Q1 2024 Earnings Call Transcript")

has set a new ATH leading altcoin season: $FLOKI, $SHIB to follow?")

Editor’s note: Seeking Alpha is proud to welcome James Cooper as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis

The oil and gas sector heavily favors shareholder payouts over project development. For Karoon Energy (OTCPK:KRNGF), however, its development pipeline offers a pathway for growth. With strong free cash flow in 2023 expected to continue into 2024 and 2025, the company is well-positioned to execute its development ambitions. Given recent production challenges and share price weakness, there’s an opportunity for investors to acquire this stock at a significant discount from six months ago.

Company Snapshot

Karoon is an ASX-listed oil and gas company that transitioned from a greenfield explorer to a significant oil producer in 2020. After successfully discovering the Poseidon gas project in Australia and divesting it to Origin Energy in 2014, Karoon has aggressively pursued a pathway toward becoming an oil producer. That began in 2020 when it acquired the offshore Baúna oil field in the Santos Basin.

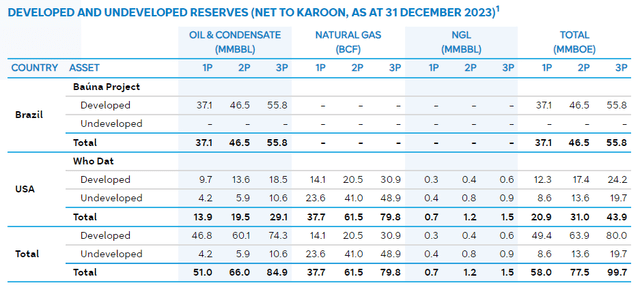

Since then, the company has rapidly grown its production profile. In FY23, the company produced 7.04 million barrels of oil, a 52% increase from FY22. Meanwhile, reserves across the full suite of operations total 235 million barrels of oil equivalent (mmboe). The reserve base is appropriately de-risked, with around 77.5 mmboe, or 33% of the total, falling in the probable (2P) category. Meanwhile, 58 mmboe sits within the measured (1P) category, or 25%.

Karoon Energy reserve and resource statement

As the company expands its footprint across the Santos Basin, it’s also developing a foothold in the world’s most sought-after O&G region, the Gulf of Mexico. With a healthy balance sheet, including manageable debt levels and record-free cash flow, the company is in a strong position to develop these projects. We’ll begin our analysis with an overview of the company’s core assets in the Santos Basin.

Business Overview: Baúna Acquisition

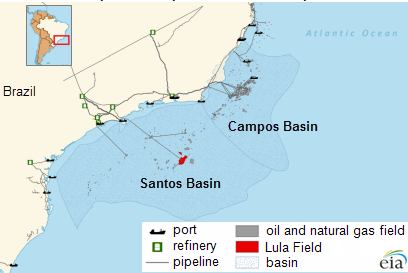

The company owns Baúna in the Santos Basin, southern Brazil, an active oil field. The basin is recognised as hosting one of the world’s largest offshore oil fields (according to NS Energy) and is known as Lula. Oil and gas explorers have probed this large sedimentary system for decades. But it wasn’t until 2007 that a large Brazilian state-run company, Petrobras, revealed its true potential. This oil giant initially discovered an 8 billion barrel well; for reference, that’s enough to meet 3 months of global demand.

US Energy Information Administration (EIA)

While not on the same scale, Baúna was part of Petrobras’s suite of discoveries happening at the time. In 2013, it offered its owners peak production of around 70,000 bopd (barrels of oil per day). But a decade later, production fell to just 14,000 bopd. By that point, Baúna had become marginal for this major state-run institution. The time had come to divest the project to a smaller player.

After offloading its Australian project to Origin Energy for around US$600 million, Karoon’s management team was interested. Despite falling production, Baúna offered strong free cash flow and significant infrastructure to build a presence in the Santos Basin. That included the capacity to process 80,000 barrels of oil per day and storage of 631,000 barrels.

