")

Danaos (NYSE:DAC) is a Greek shipping company with 68 owned and/or operated containerships, mostly transiting goods to Europe, Asia and Australia. I wrote two bullish articles on the company last year (June) (October), starting at a share price of $60. Over the last 10 months, DAC has performed well for shareholders with a +21% total return vs. the equivalent-period S&P 500 gain of +18%. Nothing spectacular, yet I would have guessed this outcome as closer to a minimum return with the general equity market rising, based on all the accretive math for earnings and quickly rising tangible book value.

The bullish news is Danaos is even MORE undervalued today than in June 2023, against simple arithmetic calculations, accretive financial changes taking place, and the rising relative valuation level of all U.S. equities. Management continues to plug along in a conservative fashion: buying back shares, purchasing several new ships, paying a dividend, and reducing net debt.

The balance sheet is moving into an A+ position compared to alternative deep-cyclical business models. Easily sellable and converted current assets like investments, inventory, accounts receivable, plus cash holdings represent a far greater number than its debt and long-term liabilities. In fact, $3.66 billion in total assets ($500 million in current assets) stacked up nicely vs. just $645 million in total liabilities at the end of December. This financial design is incredibly rare in the maritime shipping industry, and absolutely worthy of investor consideration for purchase.

In the end, DAC also represents one of the strongest net-asset buys on Wall Street today. Don’t laugh, but I am coming up with an easy to understand “fair value” for shares north of $150 vs. the current $74 quote. That’s a 50% discount to underlying accounting worth, with a superb management team, simple business model, and hard-asset ocean vessels (inflation winners) supporting future gains in your portfolio.

While a recession could keep the price from rising this year, I don’t believe much sustainable downside is part of the investment equation from $74 per share. And, for long-term owners, an eventual move to $150 or even $200 over several years appears to be the most likely statistical move from April 2024. So, I am keeping my Strong Buy rating on DAC. Let me explain some of the math.

Danaos Website Homepage – April 26th, 2024

Net Asset Play

The best buy-supportive argument to own Danaos is the net cost accounting and depreciated value of its ships plus current assets is far above today’s stock price. What do I mean? The maritime shipping industry is incredibly capital intensive, where major debts and liabilities are taken out against the underlying hard-asset value of ocean vessels. So, limited liabilities/debts present a clear competitive advantage for both business growth and owner profits.

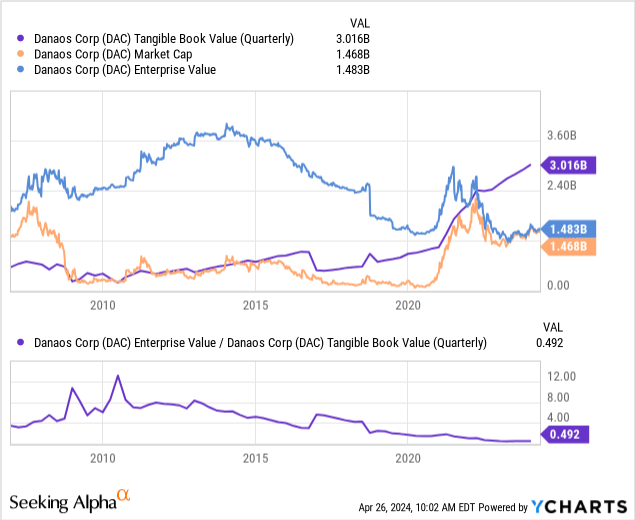

To be honest, I do not know of another major shipping or transportation company now selling well below tangible book value ($155 per share in December), with customer charter contracts price-locked to deliver a high level of earnings, holding little net debt on the balance sheet. Danaos is the only name to fit this formula for success.

When we look at the company’s equity market capitalization and enterprise value (EV adds debt to equity totals, then subtracts cash on hand), both are now trading dramatically below the tangible book value of hard assets minus all liabilities. A 50% discount for price to book value is somewhat common over the years in the shipping industry because of wild cyclical swings in transportation rental/charter rates charged customers, affecting final income levels for the business. Another reason overseas shipping companies can trade at steep discounts to book value is the solvency risk excessive debts carry. Interest rates can change in a negative way, raising borrowing and refinancing costs, while too much debt can/will bankrupt your company in a severe global economic contraction.

