")

Successful investing is about managing risk, not avoiding it.

Benjamin Graham

Let’s talk about the elephant in the room. While many income investors seek a relatively safe source of income and wish to preserve capital in doing so, there are many assumed risks associated with CEFs that offer a high yield distribution. For example, several SA analysts who have reviewed Oxford Lane Capital (NASDAQ:OXLC) in recent months have concluded that the current distribution yield of 19% represents extreme risk, and they suggest staying far away or selling. My analysis suggests a different recommendation, and that is to buy shares of OXLC now for the income while the premium remains low and the distribution yield, which is well covered by core net investment income, remains high.

Seeking Alpha

As a now retired income investor who seeks passive income from my investments “while I sleep”, I look for opportunities to purchase shares of high yield dividend paying stocks and funds. Many of my portfolio holdings in my Income Compounder portfolio include CEFs that offer a monthly distribution. By reinvesting all or a portion of those monthly distributions, I continue to grow my future income stream, and if I can take advantage of low pricing by buying those CEFs at a discount, or at least a lower-than-average premium, then I can increase my future income stream even further. That is the basic concept behind my IC strategy, which has worked very well for me in the past couple of years since I began to shift from accumulation mode to the “decumulation” phase of my investing experience.

What is the NAV of OXLC?

While OXLC now trades at a slight premium to NAV of about 1.6%, that premium is based on an estimated NAV that is reported quarterly (with monthly estimated ranges). Furthermore, the NAV of a fund that holds CLOs as OXLC does, is challenging to estimate because of the difficulty in quantifying variables that affect CLO pricing. This Primer on the Valuation of CLO Equity for Financial Reporting gets into the details if you would like to learn more.

The standard application of the Income Approach for structured products is to forecast the cash flows on the underlying collateral pool and then allocate those collateral cash flows to the respective CLO securities using the transaction waterfall provided in the transaction’s governing documents. In the case of a CLO transaction, key assumptions include the expected credit performance of the collateral pool, loan voluntary-prepayment rates, and expectations for the deal call option, as well as assumptions regarding the anticipated behavior of the collateral manager during the reinvestment period. A robust valuation often involves using multiple cash flow scenarios to assess the sensitivity of the subject bond’s cash flows to changes in the collateral-performance assumptions. Finally, the tranche cash flows are discounted to a present value using discount rates (spreads, discount margins, yields) that are observed from new-issuance pricing and secondary-market transactions.

While I am certainly no expert on CLOs, I do feel that OXLC has the expertise and proven ability to effectively manage a CLO fund and I trust their judgment in determining the NAV of the fund. The OXLC fund website posts the monthly estimated NAV and for the February estimate published on March 7, 2024, the NAV was estimated to be in a range of $4.90 to $5.00.

Management’s unaudited estimate of the range of the NAV per share of our common stock as of February 29, 2024 is between $4.90 and $5.00. This estimate is not a comprehensive statement of our financial condition or results for the month ended February 29, 2024. This estimate did not undergo the Company’s typical quarter-end financial closing procedures and was not approved by the Company’s board of directors. We advise you that our NAV per share for the quarter ending March 31, 2024 may differ materially from this estimate, which is given only as of February 29, 2024.

But because CEFs tend to trade at a discount or premium to NAV and those price variations can swing quite wildly at times, it is important to know what level of premium or discount is ideal when purchasing shares, and whether that NAV is rising or falling. The monthly estimated NAV for March was provided in a OXLC Q4 2024 preliminary estimate and update (for the quarter ending March 31, 2024) on April 17. In that press release, the estimated NAV for March was reported as between $4.85 to $4.95. That would indicate a decline of $.05 in the NAV between February and March going by the midpoint of each range, which included a dividend of $.08 paid (which would have reduced the NAV by that amount), which effectively indicates a slight increase in NAV of about $.03.

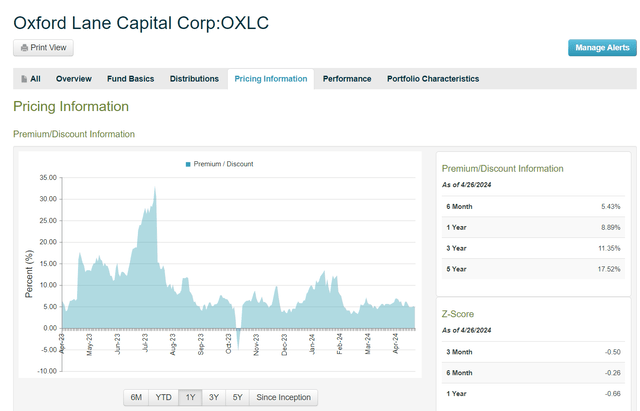

Meanwhile, the market price of the fund has remained just below $5, closing at a price of $4.98 as of the market close on 4/26/24. That represents a premium of only about 1.6% above NAV if we use the midpoint of the March estimate, which would be $4.90. That is well below the 1-year average premium of about 9% and even significantly lower than the 3-year or 5-year average premium. The only time the premium was lower in the past year was back in October when OXLC briefly traded at a discount.

