Overview

The Fidelity MSCI Energy Index ETF (NYSEARCA:FENY) is designed to offer investors exposure to the U.S. energy sector, aligning its performance with the MSCI USA IMI Energy Index. Principally, FENY invests at least 80% of its assets in securities that are included in its underlying index, adopting a representative sampling indexing strategy. This strategy involves selecting securities that represent the full index in terms of its characteristics such as market capitalization and industry weightings. As a sector-specific, passively managed ETF, it mainly invests in North American equities, with a strong focus on large- and mid-cap companies which are about 63% and 25% of the portfolio’s composition, respectively.

The ETF’s top holdings are Exxon Mobil and Chevron, and they make up over 35% of FENY’s assets combined, emphasizing the ETF’s exposure to the biggest players in the energy industry. The ETF has shown varied performance metrics over different periods, though it generally aims to capture the sector’s growth while offering a dividend yield of 2.84%. Notably, FENY operates with a low expense ratio of 0.08%, allowing investors to retain a larger portion of potential gains and dividends. This structural setup suits investors looking to gain efficient and focused exposure to the energy sector, particularly during times when the sector might present a value opportunity compared to others in the broader market.

Peer Comparison

Looking at its peers, FENY has many favorable characteristics. The main one is the low expense ratio, which is often the case for a Fidelity fund. At 0.08%, its expense ratio is cheaper than the most popular and oldest energy sector ETF, the Energy Select Sector SPDR Fund ETF (XLE), which is only slightly higher at 0.09%. However, when compared against other XLE alternatives, its expense ratio is highly favorable. In terms of its dividends, FENY offers a yield that is solid compared to its peers. XLE has a higher yield over the last year at 3.05% (vs FENY at 2.80%) and over the last four years at 5.08% (vs FENY at 4.53%), but FENY’s dividend growth rate in the last three years has been a bit stronger at 13.78% (vs XLE at 11.83%). When looking at the domain of XLE alternatives, FENY’s dividend yield is on the higher end. One similarity that FENY has with XLE is the concentration of its portfolio in its two main assets. Both have Exxon Mobil (XOM) and Chevron (CVX) composing over 35% of their holdings, and both have over 60% of the portfolio invested in the top ten holdings. The main difference in portfolios is that FENY has many smaller holdings and XLE is much more narrow.

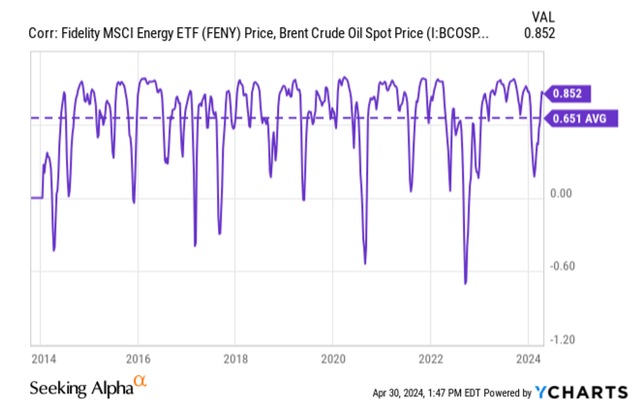

Oil Price Outlook

YCharts

The outlook for the price of oil is bullish for FENY (which is highly correlated with the Brent spot price), especially since the index has significant exposure to Exxon Mobil and Chevron. From the current view, where Brent trades around $88 and WTI trades just shy of $84, there are many reasons to believe that the price of oil is well-supported, and that upside risks outweigh downside risks.

