")

Analyzing Meta’s Long-Term Future

Meta (NASDAQ:META) has become very active in artificial intelligence as of late. The firm is arguably morphing into not only a social media conglomerate focused on AI but a technology infrastructure hub that, over the long term, I believe, could have its social media operations significantly morph into the foundation of more AI-based websites and apps. It is my opinion that to remain competitive over the long term, the company is going to have to compete with the likes of X and super apps in China in offering a full suite of not only social media but AI-ecosystem tools, which I believe will also include a higher focus of financial assets within the platforms. Thankfully, Meta is very well aware of the evolving competition, and Mark Zuckerberg seems tuned in to the financials of his firm as well as the technology that is his initial skill set. Zuckerberg’s understanding of finance is something he has seemingly had to learn over time from watching his interview with Dwarkesh Patel. I believe that after Zuckerberg’s ‘Year of Efficiency’, Meta and Zuckerberg have come out a lot stronger, and in the future, Musk and X will compete with Zuckerberg and Meta in multiple domains, not just in social media but in AI and internet ecosystems.

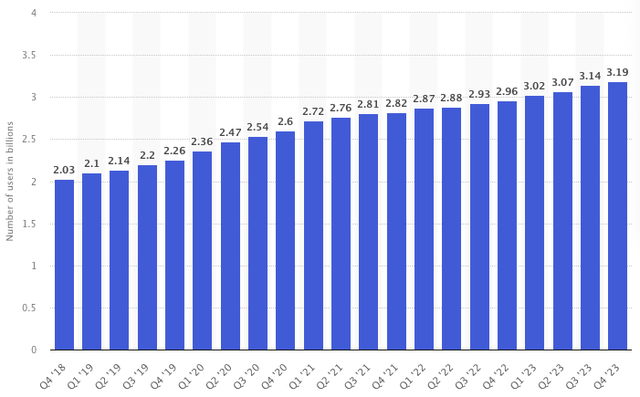

The advantage that Meta has at this time is that it reported 3.19 billion monthly active users across its family of apps in Q4 2023:

Meta daily active users in billions (Stacy Jo Dixon on Statista)

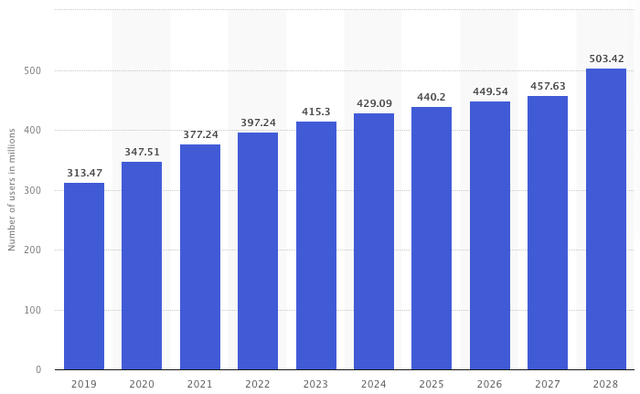

Its large user base has no shortage of competitive advantage and moat. X.com, as of 2024, is estimated to have around 429 million daily active users, although it is difficult to get an accurate exact figure due to the company being private.

Number of X (Twitter) users worldwide, including estimates (J. Degenhard on Statista)

In addition, it is well established that some Chinese super apps, like WeChat, have a billion or more daily active users, and hence, this is arguably the more severe and pressing competitor to Meta at the time of this writing. I believe that this concern is even more real considering the heightened geopolitical tensions at this time and arguments that China may become the dominant world power. In many respects, some people believe this is unavoidable, and it may become the case that China’s social media platforms come to dominate the internet climate over the long term.

However, in the immediate future, I think Meta will retain its top spot in the social media hierarchy. The threat of China remains real, but I believe it is also assailable because Meta is supported by a very complex system of federated power in economics that, I believe, is stronger than China’s socialist style of governance. I think that the interplay between native Western economics and its social media infrastructure is integral to why Meta will continue to be a company worth holding a stake in over the long term.

