")

")

The iShares MSCI Australia ETF (NYSEARCA:EWA) experienced positive performance in 2023, printing +13.98% in returns for 2023. While this could be considered underwhelming when compared to the US and other developed markets, it has some real bright spots; an attractive dividend profile, some diversification characteristics, and offers a niche investment opportunity for the region. The current state-of-play is positive, though based on current valuations and some macro headwinds I rate EWA at a hold for now.

An anomaly in the Asia Pacific Region

Australia has my attention for several reasons. It is a stable and prosperous industrialized nation with relative proximity to Asia. We are in an era of shifting geopolitical alignment and as US/China relations have soured in the recent period, I find myself looking to countries in the region that might be of strategic importance, and Australia is one of them. We are seeing a rise in cooperation and investment between Australia and other global powers in response to China’s saber-rattling. Just last week the UK and Australia signed a mutual defense agreement to enhance maritime security.

The country’s macro environment is tepid but still positive. According to the OECD, 2O24 GDP is projected to slow to 1.4% compared with 1.9% in 2023, while then again regaining steam in 2025 growing to 2.1% in 2025. In terms of the monetary environment, inflation is on a downtrend. The Reserve Bank of Australia kept rates steady at 4.35% at last week’s meeting. Contrasting with many central banks’ messaging, it remained ambiguous about the direction that rates would head. The Aussie dollar dipped on the result of the meeting, suggesting that investors are betting on a rate reduction sometime soon. This could be a benefit for Australia’s mining sector (and the fund, which has a large allocation to basic materials), as a devalued currency often helps exports. One area of concern, however, is how a reduced interest rate environment might impact net interest margin on the financials sector in EWA.

OECD

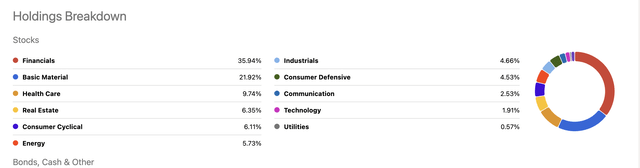

EWA holdings

EWA is a $1.9B ETF, with 73 holdings as of writing. The fund has a 25+ year track record, having been incepted with the initial slew of single-country ETFs from iShares in 1996. The fund is financials heavy ETF, owing ~36% to the sector. The next largest allocations are to basic materials ~22%, followed by health ~10%.

Seeking Alpha

The top 10 holdings for the fund account for about 60% of total assets, with the largest (~12%) allocation going to the multinational mining company, BHP Group (BHP). This is no surprise that Australia is one of the premier locations for mining globally. The second largest allocation goes to the financials giant Commonwealth Bank of Australia (OTCPK:CBAUF) with ~10%.

Seeking Alpha

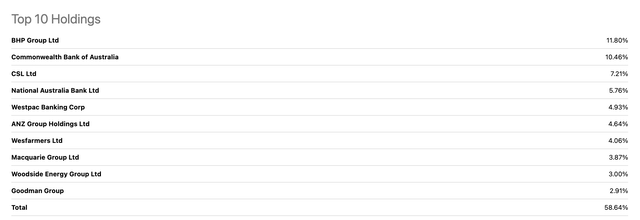

Outflows dominating YTD

EWA has seen recent periods of major outflows. In 2021, there were net outflows of $476M, while YTD the fund has also seen large outflows of ~$250M. There were no major market movements since January that would incentivize a sudden flight away from EWA. However, major institutional investors could have rebalanced away from the fund contributing to the size of outflows.

ETF.COM

Some diversification benefits

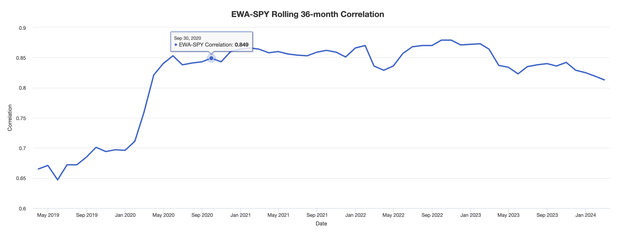

When looking at the rolling 36-month correlations over the last 5 years, we see that EWA has had some periods of low correlation with US stocks, using the SPDR S&P 500 ETF (SPY) as a proxy for US markets. Although correlations have risen more recently, EWA is able to lend itself as a diversifier. It is a developed, industrialized country that is located in Asia Pacific. This makes it a pretty niche market.

Portfolio Visualizer

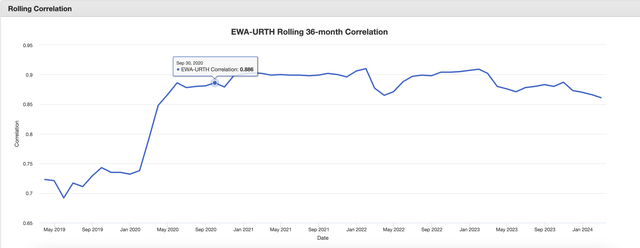

We see here that EWA generally has a somewhat higher correlation with global stocks, using the iShares MSCI World (URTH) as a proxy, although it has also had periods where correlations trended lower.

Portfolio Visualizer

Offering yield, but not as much value

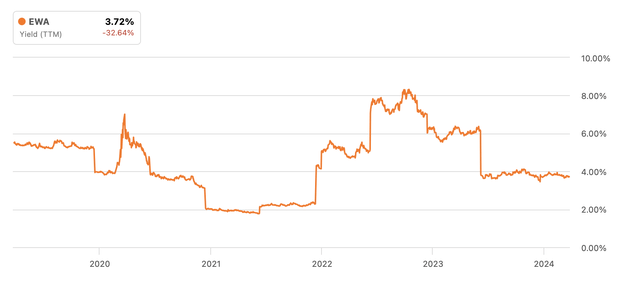

EWA’s current 12-month trailing yield is 3.78%, making it more attractive from an income perspective. It has trended towards higher than average yields in the past, though we don’t always see consistent and consecutive dividend growth. Valuation multiples are less attractive with a 17.99x P/E ratio and a 2.37x P/B and are a key reason I feel hesitant about EWA at the moment.

Seeking Alpha

Closing thoughts

EWA has some solid component parts and it has a good foundation in the Australian economy. The country is facing challenges that are nearly omnipresent. Its yield profile is attractive, and though it hasn’t always provided consistent dividend growth, the yields remain above average. The fund has demonstrated in the past that it can offer some diversification benefits to developed markets. However, I believe the market has priced in much of what it has to offer at this point. I’ll be paying attention to how this story unfolds, but I rate EWA as a hold for now.

")

")

Q1 2024 Earnings Call Transcript")