The company reached a deal with Petrobras in 2020, acquiring the project for US $380 million plus oil-price-related contingent payments of US$285 million, assessable in 2026. Overall, Karoon timed the acquisition well. The deal occurred against a backdrop of historically low prices and poor sentiment, with crude prices falling below US$20 in 2020.

While Baúna had passed peak production, Karoon was committed to squeezing out more output by revamping the wells. That included replacing down-hole electric submersible pumps across the project’s two active wells. The project was completed in 2022. Along with several other production tweaks, Karoon successfully boosted annual output at Baúna by 11,000 bopd.

Pathway to Growth – Brazil

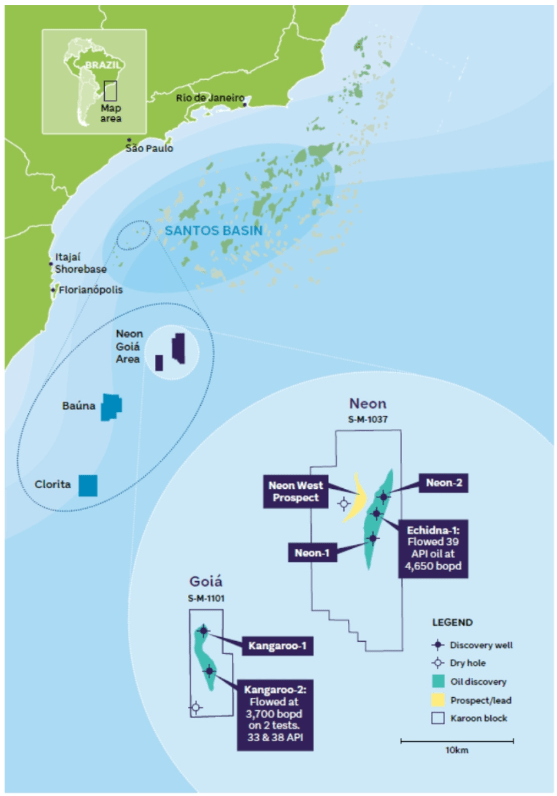

Given that Baúna is an aging oil field, executing a strategy focused on growth has been key. Bringing the company’s 100% owned Patola and Piracaba oil fields into production has been a major focus. The oil fields are located close to Baúna, enabling the company to use existing infrastructure. That enabled Karoon to bring these two oil fields on time and within budget last year. Patola and Piracaba have since delivered the company an additional 24,000 bopd from two active wells. Building on its presence within the Santos Basin, Karoon is also looking to develop opportunities in the Neon and Goia license blocks; see below:

Karoon Energy

Located less than 100km from its active production wells, these oil fields are part of Karoon’s legacy as a successful greenfield explorer. The company struck oil here in 2012 and has maintained an active presence in the Santos Basin ever since. Karoon’s proven discovery ability and technical expertise should bode well for future exploration campaigns. We’ll cover those shortly. For now, the company is evaluating Neon and Goia’s commercial feasibility. In recent tests, Neon returned 100 metres of oil-bearing reservoir with a flow rate of 4,650 bopd of high-quality oil. Investors should expect a final investment decision by 2025.

