")

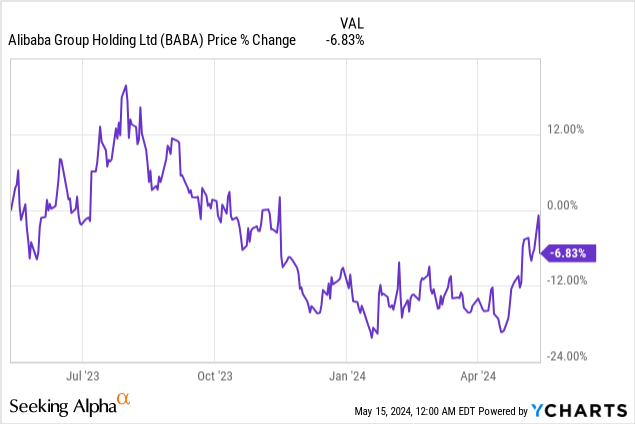

Shares of Alibaba (NYSE:BABA)(OTCPK:BABAF) slumped yet again after the e-Commerce company submitted its earnings sheet for the March quarter that unfortunately showed a 96% decline in profitability. However, Alibaba beat on the top line and saw encouraging results from its domestic e-Commerce business. Additionally, Alibaba is generating a ton of free cash flow, which, I feel, is still widely undervalued by the market. With a considerable amount of free cash flow from its e-Commerce enterprise, I believe Alibaba’s shares deserve a much higher valuation multiplier, especially now that the company also declared a special dividend in the amount of $0.66 per-ADS. Given the 6% drop in price after earnings, I believe investors are faced with another engagement opportunity!

Previous rating

I rated shares of Alibaba a buy previously (February 2024) due to the company trading at an attractive P/E ratio and insiders buying a ton of shares in the e-Commerce enterprise: Jack Ma And Joe Tsai Are Teaching The Market A Lesson. In the March quarter, Alibaba’s domestic e-Commerce business saw a bit of a rebound, driven by stronger order volumes, and the company continued to generate a ton of free cash flow that will be returned to shareholders going forward, in part through a special dividend. Based off of earnings and free cash flow, Alibaba represents top value for e-Commerce investors.

Alibaba beat top line estimates

e-Commerce company Alibaba beat the average Wall Street prediction on the top line, but missed on adjusted earnings by a lot due to the company reporting a large decline in earnings year over year (related to valuation changes for equity investments). Alibaba reported adjusted earnings of $1.40 per-ADS, which fell short of the consensus by $0.02. The top line was reported at $30.73 billion, which was $310M better than expected.

Alibaba’s e-Commerce business is on an upswing

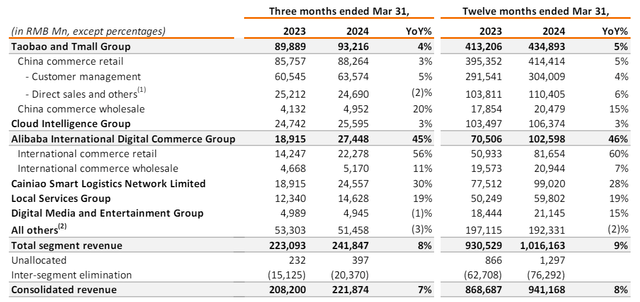

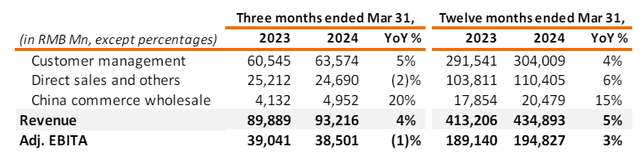

Compared to the previous quarter, Alibaba’s top line growth in its domestic e-Commerce division (Taobao and Tmall Group) doubled from 2% to 4% amid a recovery in the Chinese economy. The segment reported total revenues of 93.2B Chinese Yuan ($12.9B) with growth driven by online search results and purchase recommendations.

In total, Alibaba generated 221.9B Chinese Yuan ($30.7B) in revenues, showing 7% year-over-year growth as well. Alibaba’s revenue growth accelerated 2 PP compared to the previous quarter due to accelerating strength in the Chinese economy.

Alibaba

In the near term, I expect Alibaba to sustain this momentum in its biggest and most important segment in terms of revenue generation (Taobao and Tmall Group is responsible for 39% of all revenues): China’s economy is showing vital signs of a recovery as its economy grew 5.3% in the first-quarter, beating consensus expectations. This growth is driven by a robust consumer spending recovery after a 3-year long period of brutal COVID-19 lockdowns, as well as a rebound in manufacturing activity.

Alibaba’s Taobao and Tmall Group’s results were driven by growth in customer management, specifically growth in online gross merchandise value/GMV. GMV measures the amount of dollars that flows through an e-Commerce platform and is often regarded as an important KPI. Total segment revenue growth was 4% Y/Y, showing a 2 PP increase compared to the December quarter.

