")

Overview

Pacer US Cash Cows 100 ETF (BATS:COWZ) is an S&P 500 (SPY) beating ETF that focuses on companies with high cash flow which can grow dividends over time and have healthy balance sheets, with opportunities to capitalize on companies that are trading at a discount. I previously covered COWZ in November 2023 and the ETF has delivered a total return of 12% since then. Since my initial coverage, the holdings within the ETF have been rebalanced and now the weight of exposure to each sector has changed. Therefore, I thought it would be a good idea to provide follow-up coverage for COWZ to provide some insight into how the ETF has changed and what my expected outlook is in this current economic environment.

The latest CPI report concluded that inflation still sits higher than expected. As a result, we saw a negative market reaction with drops across the majority of sectors. For me, I see this as a huge buying opportunity because I think this reaction was a bit overdramatic. After all, the CPI climbed 0.4% over March, which was only slightly over the expected 0.3% rise. This translates into a longer period of elevated interest rates and a lowered probability that the Fed will start cutting rates this quarter.

Although the starting dividend yield is very low at 1.8%, I throw this fund into the same category as other dividend-focused ETFs alongside Schwab U.S. Dividend Equity ETF (SCHD). This is because the fund has averaged an excellent dividend growth rate since inception. I will touch on this dividend growth more in-depth further along in this article but first let’s dig into the revised holdings within.

Fund Style – Filtered For Quality

COWZ implements a passive management-styled approach which results in a total management fee of 0.49%. This means that there are no active managers that decide which companies the fund holds. Instead, holdings are chosen based on a formula that likely never changes. The fund has a strategy that filters potential holdings by market capitalization, ability to generate free cash flow yield, and companies that have an established history of increasing dividends. These metrics are all important because these are indicators of strong companies that are excelling in terms of profitability.

The process starts with the Russell 1000 Index consisting of 1,000 companies and a P/E (price to earnings) of 27.39x. From here, 100 companies are chosen and ranked by their free cash flow yields. These 100 holdings average out to a 7.66% free cash flow yield and a P/E of 11.54x. The free cash flow yield is an important metric that contributes to this formula’s success because it indicates the amount of cash flow a company generates relative to its market value. In short, a higher free cash flow yield is a good thing because it means that more cash is being earned relative to the company’s market price. This is an indicator that a company is undervalued, which is what helps contribute to COWZ’s superior price return.

The final part of the fund’s strategy is to take these 100 holdings and then rebalance them so that each position gets capped at a 2% weighting. This results in a final fund free cash flow rate of 7.88% and a P/E ratio of 11.77x. The fund’s holdings are reconstituted and rebalanced on a quarterly basis, which ensures that the fund is taking advantage of opportunities in the market. With this, the fund was recently reconstituted, so let’s review the updated holdings and structure.

Updated Holdings

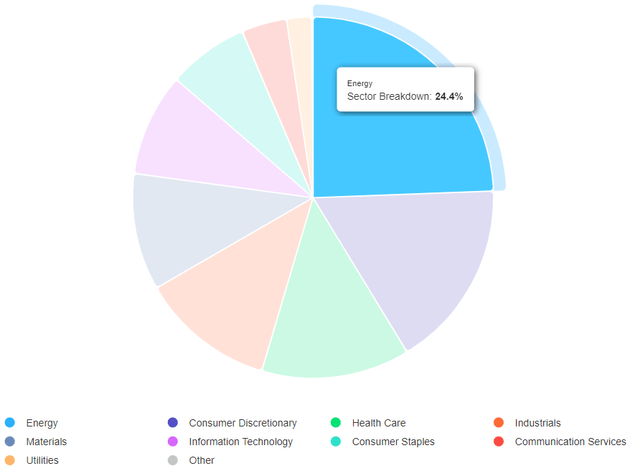

The fund currently has net assets totaling $22.5B culminating across 103 different holdings. The largest sector by weight is Energy, making up approximately 24.4% of the total breakdown. This is closely followed by the consumer discretionary sector which makes up 16.9% and the healthcare sector that makes up 13.3%. This essentially makes COWZ a bet on the energy sector more than anything else. Energy companies are typically cash flow rich due to the higher operating margins between the revenues and operating expenses.

