")

")

Freshpet, Inc. (NASDAQ:FRPT) is a front-runner in producing fresh food for animals. The company has little competition and is benefiting from pet humanization trends shifting pet food buying behaviors in its favor. Fresh dog food has grown by 86% since 2021. Customers are willing to pay premium prices to spoil their animals. Freshpet invested heavily in advertising over the last year to take advantage of these tailwinds, and FY2023 results showed upward trending results, with serious growth and positive EPS results in Q4 2023.

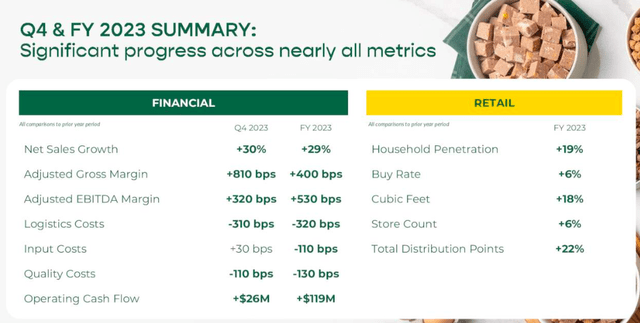

Q4 and FY2023 results (Investor presentation 2024)

However, the company has yet to deliver annual profits, has high capital expenditures, and has only recently improved its levered free cash flow trend, which remains negative. Freshpet is a company that could see significant growth on its own or even pique acquisition interest from traditional pet food players. The excitement around the company is apparent from the stock’s growth momentum. In the last six months, it has rewarded investors with returns of 83.97%, much higher than peers in the market. However, this has made the company very expensive relative to its peers, and short interest has increased to 11.24%, indicating negative market sentiment. Therefore, I recommend putting this stock on your radar but waiting for a better entry point.

Historic stock trend (SeekingAlpha.com)

Company overview and increasing brand awareness

Freshpet, founded in 2006, is a front-runner in producing fresh foods for cats and dogs, which has boomed alongside an increase in pets since the pandemic, the growing pet humanization trend and an increasing focus on health and wellness. Customers are willing to pay premium prices to treat their pets, and the company has capitalized on this by increasing its brand portfolio, product offering, and production capacity.

Company brands and products (Company website)

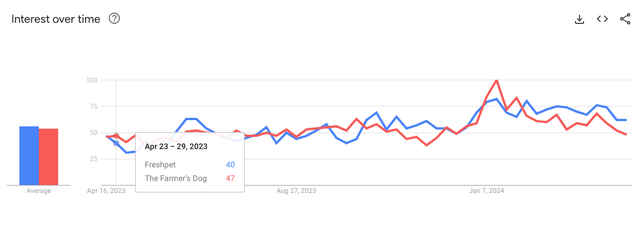

For the previous six financial years, revenue has increased annually by over 25%. Several interesting smaller players are pawing at the market, such as The Farmer’s Dog, which has a small annual revenue of $24 million, although it has a much larger following on social media. Freshpet will likely stay the dominant player for at least the next few years, with 96% of the market share in 2023 and heavily investing in advertising, growing its brand awareness through partnerships with celebrities such as a catchy song with Megan Trainer.

According to Google Trends, there is an increasing interest in Freshpet and The Farmer’s Dog.

12 month Google trend comparison in the United States (Trends.Google.com)

Expanding operations

It also invests significantly in R&D, ensuring its products are fresh by selling them in 26,777 stores across the USA and parts of Europe, using Freshpet fridges placed in the stores. Through its omnichannel strategy, it has reached over 11.5 million homes, a 19% year-over-year growth. The products are sold to a wide variety of large and small retailers through broker and distributor arrangements.

Freshpet fridges in stores such as Costco (Petfoodindustry.com)

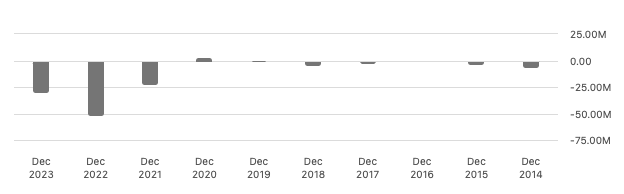

What the business is doing is not easy to replicate in my opinion, the setup includes complex processes and high maintenance costs. The company’s SG&A expenses exceeded the gross profit for the prior three financial years, leading to operating losses of negative $29.6 million in FY2023. What is great is that these losses have minimized for four consecutive quarters, and Q4 had a positive operating income of $15 million for the first time in the company’s history.