Alibaba

Alibaba’s key value is its free cash flow

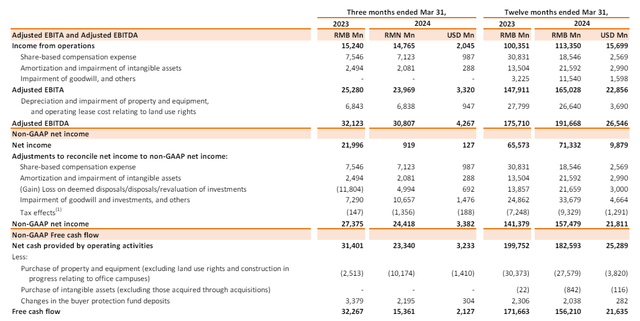

Alibaba’s free cash flow in the March quarter was 15.4B Chinese Yuan, which comes out to $2.1B. In the full financial year, Alibaba generated 156.2B Chinese Yuan ($21.6B) in free cash flow, which calculates to a quarterly average FCF of a massive $5.4B. This implies positive free cash flow of $1.8B per month!

From a free cash flow perspective, Alibaba is enormously profitable with a free cash flow margin of 17%, and it explains why the company earlier this year announced a $25B stock buyback. To further the appeal of Alibaba’s shares to investors, the e-Commerce company announced a special, one-time dividend of $0.66 per-share on Tuesday (which comes in addition to the annual $1.00 per-ADS dividend). This one-time dividend is a big deal for investors as Alibaba is gradually moving towards becoming a serious dividend stock: at a current price of $80, shares of Alibaba are set to yield approximately 2.1%.

Alibaba

Alibaba’s valuation

Alibaba is cheap based off of earnings and free cash flow, chiefly because U.S. investors are too scared to touch Chinese large-cap investments. There are some legitimate concerns relating to Chinese companies, as they don’t operate without government intervention, but I believe Alibaba’s focus on reorganizing its business into six different parts (last year’s reorganization plan) and returning much more of its free cash flow to shareholders are reasons why U.S. investors should take an investment in Alibaba seriously.

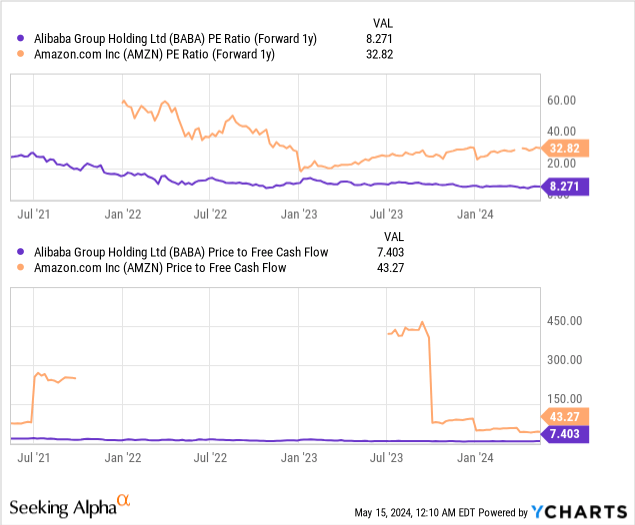

Shares of Alibaba are currently valued at a P/E ratio of 8.3X, which is significantly below the company’s 3-year average P/E ratio of 13.0X (reflecting a 36% discount). Alibaba is also trading at a much lower P/E ratio than Amazon (AMZN), which has a 32.8X P/E ratio. Amazon is more highly valued because it is a U.S.-domiciled company with considerable free cash flow growth prospects relating to its AWS Cloud business.

Amazon is also expected to grow its EPS faster than Alibaba in the near term (56% Y/Y growth for Amazon vs. 8% Y/Y for Alibaba in FY 2024). However, the extremely low valuation does not seem right to me, considering that Alibaba is enormously FCF-profitable and is now also paying special dividends. Given this backdrop, I believe Alibaba could trade at its 3-year average P/E ratio of 13X, which implies a fair value of ~$125.

Risks with Alibaba

Alibaba is still overly reliant on its domestic e-Commerce business. While the company has reorganized and split its business into 6 different reporting units last year, the domestic Chinese e-Commerce division is still responsible for the majority of the company’s revenues and income. From a diversification and revaluation point of view, Alibaba would be well-advised to reduce its reliance on Taobao and Tmall Group and develop its non-Chinese revenue streams. If Alibaba fails to do this going forward and continues to be overly reliant on domestic e-Commerce, I would be willing to change my opinion and rating on Alibaba.

Closing thoughts

Alibaba’s shares dropped 6% after earnings, but the company’s fourth fiscal quarter results were not that bad: the e-Commerce company doubled its revenue momentum Q/Q, driven by a focus on low-cost products in its domestic e-Commerce business and Alibaba continued to rake in a ton of free cash flow that will be returned to shareholders as part of its generous capital return plan (which now also includes special dividend). The Chinese economy is also showing vital signs of growth which could point to a robust consumer spending recovery in 2024… which is where Alibaba could handsomely profit as domestic e-Commerce is still by far the largest business segment for the company. From a valuation and dividend point of view, I believe Alibaba represents top value, especially for U.S. investors that want to diversify and invest in another e-Commerce giant other than Amazon.

Q2 2024 Earnings Call Transcript")