadian National Railway. I believe it has everything it needs to deliver both elevated capital gains and steadily rising income on a prolonged basis.

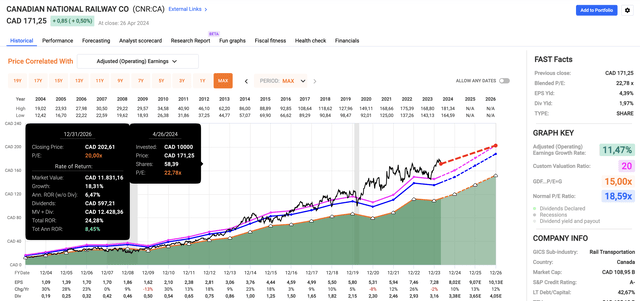

On a shorter-term basis, we see that CNI/CNR is trading at a blended P/E ratio of 22.8x, which is above its long-term normalized multiple of 18.6x.

However, analyst expectations are upbeat. This year, analysts are looking for 10% EPS growth, which is in line with company guidance. In 2025 and 2026, growth is expected to be 13% and 12%, respectively.

FAST Graphs

In other words, they expect an uptrend that usually warrants a 20x EPS multiple.

Using that multiple (as displayed by the pink line in the chart above), we get a fair stock price of $202 in Toronto, which is 18% above the current price. The same applies to New York-listed shares, with the exception that CAD/USD fluctuations have an impact.

These numbers imply an 8% annual return through 2026. Hence, if I were looking for even more railroad exposure, I would try to buy CNI for close to US$160. That number implies a 10% annual return, which makes the risk/reward a bit juicier.

Takeaway

Investing in Canadian National offers a unique mix of stability and growth potential.

Despite facing challenges such as weak demand in certain sectors and margin pressures from inflation, the company maintains resilience through its diversified revenue streams and strategic investments in network expansion.

With a track record of consistent dividend hikes and a commitment to shareholder value through share buybacks, CNI stands out as a solid long-term investment.

Meanwhile, analysts’ optimistic projections suggest the potential for significant upside, making CNI an attractive addition to any portfolio seeking both capital appreciation and income growth.

Pros & Cons

Pros:

- Stability & Growth Potential: CNI offers a mix of stability and growth opportunities, backed by diversified revenue streams and strategic investments.

- Consistent Dividend Growth: With a track record of consistent annual dividend hikes, CNI provides steady income growth for investors.

- Strategic Investments: The company’s focus on network expansion and efficiency improvements positions it well for future growth and market leadership.

Cons:

- Market Challenges: CNI faces challenges such as weak demand in certain sectors and margin pressures from inflation, which may impact its short-term performance.

- Operating Environment Risks: Factors like fluctuating fuel costs and labor expenses pose risks to the company’s operating margins and profitability.

- Valuation Concerns: While analysts are optimistic about future growth, CNI’s current valuation may be perceived as relatively high, which means there’s little room for error.

- Currency Changes: Because Canadian National is a Canadian company, foreign investors need to be aware of the impact of currency fluctuations on the value of their investments and dividends.