The chart below from CEFconnect shows the 1-year pricing range and as you can see, the premium has been steadily dropping even though the NAV has remained steady to even a slightly increasing NAV. This mispricing represents the ongoing fear that investors have about the high-yield distribution that OXLC pays out.

CEFconnect

How Safe is the OXLC 19% Yield?

Let’s review the high yield distribution from OXLC, which is the primary reason for investors to own the stock. As a RIC (regulated investment company) the company is required to distribute at least 90% of its taxable income annually. However, the way that taxable income is determined for a fund that holds CLOs is different from other CEFs that rely on NII and/or capital gains to cover the distribution. In the case of OXLC, what they refer to as “core NII” is a more useful metric for determining distribution coverage.

While OXLC currently pays a monthly distribution of $.08 per share (which was raised from $0.075 in July 2023), the core NII was estimated at between $0.32 and $0.38 per share as of March 31 according to the press release. That means that at least 8 cents of quarterly undistributed core NII is available for future distribution, perhaps in the form of another raise in the monthly distribution or paid out at the end of the fiscal year as a supplemental distribution. In the press release, further details of what is included in the determination of core NII is provided:

Supplemental Information Regarding Core Net Investment Income Estimates

We provide information relating to core net investment income (a non-U.S. generally accepted accounting principles (“GAAP”) measure) on a supplemental basis. This measure is not provided as a substitute for GAAP NII, but in addition to it. Our non-GAAP measures may differ from similar measures by other companies, even in the event of similar terms being utilized to identify such measures. Core NII represents GAAP NII adjusted for additional applicable cash distributions received, or entitled to be received (if any, in either case), on our CLO equity investments. The Company’s management uses this information in its internal analysis of results and believes that this information may be informative in assessing the quality of the Company’s financial performance, identifying trends in its results and providing meaningful period-to-period comparisons.

Income from investments in the “equity” class securities of CLO vehicles, for GAAP purposes, is recorded using the effective interest method; this is based on an effective yield to the expected redemption utilizing estimated cash flows, at current cost, including those CLO equity investments that have not made their inaugural distribution for the relevant period end. The result is an effective yield for the investment in which the respective investment’s cost basis is adjusted quarterly based on the difference between the actual cash received, or distributions entitled to be received, and the effective yield calculation.

While Core NII may provide a better indication of our estimated taxable income than GAAP NII during certain periods, we can offer no assurance that will be the case, however, as the ultimate tax character of our earnings cannot be determined until after tax returns are prepared at the close of a fiscal year. We note that this non-GAAP measure may not serve as a useful indicator of taxable earnings, particularly during periods of market disruption and volatility, and, as such, our taxable income may differ materially from our Core NII.

Excess Core NII Reported in Previous Quarters

In terms of how the estimated core NII for the fiscal Q4 period (calendar year first quarter) compares to the previous quarter reported in January, the earnings call sheds some light on what transpired at the end of 2023. The fiscal Q3 results were summarized by CEO Jonathan Cohen on the Q3 earnings call:

Our core net investment income was approximately $82.7 million or $0.39 per share for the quarter ended December compared with approximately $79.7 million or $0.41 per share for the quarter ended September. For the quarter ended December, we recorded net unrealized appreciation on investments of approximately $6.7 million and net realized losses of approximately $3.1 million or $0.02 net per share. We had a net increase in net assets resulting from operations of approximately $52.4 million or $0.25 per share for the third fiscal quarter.

Therefore, it appears that core NII has exceeded the distributions paid in each of the past 3 quarters by a considerable amount, although declining slightly from quarter to quarter. With the pending fiscal Q4 report coming up in May, I would expect that OXLC will be required to pay a special or supplemental dividend to meet their requirement to distribute at least 90% of taxable income, assuming that the estimates of core NII closely approximate taxable income.

Additional comments from CEO Cohen in the Q3 transcript are worth including here and may help to explain how OXLC can continue to sustain such high yield distributions.

