")

In my last article in February on CVR Partners (UAN), I wrote I thought the “Buy”-rated company would pay a higher variable distribution than it did in Q4 as fertilizer prices had rallied from their lows. With more data available on fertilizer prices, I wanted to update that outlook as well as look at a recent filing from CVR Energy (CVI) that its parent Icahn Enterprises (IEP) could look to acquire the rest of CVR Partners or sell its stake.

Q1 Adjusted EBITDA and Distribution Outlook

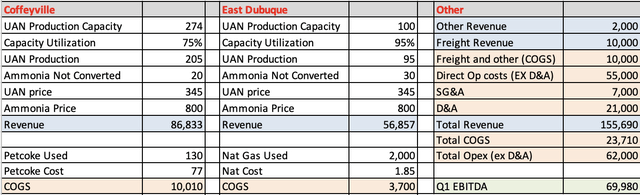

Looking at Q1, UAN and ammonia prices are much lower compared to last year, when the company reported adjusted EBITDA of $124.3 million. Its cash available for distribution was $110.3 million, after it reserved $19.5 million for maintenance capex and future turnarounds.

At the time, the company realized UAN prices of $457 per ton and ammonia prices of $888 per ton. It also received proceeds of $18.1 million from 45Q transactions. This year-over-year comparison will be very difficult.

UAN prices look pretty similar to Q4 prices, while ammonia prices are down slightly. However, CVR’s realized prices were relatively low in Q4 compared to market prices, reflecting forward sales prices. Given where Q1 and Q4 market prices were compared to the prices it realized in Q4, I would expect a nice increase in realized prices in Q1 compared to the Q4.

Nitrogen Fertilizer Prices (Progressive Farmer)

Based on average prices for UAN and ammonia over the past two quarters, I see CVR Partners generating around $70 million in Q1 adjusted EBITDA. That considers the downtime at its Coffeyville plant in the quarter, which had some scheduled maintenance planned. It’s much higher than the $37.9 million in adjusted EBITDA it produced in Q4, but much lower compared to a year ago.

CVR Partners EBITDA Projections (Self and filings)

As for its dividend, I’m going to assume around $15 million in reserves in the quarter. It has no big refinery turnarounds this year, but said it expects capex spending of between $9-13 million in the first quarter. I’ll add just a bit more in case of any issues with the Coffeyville maintenance to be conservative. Based on 10.57 million shares, that gets you to a distribution of about $5.20 per share. Now differences in commodity prices realized, utilization, and reserves taken can change that number quite dramatically.

The company is set to report its results next week.

Potential Sale

Now, the other big news about CVR Partners is that its parent CVR Energy revealed in a filing that Icahn Enterprises may look to acquire some or all of the shares of the fertilizer maker. It could move the other direction and also look to sell its stake. CVR Energy owns 36.8% of the outstanding common units of CVR Partners and its general partner. Icahn Enterprises, meanwhile, owns about 66% of CVR Energy.

Now IEP could buy CVR Partners in a negotiated deal, or it has a right to buy back the company at no less than current prices if its general partner, which is owned by CVR Energy, and affiliates own more than 80% of the company. That seems to suggest the most likely route would be a negotiated buyout.

Now there is a recent fertilizer plant deal in the works, with Orascom Constructions Industries (OCI) in the midst of selling a fertilizer plant in Iowa for $3.6 billion to Koch Ag & Energy Solutions. The seven-year-old plant produces roughly 2 million metric tons of nitrogen fertilizer, most of which is UAN. CVR Partners’ two plants combined produce about 1.6 million metric tons.

A similar valuation would value CVR Partners at about $2.9 billion, or about $227 a share. Now CVR Partners’ plants are much older and one does run on pet coke, so let’s apply a 20% to 30% discount and value them at between $2.0-2.3 billion. That would equate to $142-170 a share.

Now given Icahn’s limited call rights and the fact that CVR Partners is structured as an MLP, maybe Icahn can strike a deal below fair value, but I’d still see a deal in the $100-120 range.

Valuation

Given the potential sale of the company and with a recent sales comparison, I’d currently value CVR Partners based on the value of its plants, which I go into detail above. However, in determining my target, I do discount it back because of the favorable position Icahn finds himself in to help dictate a potential purchase. This is the best way to value the company, and how I valued it when working at a hedge fund. This valuation method eventually helped see a beaten-down stock increase over 10x off its lows.

However, if you want to value it based on EBITDA, you can. Above, I have the company generating about $70 million in EBITDA in Q1, which if you annualized for the full year based on current prices is $280 million. This assumes commodity prices stay the same throughout the year. Prices have gradually moved higher this year.

That would value CVR Partners at about 4.6x full year 2024 EBITDA. Bellwether CF Industries (CF), which is also its closest comp, trades at 7.7x the 2024 EBITDA consensus. Place a 6x multiple on CVR Partners, as it should trade discounted to CF given its size and older plants, and it would be a $114 stock.

Risks

Risks to the stock achieving my target would be Icahn deciding not to purchase the rest of the company or not selling his stake to another buyer.

Outside of that, commodity prices can be volatile. Nitrogen fertilizer prices were in a long bear market several years ago, and there are a lot of factors that can impact pricing. This can include everything from nitrogen fertilizer exports coming from China, to India consumption patterns. How much corn is planted, which uses a lot of nitrogen fertilizer, versus how much soybean is planted, which uses very little, can also impact demand and prices.

Naphtha prices, and in particular compared to U.S. natural gas prices, can also impact nitrogen fertilizer prices. The reason is cheap naphtha prices can bring foreign swing producers back to the market. Higher fertilizer prices can also lead to new facilities being built, which can cause supply demand imbalances as well and hurt prices.

And as for company-specific risks, CVR Partners only owns two facilities, so if there are any issues with its plants or long stretches of unplanned downtime, it could hurt its results proportionally more than larger fertilizer makers.

Conclusion

Based on the pending sale of the OCI plant to Koch and the cost to build a plant nowadays, CVR Partners’ two plants are quite valuable. I don’t think the market currently is pricing in the importance of fertilizer plants, especially given current geopolitical tensions. If Icahn is a buyer or seller, there should be some solid upside to CVR Partner shares in either scenario.

Barring a sale, fertilizer prices have continued to trend higher as we’ve moved into the spring. Current UAN prices are still below their 5-year average, so we are far from a fertilizer bull market. However, if the Port of Baltimore remains closed, it could push up UAN prices in the U.S. The port handles about 10% of the annual UAN imports to the United States.

Another interesting thing to consider is where those imports come from, and that is Russia. While Russia seems on the back burner given the tensions in the Middle East, relations between the U.S. and Russia also aren’t good given its current war in Ukraine. While the nitrogen fertilizer market is off its lows, there still could be some factors that help rally the market.

Given a potential sale to or by Icahn, as well as the current stake of the market, I’m going to maintain my “Buy” rating, while raising my price to $110 from $95, the midpoint of my discounted takeout target value listed above.

Q1 2024 Earnings Call Transcript")