")

On Monday, April 29th, Annovis Bio (NYSE:ANVS) announced the topline results from their phase 2/3 Alzheimer’s Disease (AD) trial. This trial was described as:

The Phase II/III study was a randomized, double-blind, placebo-controlled trial investigating the efficacy, safety, and tolerability of buntanetap in patients with mild to moderate AD. This was a dose-ranging study where patients received either one of three doses of buntanetap (7.5mg, 15mg, or 30mg) or placebo on top of their standard of care for 12 weeks. In this study, over 700 patients were screened, a total of 353 patients were enrolled, and 325 patients completed the study across 54 sites in the US. The study included mild to moderate AD patients whose Mini Mental State Examination (MMSE) scores at baseline ranged from 14 to 24.

(Source; Bold emphasis added)

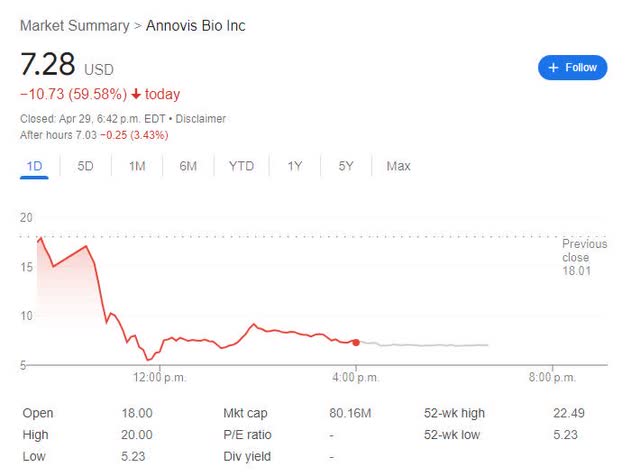

Despite a very positive headline that reads: “Annovis Bio Announces Statistically Significant Phase II/III Data in Patients With Early Alzheimer’s Disease”, the market reacted negatively to the news by sending the stock down ~60%, i.e. from a close of $18.01 on April 28 to $7.28 on April 29.

ANVS 1-day chart ending on April 29, 2024 (Google)

To understand this dramatic market reaction, one first needs to understand the results. Let’s now take a look.

Pre-specified [efficacy] endpoints

According to the trial protocol (NCT05686044), there are 2 co-primary efficacy endpoints*, i.e. ADAS-Cog11 and ADCS-CGIC, and 3 secondary efficacy endpoints*, i.e. ADCS-ADL, MMSE, and DSST.

*Note: please check the protocol for the full names of these endpoints.

Of the 5 efficacy endpoints (2 co-primary and 3 secondary), only the ADAS-Cog11 data is reported in some details.

It should be noted here that per the announcement, there was no statistically-significant [improvement] data in ADCS-CGIC (co-primary endpoint) and in ADCS-ADL (a secondary endpoint)

In addition, neither MMSE nor DSST (both secondary endpoints) results were disclosed.

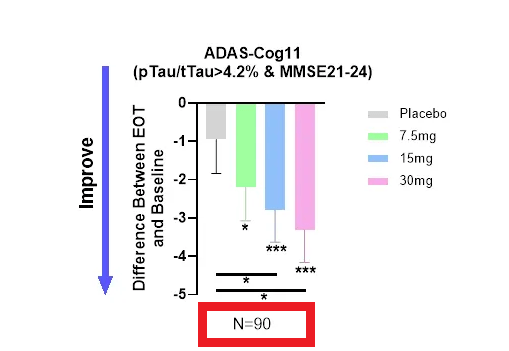

ADAS-Cog 11 data from a non pre-specified subgroup (n=90), of a bigger, non-prespecified subgroup (n=202)

According to PR:

We observed a significantly higher improvement in ADAS-Cog 11 scores in each treatment dose relative to placebo for patients with mild AD. The analysis focused on biomarker-positive early AD patients (MMSE 21-24, pTau217/tTau≥4.2%) found that ADAS-Cog 11 was highly statistically significant at all 3 dose levels and in the combined dose levels compared to placebo as well as to baseline (Figure 1)

Dosedependent improvement in cognition in the population with confirmed early AD (ANVS April 29, 2024 PR)

(Red box added by author)

For this section, there’s one important item (Note 2) to pay attention to in the PR, see the screenshot below.

ANVS April 29, 2024 PR

(color boxes added)

In summary: For the ADAS-Cog 11 measurement, the company did not report any original data from the completed patients (n=350), i.e. the ITT (intend-to-treat) or the PP (per-protocol) patients, and reports, instead, only the data from ~28% (90/325) of the completed patients, cherry-picked post hoc by two non-prespecified selection criteria.