Pacer ETFs

Like previously mentioned, the portfolio is rebalanced so that there are no holdings that have a weight over 2%. While 2% is the goal, some holdings inevitably grow in value to eventually become worth more than that 2% threshold. In fact, almost all the top ten holdings have grown to be worth more than 2% of net assets. As of the latest reconstitution, we see some changes from my initial coverage 6 months ago. For example, here are the most updated top ten holdings. The top ten holdings make up nearly 22% of the portfolio.

| Ticker | Holding | Weight |

|---|---|---|

| (MPC) | Marathon Petroleum Corporation | 2.33% |

| (VLO) | Valero Energy Corporation | 2.32% |

| (VST) | Vistra Corp. | 2.24% |

| (EOG) | EOG Resources, Inc. | 2.23% |

| (XOM) | Exxon Mobil Corporation | 2.21% |

| (OXY) | Occidental Petroleum Corporation | 2.17% |

| (FANG) | Diamondback Energy, Inc. | 2.16% |

| (DVN) | Devon Energy Corporation | 2.06% |

| (CVX) | Chevron Corporation | 2.01% |

| (CMI) | Cummins Inc. | 1.99% |

| Total | 21.72% |

The large majority of these top ten holdings have either reported great earnings or seen nice price growth. For example, Marathon Petroleum Corporation (MPC) is up over 37% YTD and generated $14.1B in net cash from operations according to their latest earnings report. Another example is Valero Energy Corporation (VLO); up 30% YTD in price and has recently increased their dividend by 4.9%.

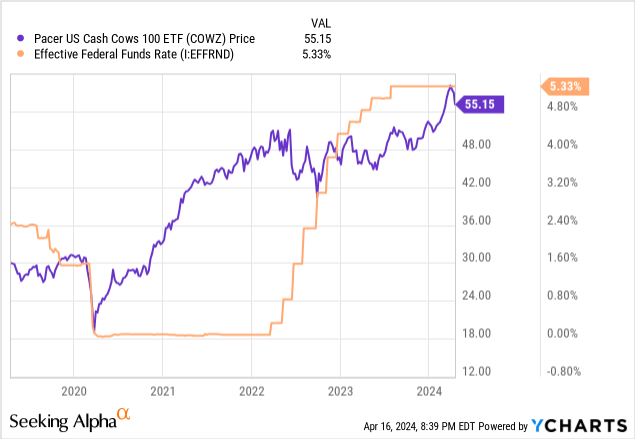

Although the history is short, we can see how the strategy implemented by COWZ offers stability to interest rate sensitivity. When rates were cut in 2020, the price ultimately ended up rising through 2021. Once rates began to increase at rapid rates, we can see that the price traded sideways for a bit but remained stable. This stability offers peace of mind that the COWZ strategy works in providing total returns throughout different market cycles. Now that it seems like rates are not going to get cut anytime soon, COWZ would be a great ETF to ride out the future of anticipated higher rates.

Energy companies can rely on debt to finance capital expenditures like expansion, ESG initiatives, infrastructure, research, and development. These elevated interest rates increase the costs of borrowing and interest payments on existing debt. This concept also applies to all other companies across the other sectors not related to energy. Most companies offset this by temporarily reducing expenses and maybe even cutting headcount.

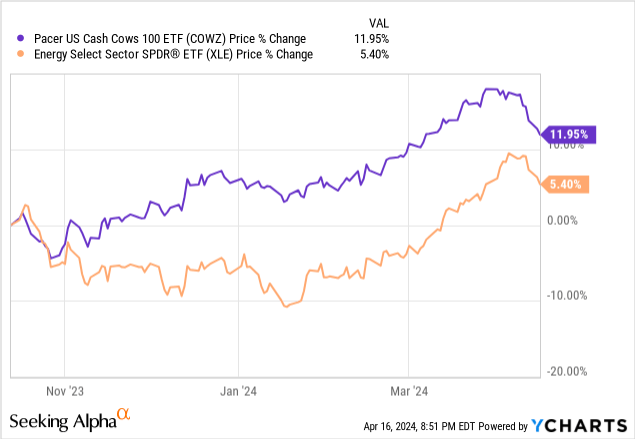

In addition, we’ve already seen the volatility that can be caused when the topic of conversation comes to interest rates. In fact, Jerome Powell’s Fed meetings were found to be three times more volatile than his predecessors. COWZ offers a better sense of stability during these moments of higher volatility. Even over a 6-month period, we can see that COWZ tested a much higher price low than the XLE. While the XLE briefly dipped into red territory, COWZ recovered out of the red nearly a whole 3 months before the XLE did.