Annual operating income (SeekingAlpha.com)

Growth potential

The company still has a lot of growth potential, with a target of reaching 20 million homes by 2027. It could also look into expansion possibilities outside of the US. In FY2024, the company expects to generate revenue of more than $950 million and adjusted EBITDA of a maximum of $110 million. Furthermore, the company will spend around $210 million in CapEx.

Long term growth strategy (SeekingAlpha.com)

Financials

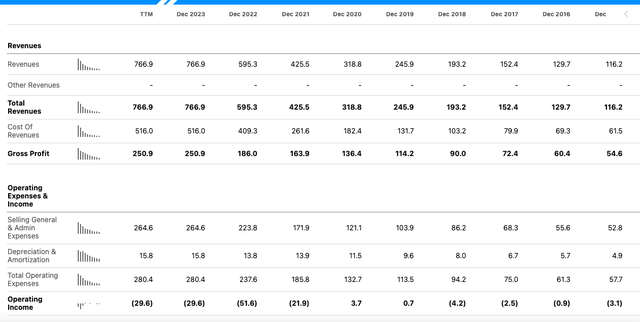

The company’s top line has more than doubled over the last five financial years. While the gross profit margin has declined significantly, it has increased year over year to 32.71% from 31.25% in FY2022. Operating income has improved YoY, although it is still negative at $29.6 million.

Annual revenue, gross profit and operating income (SeekingAlpha.com)

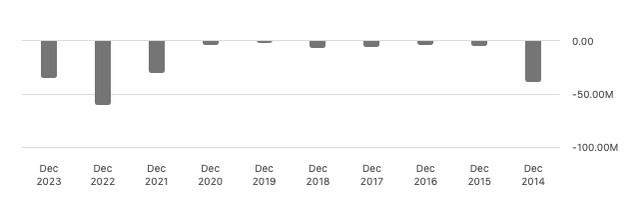

The company has yet to generate full-year profits. However, there has been a YoY improvement from negative $59.5 million in FY2022 to $33.6 million in FY2023.

Annual net income (SeekingAlpha.com)

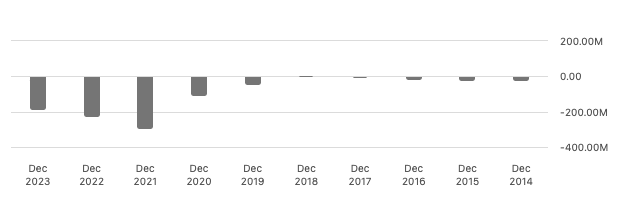

For the third consecutive year, the company has improved its levered free cash flow, although it is still negative $182.3 million in FY2023. This remains a concern as the business is still in the growth phase with high CapEx expenditures. To increase capital, the company has increased its outstanding shares, which increased to 48.2 million in FY2023 from 46.2 million. This negatively impacts the stock value for investors.

Annual levered free cash flow (SeekingAlpha.com)

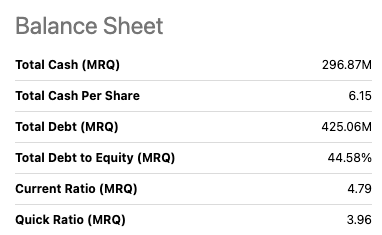

If we look at the balance sheet, we can see that the company’s cash position has improved YoY, more than doubled to $296.9 million. At the same time, the company has also taken on debt, which has increased to $425.06 million. We can see that the company is sufficiently liquid, with a current ratio of 4.79 and a quick ratio of 3.96. Management believes it has sufficient capital for growth in 2024 and will be cash flow positive by 2026.