Safety, and Biomarker data

1. Safety

There is little specific information on the safety, except that according to the PR, “Buntanetap, a once-daily oral medicine [has] an exquisite safety profile” and was “very well tolerated”.

2. Biomarker

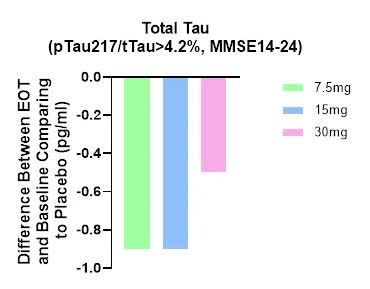

On biomarker data, the PR stated:

we observed a reduction in plasma tTau (total Tau) after treatment, providing further credence to buntanetap’s efficacy and mechanism of action (Figure 3).

ANVS April 29 PR

A few things worth noting here:

- Biomarker data is not dose-dependent and 30mg group had the smallest difference [the worst data].

- No biomarker data is presented for the whole group (n=325), nor for those who had the Tau ratio < or equal to 4.2% (n=123; i.e. 325-202)

- There is no p value given for these differences, i.e. likely no statistically-significant biomarker data, relative to the placebo group.

- Unlike the ADAS-Cog 11 data, the biomarker results were not “further sub-divided” into two groups (MMSE 14-20 vs. MMSE 21-24), nor shows any difference between these two sub-groups.

Discussion

As an R&D biotech investor, I find the space extremely discerning and punishing for trial failures and/or for any company who tries to sugarcoat their trial data.

In the case of Annovis Bio’s p2/3 AD results, both seem to be applicable.

Instead of presenting the real topline data, the company chose to report the post-hoc analysis as the only results, a likely indicator that the trial has failed in all five prespecified efficacy measurements in its ITT or PP patients (n=325).

In my opinion, such decisions/actions only discredit their R&D effort and harm their generalist investors who trust and defer to the company’s expertise to report trial data accurately.

In ANVS’ previous p2a AD trial, small patient numbers (n=14), and the short duration (25 days) were argued as the reasons why the trial did not have statistically-significant data; problems that this longer (12 weeks), bigger (n=325) p2/3 trial was supposed to fix. Evidently, this was not the case.

Again, the company seems to say that different sets of inclusion criteria, i.e. baseline Tao ratio (>4.2%) and baseline MMSE score (21-24) would fix the next trial.

In my opinion, the next AD trial will likely share the same fate as the previous two trials (p2a and this current p2/3), if/when ANVS raises enough money and the FDA clears it, i.e. the next AD trial will likely again fail to meet the pre-specified efficacy endpoints in the pre-specified patients.

Such is the futility and unreliability of post-hoc analysis or cherry-picking and reporting the best data.

Financials

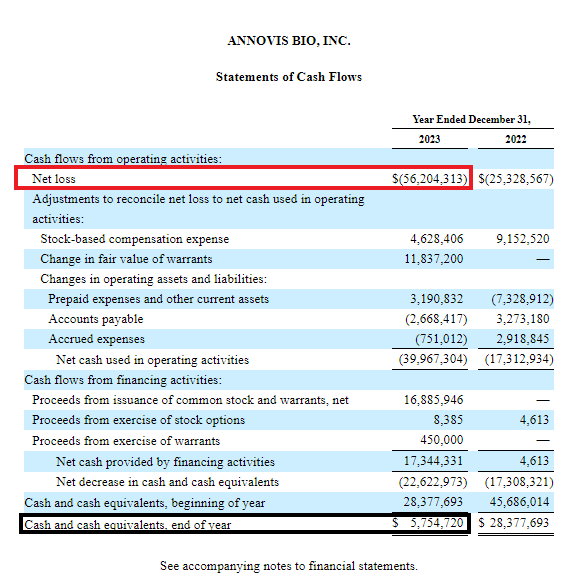

According to the 2023 Annual Report (see below, F-7), the annual net loss was $56.2M.

As of December 31, 2023, the cash and cash equivalent was of $5.75M.

ANVS 2023 Annual Report

On April 25, 2024, ANVS entered into a common stock purchase agreement with “the Equity Line investor…whereby the Company may offer and sell, from time to time at its sole discretion, and whereby the ELOC Purchaser has committed to purchase, up to 2,051,428 shares of shares”, according to a recent SEC filing.

Conclusion

Annovis Bio is expecting another important readout from their p3 trial in Parkinson’s Disease (PD) soon.

It is possible, though improbable in my opinion, that the p3 PD trial will succeed where the p2/3 AD trial had failed in a longer, larger [than the previous p2] trial, given that the previous PD p2 trial had weak and mixed results.

For the rating, I choose STRONG SELL, as I estimate a low probability of success in the coming PD trial and even if the company chooses to press on in AD and PD, I estimate little to no probability that Buntanetap would ever be successfully developed/approved for these indications.