Pathway to Growth – Gulf of Mexico

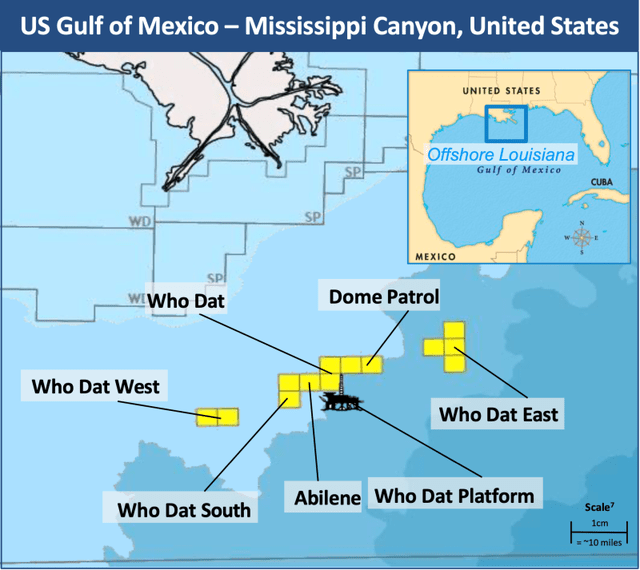

In December 2023, Karoon made a strategic 30% acquisition in the Who Dat and Dome Patrol oil and gas fields. The projects are located off the coast of Louisiana, USA and are clustered amongst a hive of oil and gas activity in the Gulf of Mexico. It funded the acquisition using a combination of debt, equity, and cash from its Baúna operation. Like its Brazilian acquisition strategy, the active oil fields will offer Karoon instant revenue with crude oil and natural gas exposure.

The company believes the acquisition will add 4 to 4.5 million barrels of oil (equivalent) in 2024. The purchase also offers Karoon strategic access to exploration tenure in the Gulf of Mexico. As part of the deal, Karoon will use the infrastructure at Who Dat and Dome Patrol to undertake joint venture exploration in 2024. Three deepwater holes are planned, offering investors near-term discovery upside. Given Karoon’s proven ability, this strategic move into the Gulf of Mexico has the potential to pay off.

Karoon Energy

Risks

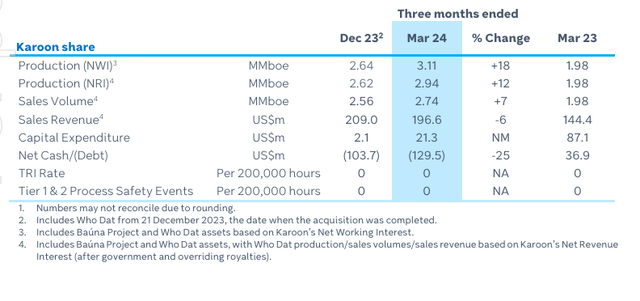

In its latest quarterly filing, the company reported an 18% lift in overall production from 2.64 to 3.11 million barrels of oil. Higher production numbers were driven by the Who Dat operation.

Karoon December Q23 Report

On the other hand, Baúna experienced a significant 15% decline from 2.53 million barrels to 2.16. As I’ve highlighted, Baúna has passed peak production, meaning natural production declines are to be expected.

However, according to the company, production was also impacted by gas dehydration problems, a process of removing water vapour from natural gas to prevent corrosion of pipelines and components. While Baúna is principally an oil operation, small quantities of natural gas should be expected, given that these two commodities coexist in fossil fuel basins. Natural gas is essentially ‘cooked’ crude oil. According to Karoon’s management team, the issue has been resolved, and the affected wells are now operating normally.

Denting its short-term outlook, the company has revised 2024 guidance to between 10.5 and 12.5 million barrels. Operational delays at Baúna have contributed to adjusted guidance. But Who Dat is also expected to have a shortfall over the coming months as operators tweak wells to boost the oil-to-natural gas output ratio. Given the ongoing depression in natural gas prices, the company is looking to increase oil extraction. This will impact output in 2024 as the company installs the necessary equipment to facilitate the changes. While there have been production challenges, the biggest risk remains on how well the company can execute its long-term growth strategy.

We’ll be looking for any updates on the commercial viability of its Brazilian developments. This will be critical as the company attempts to replace natural production declines at Baúna. As highlighted earlier, a final investment decision has been slated for FY25. Investors should assess any signals that may threaten the advancement of these projects. Flow rates, oil quality and production tests will be key measures.

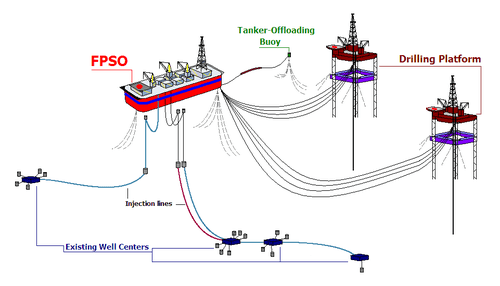

Another risk is that the company’s core assets and development projects are offshore. Unlike onshore projects, offshore developments require specific infrastructure and cargo vessels to transport oil. Known as Floating production storage and offloading (FPSO) vessels, these ships process and store hydrocarbons before offloading the fluids into oil tankers. They’re expensive and require significant maintenance. It’s just one example of the complexities involved in offshore extraction compared to oil or gas extraction on land.