However, DAC doesn’t carry much in the way of debt today. Its cash balances are elevated and growing, earning 5% for yield. Interest costs on debt are in the 6% to 7% range. Net interest expense (subtracting cash interest gains from total interest paid) last year was only $11 million on $973 million in revenue (1.1% of sales). Compared to $192 million for interest expense on $552 million in sales (34.8% of sales) a decade ago during 2014, you can see how the business has totally transformed itself into a profit-making machine for shareholders.

What really catches my attention is the enterprise value calculation vs. tangible book value is screaming at investors that the current company valuation as a whole makes absolutely no sense. Against a median annual “average” EV multiple of 4x on tangible book value over the last 17 years (New York trading began for the security in late 2006), today’s 0.49x ratio is a rare bargain, representing a deep-value play for investors. Effectively, your investment capital is being exchanged for ships at HALF their accounting value. But this is just part of the good news for shareholders.

YCharts – Danaos, Tangible BV vs. Market Cap & EV, Since 2007

Amazingly Low Valuation on Earnings

Just as important for new buyers, the ratio of share price to all-but locked earnings is insanely low. While the S&P 500 index is trading at 25x income generation, Danaos can be purchased at 2.5x trailing income, a whopping 90% discount to the general market! During the peak day-rate period following the early days of the pandemic, management astutely signed long-term shipping contracts at elevated rates for years into the future.

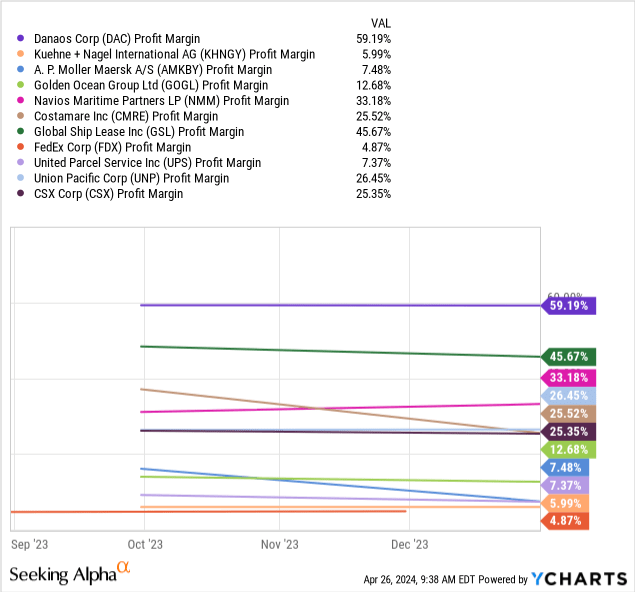

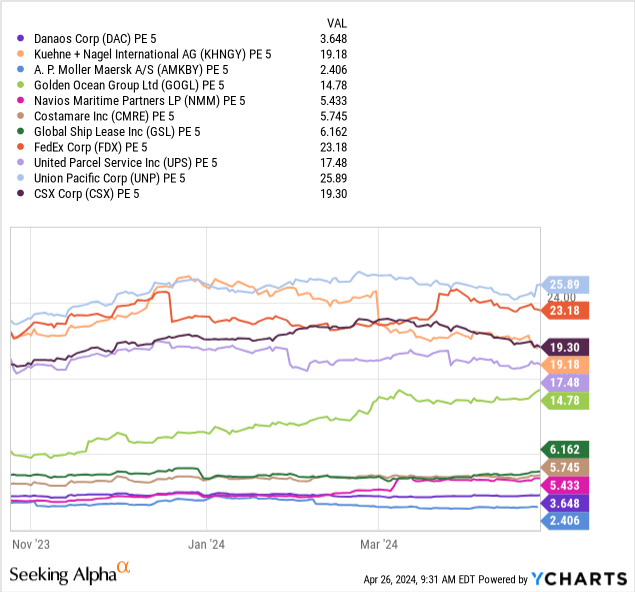

The profit margins resulting from high charter rates on its ships, in conjunction with the elimination of interest expense, have been mind-boggling positives vs. shipping peers. Today, DAC is the strongest profit-margin business in the transportation industry. Below I have drawn a comparison chart vs. other sea shipping names and a handful of transportation giants in America. A 59% after-tax margin on revenues is truly extraordinary vs. peers and competitors, with kudos owed to intelligent management decisions.