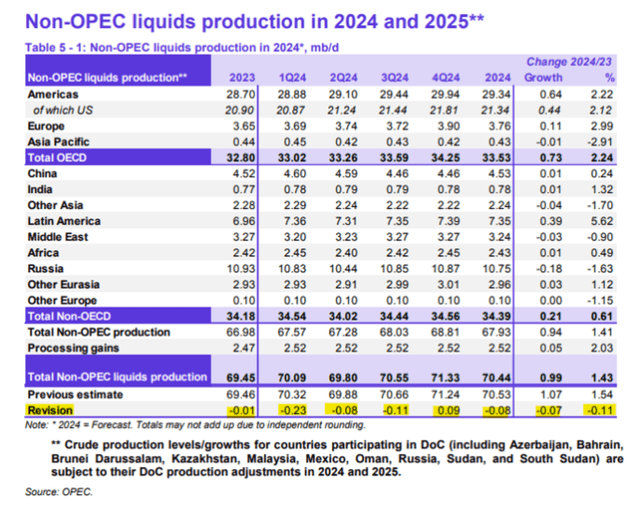

Supply

OPEC

The supply of oil looks to have little upside in 2024 as suggested by many organizations covering the topic. The EIA only predicts a 0.3 million b/d increase in production in 2024 in the US, well below the 1.0 million b/d increase last in 2023. Data from the latest Dallas Fed Energy Survey for Q1 2024, supports a view of limited US production growth. When asked about oil production, a net -4.1% of E&P firms said that production was increasing, meaning that there was a slight edge to firms that decreased output from Q4 2023 to Q1 2024. Looking more broadly, OPEC downgraded its view of oil production from countries not participating in OPEC’s supply adjustments by 0.1 million b/d to 1.2 million b/d in the April 2024 Monthly Oil Market Report. Paired with OPEC+ countries maintaining their supply cuts, it makes for a tighter supply outlook for the rest of 2024. ING highlighted that the continuation of supply cuts organized by OPEC+ is “moving the market from a surplus to a deficit in Q2 2024. “The broad trend seems to be that with interest rates high across the globe and the price of crude oil at post-pandemic highs, oil producers don’t feel the pressure to massively expand operations that would be costly to finance.

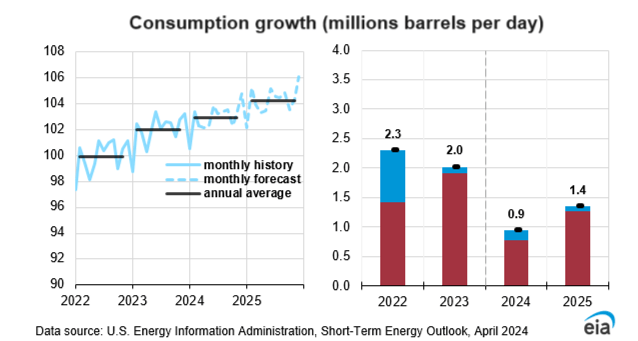

Demand

EIA

The demand for crude oil has been bolstered by strong economic fundamentals in the US that continues to surprise to the upside. In addition to revising its forecast for US production lower, the EIA revised its forecast of global oil consumption up by 0.4 million b/d to 102.9 million b/d in 2024 and by 0.5 million b/d to 104.3 million b/d in 2025. The US energy research agency points out that the combination of this upgrade in consumption with flat production will add upward pressure to oil prices. In the end, the EIA expects the tighter market balance to keep oil prices relatively elevated, with the price to average around $90 in Q2 2024. OPEC’s recent consumption forecast confirms the EIA’s view, with world oil demand growth of 2.2% expected in 2024. It also expected to see “robust oil demand” in the summer months this year, as a strong driving season is expected as a result of US economic resilience and the potential of a rebound in activity in China.

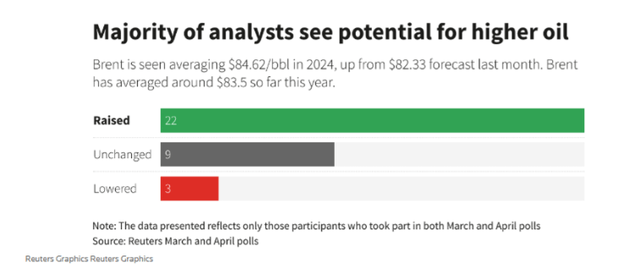

Geopolitical Tensions

Reuters

On top of bullish supply and demand fundamentals, there is more upside risk to the oil price outlook as a result of existing geopolitical tensions in the Middle East and in Ukraine, that have only been escalating. In Eastern Europe, the longer the fighting continues, the more likely energy infrastructure will be targeted. Recently, Ukrainian President Zelensky has reported that Russia is targeting “gas facilities important for supply to the European Union.” On the other side, the Ukrainian military has targeted Russian energy infrastructure and looks likely to continue attacking those targets, even though the US has asked Ukraine not to. In the Middle East, Iran’s attack on Israel suggested that the intensity of the conflict has reached an unprecedented level. In response to the recent escalation and the existing supply and demand, analysts are upgrading their views of the Brent spot price. Specifically, a Reuters poll in April found that 22 analysts raised their expectations of the Brent spot price vs. their expectations in March (9 didn’t change their expectations and 3 lowered).