Balance sheet overview (SeekingAlpha.com)

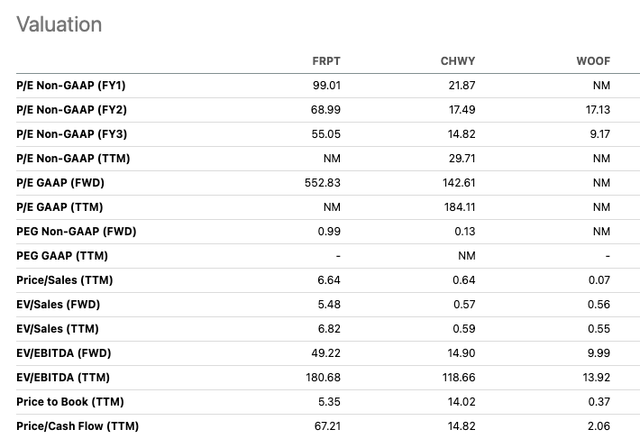

Valuation

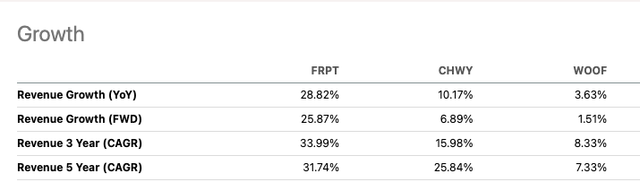

Freshpet’s stock has seen some major movement over the last six months, increasing by 82.52%. This momentum was driven by Q3 and Q4, beating EPS and revenue expectations. The company is capitalizing on an evolving pet food industry in which more customers seek fresh pet food. With little competition within the market, the company benefits generously from a growing demand. Compared to other pet stocks like Chewy (CHWY) and Petco (WOOF), Freshpet has more significant YoY revenue growth at 28.82% and is expanding its market share.

Revenue growth versus peers (SeekingAlpha.com)

However, the current stock price makes it less appealing to invest in the company. With a forward price-to-earnings ratio of 99.01, it’s pretty steep for a company that hasn’t yet posted annual profits. This ratio is also significantly higher than its industry peers and well above the consumer staple segment median of 17.12. When comparing the stock to its counterparts, justifying the premium price becomes more challenging. Furthermore, the short interest rate increased to 11.24%, which could increase the volatility of the stock.

Relative peer valuation (SeekingAlpha.com)

Risks

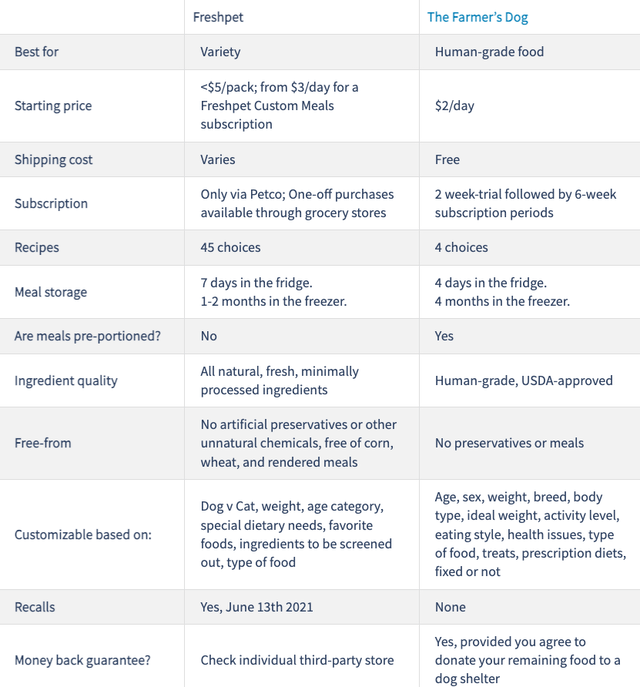

The company has a complex and costly logistics setup for its refrigerators, which are required to keep food fresh. In addition, maintenance costs are much higher than those of its dry product alternatives in the market. This could limit its pricing power, impacting its overall profitability. Furthermore, the company has not expanded outside of the US. This could open up the possibility of competitors entering the space as an opportunity exists. Although Freshpet almost has a monopoly within the fresh pet food market, we can see that smaller company Farmer’s Dog has a much larger social media following and is sold directly to the customer in a more customizable fashion at better pricing points. Increased competition could negatively impact the business.

Freshpet versus The Farmer’s Dog (Petfoodprocessing.net)

Final thoughts

Freshpet is an exciting company as it is in a great position to benefit from the growing pet humanization trends. Furthermore, it is investing in expanding its production capabilities, R&D, and advertising to increase the number and quality of products and improve its brand awareness. The company has had a great financial year, but the stock price has shot up in the last six months well above an attractive entry point if we compare it to other peers in the market and it has yet to deliver annual profitability. Therefore, for now, I recommend a wait-and-see hold rating.

")

")

Q1 2024 Earnings Call Transcript")