YCharts – Danaos vs. Major Shipping & Transportation Names, 2023 Profit Margins

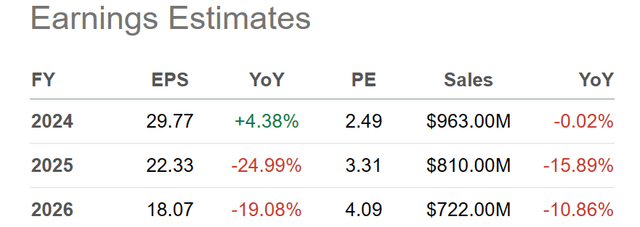

In summary… you are buying ships at 50 cents on the dollar, the company has little to no net debt and liabilities relative to assets owned (vastly reducing financial risk), AND Wall Street analysts are projecting you will get nearly all of your $74 per share investment back as after-tax earnings over the next three years! If you think about the puzzle I am explaining, buyers in the low-$70s are effectively purchasing $3 billion in ships for free right now, assuming you stay invested through 2026. The bottom line is management will have to do something ACCRETIVE with $70 in earnings per share over the next 36 months, while already sitting on $155 per share in tangible book value. It’s a unique win-win for shareholders.

Seeking Alpha Table – Danaos, Analyst Projections for 2024-26, Made April 25th, 2024

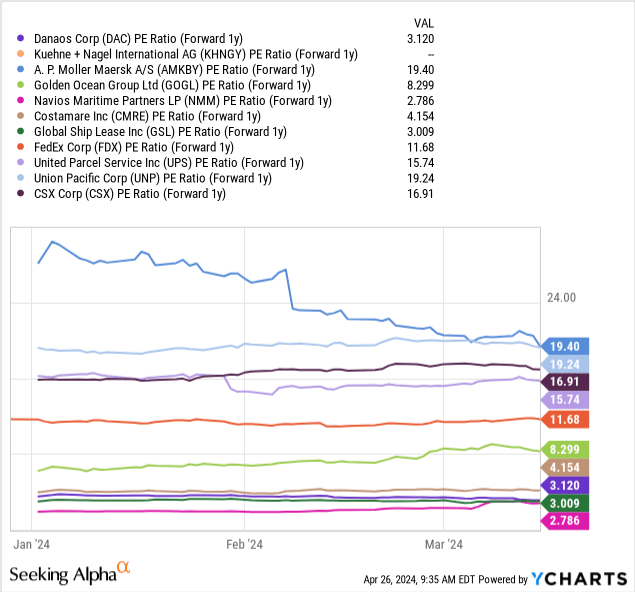

How low is the earnings valuation? Compared to my peer and competitor sort group, a 5-year average of share price to earnings generation (3.65x) puts DAC in the same undervaluation league as A.P. Moller Maersk A/S (OTCPK:AMKBY), another top and respected container shipping company in the world, alongside a better math investment setup than all the rest.

YCharts – Danaos vs. Major Shipping & Transportation Names, Price to 5-Year Average Earnings, 6 Months

Looking forward, DAC’s price to earnings ratio remains one of the cheapest in the group and on Wall Street overall. At what point will 3.1x earnings be considered too low, with a projection of 8 straight years around this number? Where’s the cyclicality? The advantage of owning DAC vs. AMBKY is the latter did not lock-in high customer rates. So, the forward/future valuation story again pushes Danaos as the champion undervaluation pick in the transportation sector.

YCharts – Danaos vs. Major Shipping & Transportation Names, Price to Forward Estimated Earnings, 4 Months

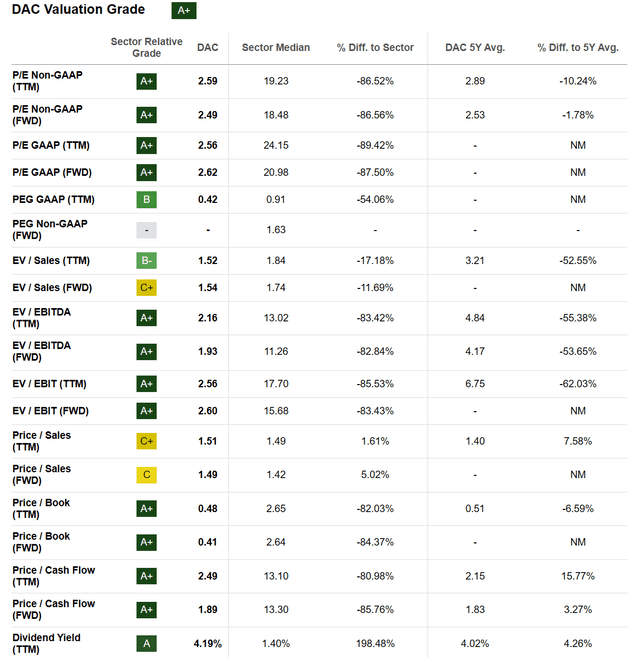

It goes without question Seeking Alpha’s quant computer-ranking system puts a Valuation Grade of “A+” on Danaos. My argument is the specific combination of positive factors for DAC should bring an even higher score, perhaps in the A++ range.