Wikipedia

However, one advantage for Karoon is that its assets are relatively shallow. Baúna is 200 metres in depth, far shallower than many other oil fields in the Santos Basin, including the Lapa oil field, at around 2,140 metres.

It’s also worth considering the jurisdictional risk. According to a 2020 World Bank report, Brazil ranked 124th out of 190 countries in terms of overall ‘ease of doing business.’ That’s certainly nothing to brag about. Brazilian officials have a reputation for corruption; this has found its way into the oil and gas sector. In 2014, dozens of high-level businesspeople and politicians were indicted as part of widespread corruption charges centered around state-owned Petrobras. Investors should consider whether they’re happy to take on these risks.

Lastly, please note that Karoon trades on the OTC market, which can pose liquidity problems due to low trading volumes. Investors can reduce liquidity risk by trading on the company’s primary exchange in Australia. Here, the ticker code is ‘ASX: KAR.’

Valuation

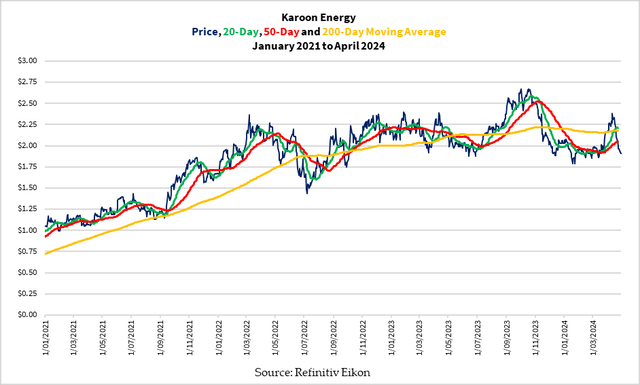

The company’s share price has fallen 30% since October 2023. Production downgrades have undoubtedly contributed to diminishing investor sentiment. Over the short term, the company needs to meet these operational challenges and ensure that the revised 2024 production guidance can be met. Another miss could be disastrous.

Refinitiv Eikon

While the company has encountered production hurdles, I’m confident it can overcome them. Karoon has a track record of delivering technical success, including bringing new oil fields into production within budget.

It has also successfully undertaken interventions at its maturing Baúna oil field to maximise cash flow and fund developments. Karoon has rapidly transitioned from greenfield explorer to oil producer in just four years and has built a sizeable portfolio of growth opportunities across two mature oil and gas provinces.

So, is the market overly focused on near-term production hurdles without appropriately factoring in the growth potential? With recent share price pressure, this stacks up as a possible value opportunity for investors. It offers attractive FY24 price-earnings of just 3.88X, rising moderately in FY25 to 4.07X. That compares favourably with other ASX-listed oil and gas producers.

|

Company |

Market Cap $AUD |

FY24 P/E Ratio |

FY25 P/E Ratio |

|

Karoon Energy |

1.56B |

3.88X |

4.07X |

|

Strike Energy |

0.63B |

24.3X |

16X |

|

Santos Limited |

16.2B |

11.8X |

11.5X |

|

Beach Energy |

3.67B |

-19.5X |

6.96X |

Source: Market Screener/James Cooper

Regarding valuation, Karoon has a 2.7X EV/EBITDA multiple and trades on par with its larger ASX-listed peers, Santos (OTCPK:STOSF)(ASX: STO) and Beach Energy (OTCPK:BEPTF) (ASX: BPT).