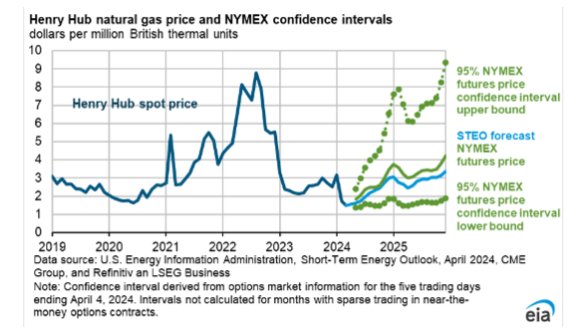

Natural Gas Outlook

EIA

A brief note on natural gas prices. The Henry Hub spot price looks to have bottomed after a mild winter in the US. Inventories are still very high, with storage levels 39% above the five-year average going into the spring. As a result of the high storage levels and the low spot prices (averaging around $1.80 in Q1 2024), US production is likely to be less than the beginning of 2024 in the coming quarters so that storage levels can stabilize. The EIA states that the US will produce less natural gas on average in Q2 2024 and Q3 2024 compared with Q1 2024. This should help natural gas prices to gradually rise throughout 2024, but not by much. The EIA currently expects natural gas prices to average $2.20 in 2024. The bottom line is that the worst of the weakness in natural gas prices is behind us, but it’s not a significant bullish driver for FENY, more neutral than anything.

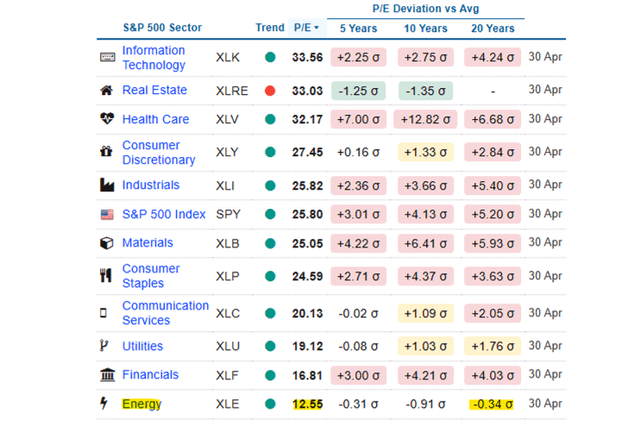

Valuation

World PE Ratio

Back in January, another Seeking Alpha author points out that with an average P/E ratio of 8x and an earnings yield of 12% suggests that the energy sector is “much cheaper than the overall market and support higher dividends.” As of the end of April, that P/E ratio has grown to around 12.5x, and this is mostly due to strong YTD performance of 15.5% (FENY performance). Compared to the broader S&P 500 P/E ratio of 25.8x, this still looks pretty cheap, especially when it looks like energy companies like Exxon Mobil and Chevron will be able to maintain healthy profit margins through the rest of the year on rising energy commodity prices. In a long-term view that ignores the poor performance of the energy sector during the pandemic, the 12.5x P/E ratio is about 0.34 standard deviations below the 10-year average P/E ratio for the sector of 14.3x which actually makes it one of the cheapest sector valuations in the pure context of earnings.

Conclusion

The Fidelity MSCI Energy Index ETF presents a compelling investment opportunity for those looking to gain exposure to the energy sector. With its low expense ratio of 0.08%, FENY offers a cost-effective way to tap into the sector’s growth potential. The ETF’s portfolio, dominated by Exxon Mobil and Chevron, is well-positioned to benefit from the expected rise in energy commodity prices, driven by supportive supply and demand fundamentals. Additionally, the energy sector’s relatively cheap valuation compared to its historical average and the broader market suggests that FENY has room for upside. As the oil price outlook remains bullish, and the natural gas price is expected to stabilize, FENY is an attractive option for investors seeking to capitalize on the energy sector’s potential growth.