Seeking Alpha Table – Danaos, Quant Valuation Grade on April 25th, 2024

Technical Trading Pattern

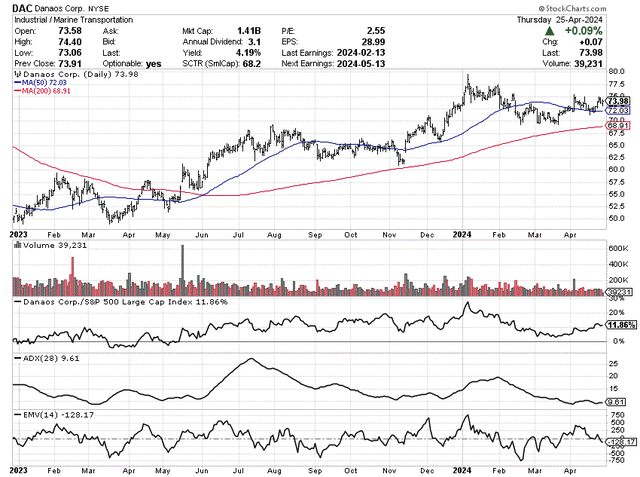

From a momentum readout perspective, DAC shares are moving in the right direction. Price is back above positive trending 50-day and 200-day moving averages, while the stock has outperformed the S&P 500 index for total returns from its bottom in early 2023.

In addition, low Average Directional Index readings in April indicate a solid balance between buyers and sellers. The 21-day ADX calculation under 10 is particularly bullish in this basing-pattern situation. Over the last 16 months, similar ADX scores have been highly correlated with successful times to buy shares, just before bulls have regained the upper hand over selling supply.

Lastly, the 14-day Ease of Movement indicator has recovered from noticeable selling in February, reversing to positive territory since late March. My view is more buyers than sellers are starting to appear. A deep-value starting point with limited share supply available for sale, taken together, is ripe for powerful price gains should any positive news in ocean freight/charter rate trends or an improving global economy (rising shipping volumes) appear in the near future.

StockCharts.com – Danaos, 16 Months of Daily Price & Volume Changes, Dividend Adjusted

Final Thoughts

How do I quantify downside risk? In a -50% crash scenario for the S&P 500, I am modeling Danaos should be able to hold on to $60 for price, representing -20% in price downside potential (ignoring cash dividend payouts). With future profits and cash flows largely locked-in, net cash holdings on the rise, and one of the lowest valuations of any U.S. stock already in place, plenty of new buyers (including management) will likely jump into the stock on a significant price decline from $74.

For sure, a severe recession shock could hold price under $70, as investors reevaluate what kind of earnings are possible after 2025-26. However, with almost $70 in after-tax “cash” projected to come in the door for DAC over the intermediate term, and few liabilities/debts needing repayment, I find it hard to believe a price well under $70 is sustainable for long.

On the upside, $150 for a quote over the next 12 months is a real possibility, which would deliver a better than +100% total return, when we include the indicated dividend rate of 4% yearly at $74 per share. The biggest kicker and bullish reason to own Danaos is the target potential for $200 to $250 per share (trading closer to tangible book value and 10x EPS) a few years out has some chance of coming to fruition. In terms of a deep-value pick, upside beyond 200% on your investment over 3-5 years is absolutely worth the inexpensive-valuation price of admission.

The company is buying back additional shares (at half their intrinsic worth) and could substantially raise the dividend this year. Rumblings about management (already owning a controlling stake) taking the company private do resonate with me. An outlier possibility is a larger transportation company tries a high-dollar takeover bid. I doubt insiders and major investors would be willing to sell for anything less than $120, when the company is worth $150+ today, moving to a number as high as $250 by 2026. Given the hugely accretive effect of aggressive share buybacks at 50 cents on the dollar and a decent global economic backdrop, DAC could be a top-performing transportation name to own over the next 2-3 years.

From my risk-reward analysis and personal experience trading stocks over 37 years, DAC remains a Strong Buy for most retail investor accounts.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

")

")