|

Company |

Market Cap $AUD |

FY23 EV/EBITDA |

|

Karoon Energy |

1.56B |

2.7X |

|

Strike Energy |

0.63B |

-82X |

|

Santos Limited |

16.2B |

5.3X |

|

Beach Energy |

3.67B |

3.13X |

Source: Market Screener/James Cooper

The company’s value relative to free cash flow also looks appealing. In FY23, EV/FCF stood at 3.8X and remains robust over FY24 to FY25. In comparison to the larger oil and gas producers, Karoon’s low EV/FCF ratio suggests that it may be undervalued in the sector.

|

Company |

Market Cap $AUD |

FY23 EV/FCF |

FY24 EV/FCF |

FY25 EV/FCF |

|

Karoon Energy |

1.56B |

3.8X |

4.0X |

2.0X |

|

Santos Limited |

16.2B |

9.9X |

37.0X |

13.3X |

|

Beach Energy |

3.67B |

nil |

nil |

12.4X |

Source: Market Screener/James Cooper

Balance Sheet Health

With that comes a healthy balance sheet. In its latest quarterly filing, Karoon reported a modest debt of around US$249 million and US$119.5 million in cash, which gives it a net debt position of US$129.5 million. The company reported declining unit production costs, falling 23% to US$11.09/boe. According to management, this primarily reflects higher production over a largely fixed cost base and improved efficiency across its FPSO vessel fleets compared to the previous period.

The healthy balance sheet was also strengthened by a net drop in capital expenditure on exploration, plant, and equipment. Year-on-year capital outlays have fallen from $US 87.1 million to just $US 21.3 million. However, investors should be aware of the higher capital costs in future years as the company advances the Brazilian developments and undertakes joint venture exploration drilling within the Gulf of Mexico.

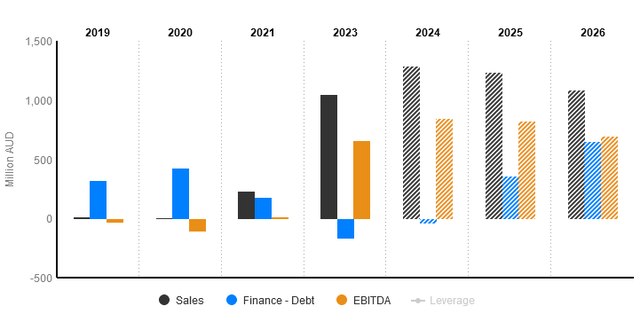

Overall, the strong balance sheet has been driven by strong sales volumes in 2023, reaching more than AUD$1.05 billion. This is expected to remain robust, with projected sales of AUD$1.29 billion in 2024 and AUD$1.22 billion in 2025. Despite recent guidance downgrades, EBITDA is still expected to be robust, peaking at $AUD 850 million in 2024 and remaining elevated over 2025/26.

Market Screener/S&P Global Market Intelligence

The latest results confirm that the Brazilian acquisition is starting to bear fruit. In 2023, the company delivered a strong free cash flow of AU$469.2 million. This is forecast to dip slightly in 2025 before rising to over AU$500 million in 2026.

In sum, low debt and strong projected sales over 2024 and 2025 should place the company in a robust position to execute development ambitions in Brazil and fund organic growth without relying on debt or capital raising. Overall, that reduces the risk of potential shareholder dilution.

Conclusion

Management has a demonstrable ability to target opportunities and deliver projects on cost and on time. Given oil and gas’s critical role in the global economy, demand is set to last far longer than most anticipate.

Meanwhile, the five ‘super-majors’ – BP, Shell, Chevron, ExxonMobil, and Total Energies—continue to lavish shareholders with dividend payments and share buybacks at the expense of growth. According to the Institute for Energy Economics and Financial Analysis (IEEFA), this totalled US$104 billion in 2022. The oil and gas industry is strongly biased toward making payouts ahead of developing new projects. That’s undoubtedly being driven by government disincentives that are preventing the development of new oil fields. That signals potential supply problems in the years ahead.

Is the market ready to put more value on Karoon’s pipeline of growth assets? Once cracks start emerging in the global oil and gas supply, I think it will. Given its healthy balance sheet, a strong pipeline of development projects and relative value to other ASX producers, Karoon could offer investors strong upside to higher oil and gas prices.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")