Value Analysis

At the time of this writing, Meta stock doesn’t offer investors very good value for money. Instead, it is the WeChat operator, Tencent Holdings (OTCPK:TCEHY), which offers a much better valuation. This begs the question again: how likely is it that the United States will continue to be the dominant world power over the next 50-100 years? If China does outcompete it reliably, I think investors in Tencent are in for a large long-term win. Meta, at the present valuation, likely would not be deemed a good long-term investment, even if it continues to grow well. The valuation is arguably not appealing enough.

I wouldn’t have said this in late 2022 when Meta stock was at the bottom of its colossal sell-off. Since then, the stock has had a monumental turnaround in price, and intelligent investors who bought during that time are undoubtedly nothing short of great value investors. Now, the stock is trading at all-time highs, which presents a lot less of an opportunity unless investors are decidedly only focused on Meta’s long-term growth, which I think, due to the company’s massive saturation this late in the game, will be highly dependent on new areas of operation, like artificial intelligence.

Meta is doing an exceptional job of developing its own AI, most notably its Llama models, but it is also continuing to develop a portfolio of AIs that I believe are going to position it as one of the leaders in AI over the long term. This is an incredible competitive advantage for Meta to have. Zuckerberg and his team have done well to pivot and iterate in this regard as soon as they noticed that AI was taking full flight. But Tencent Holdings is also developing AI, so one has to argue: is better value and perhaps less prestigious AI better than high growth at a premium valuation with arguably some of the best AI in development? Investors also have to consider that Tencent Holdings is not only a technology company, with massive investments overseas, acting like a conglomerate holding company rather than a pure social media firm. In addition, I believe that in time Tencent’s AI developments will catch up to the Western leaders, perhaps even innovating on it more rapidly. This opens up considerable further added value for investors in the Chinese technology conglomerate at this time. To compare each company on TTM P/E GAAP, Tencent has a ratio of around 19 at the time of this writing, which doesn’t account for the investment holdings it has; Meta has a ratio of around 33.

Risk-Reward Analysis

My opinion of Meta, in general, is that it is an exceptional company with a very large moat in social media user saturation and technological advancement. I believe the company has proven over many decades the executive team’s strengths in allocating capital effectively to not only iterations within Facebook but also to its multiple powerful acquisitions, which have positioned the firm as a leading technology conglomerate today. Meta’s long-term goal is to create artificial general intelligence and an ambitious plan to use around 600,000 AI GPUs to train its next-generation AI models. This, I believe, is a very strong move and bodes well in a lower-risk, high-reward segment of high-capex technology development with a strong moat in operations.

However, Mr. Zuckerberg’s Realty Labs projects, including the Metaverse, are somewhat less of a return on investment at this time. Yet, this seems like a long-term bet that could be undervalued today but highly sought after in the future. Then again, I do see some risk here that the Metaverse becomes one of Meta’s notable big mistakes, which could detract somewhat from my overall Buy investment thesis. But if Meta has proven anything over the long term, it is that the firm is highly adaptable and willing to iterate and pivot based on the reaction of the market to its offerings over sustained periods. If the Metaverse has a poor return on investment over the long term, I believe it will change dramatically to fit what consumers want.

Key Takeaway

Meta is going to be one of the major firms with some of the strongest AI in the world. At this time, the stock is not a value investment, and I assess that it is moderately overvalued. Tencent Holdings offers much better value and significant exposure to Chinese social media and AI development. I believe the battle between Chinese and Western social media will escalate over the coming decade, but I think Meta has a good chance of maintaining its dominant position for the foreseeable future. However, investors who own Tencent Holdings and also capitalize off of a potentially dominant Chinese world economy in the future will likely see the largest outsized returns. I estimate that Meta shareholders will continue to do very well, including enjoying the newly issued dividends, which should grow in time. From my analysis that Meta is one of the greatest companies in the world with exceptional executive management, I rate the stock a Buy.

Q1 2024 Earnings Call Transcript")

")