The weighted average yield of our CLO debt investments at current cost was 16.6%, down from 18.5% as of September 30th. The weighted average effective yield of our CLO equity investments at current cost was 16.5%, up from 16.3% as of September 30th. The weighted average cash distribution yield of our CLO equity investments at current cost was 24%, down from 25% as of September 30th. We note that the cash distribution yields calculated on our CLO equity investments are based on the cash distributions we received or which we were entitled to receive at each respective period end.

These levels of returns from CLO equity tranches are not unusual and help to explain why so many CLO CEFs are starting up, including EARN, which I recently wrote about that is converting from an REIT to a CEF that holds CLOs.

OXLC DRIP Policy Further Enhances Returns

As I discussed in my recent article about Closed End Funds That Offer A Discount To Reinvest, the Board of Directors at OXLC approved a DRIP (distribution reinvestment plan) policy that supports additional gains from reinvesting the monthly distribution into new shares of the fund. As described in the fund’s Annual Report (page 60), reinvesting offers a discount whether the shares trade at a premium or discount to NAV:

We have adopted a distribution reinvestment plan that provides for reinvestment of our distributions on behalf of our stockholders, unless a stockholder elects to receive cash as provided below. As a result, if our Board of Directors authorizes, and we declare, a cash distribution, our stockholders who have not opted out of our distribution reinvestment plan will have their cash distributions automatically reinvested in additional shares of our common stock, rather than receiving the cash distributions.

We expect to use primarily newly-issued shares to implement the plan, whether our shares are trading at a premium or at a discount to net asset value. Under such circumstances, the number of shares to be issued to a stockholder is determined by dividing the total dollar amount of the distribution payable to such stockholder by an amount equal to ninety-five (95%) percent of the market price per share of our common stock at the close of regular trading on the Nasdaq Global Select Market on the valuation date fixed by our Board of Directors for such distribution.

What this means is that for investors who elect to reinvest in more shares of OXLC using their monthly distribution, those shares may be reinvested at a price that is up to 5% below the market price. That effectively lowers the cost basis of newly issued shares, thereby increasing the yield on cost. For those investors who rely on the monthly income for living expenses, an equivalent number of shares could be sold at market price, capturing an immediate gain of up to 5%. However, for those investors like me who wish to increase their future income and reduce the cost basis of their existing holdings, reinvesting at discounted prices makes a lot of sense and provides yet another reason to buy shares of OXLC even when it is trading at a slight premium.

Summary: Buy OXLC for the High Yield Income While the Price is Low

There are now many choices of funds that hold CLOs and offer a high yield income to investors who are somewhat risk tolerant. Other CLO funds include ECC, EIC, CCIF (which I last covered in December), OCCI, JBBB, CLOZ, and more. Some of those funds, including EIC and JBBB, hold mostly CLO debt, while others hold a mix of equity and debt tranches.

While OXLC currently offers the highest yield of the CLO funds available to retail investors, it may also hold the highest risk due to its concentration in the equity tranches of CLOs, although that risk is less than what many might imagine based on my review of the core NII being reported.

Also, default rates for CLOs are historically low and as explained by this treatise from Guggenheim on Understanding CLOs, the recovery rate is typically higher compared to high yield bonds.

Most CLO collateral consists of senior secured loans, or first-lien loans, which have a priority claim on all of the related company’s assets in the event of bankruptcy and are intended to be a less risky investment in these companies. CLOs historically have further mitigated default and recovery risk of individual company credits by holding diverse portfolios of leveraged loans – typically more than 200 borrowers – that are actively managed.

The future returns of CLO funds like OXLC may be affected by any potential reductions in interest rates should the Fed decide to take that action later this year, however, the impact on CLO returns based on lower interest rates is negligible, at least according to some sources. This February 2024 discussion from Pinebridge explains why this is a good time for CLO equity returns and how changing interest rates could impact CLOs.

Moreover, although many are betting that the economy is headed for a slowdown, the long-wished-for “soft landing” is now a distinct possibility. That could be the best scenario of all for CLO equity, as it would mean the Fed is cutting rates, but not by much. With rates stabilizing at a low enough level to provide loan issuers more breathing room but still high enough to support healthy CLO yields, more loan issuers and debt investors could be drawn back into the market, providing managers with a better selection of loans to choose from and potentially compressing liability spreads.

In the case of OXLC, the NAV remains steady to improving over the past few months, the price is currently trading at a lower-than-average premium, and core NII more than covers the current high yield distribution. I rate OXLC a Buy for income investors who are willing to accept the risk associated with a fund that holds CLO equity in return for a steady high yield income stream.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.