Good Entry Opportunity

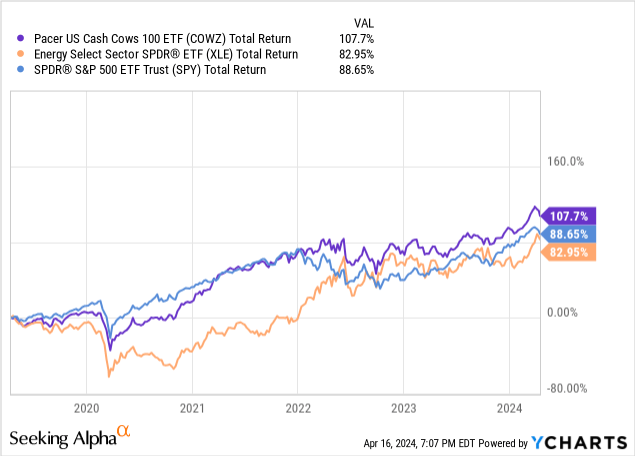

We can see how COWZ has outperformed the S&P 500 (SPY) as well as the Energy Sector ETF (XLE) in total return. The outperformance margin started to widen back in 2022 which shows that COWZ’s system of choosing high quality, free cash flow yielding businesses delivers better results. While the price currently sits near the all-time high of $58.48 per share, I still believe there is tremendous opportunity in holding shares of COWZ here for the long term. An investment in COWZ is similar to an investment in SCHD. What I mean is that an investment in either of these funds means that you have to believe in the formula and strategy that they follow.

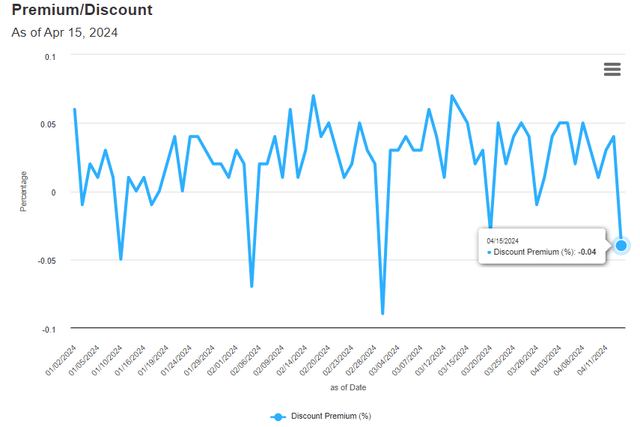

The price trades at a small discount to NAV (net asset value). While the discount itself isn’t what’s important, since the discount is practically immaterial at -0.04%. However, it’s worth pointing out that for the year 2024, the fund has traded at a very small premium for 64 days. COWZ has traded at a discount to NAV for only 8 days of the year so far.

Pacer ETF

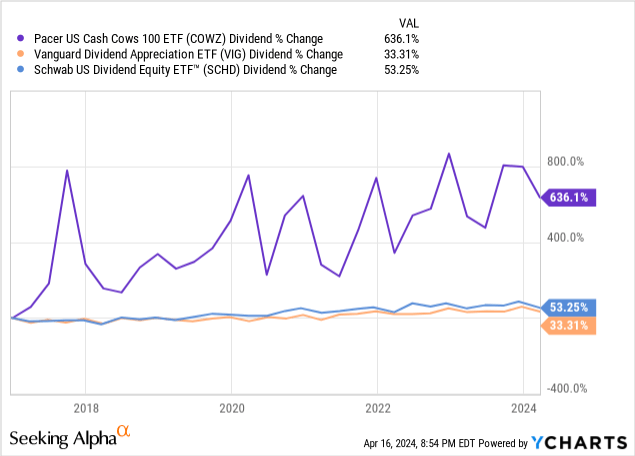

As of the latest declared quarterly dividend of $0.2443 per share, the starting dividend yield sits at 1.8%. While this certainly isn’t a large enough yield to generate any sort of meaningful dividend income, unless you take on a large position greater than $1M, the dividend yield is not the main appeal here. While the fund’s inception was only in 2016, the dividend growth is where the magic has happened. While the dividend payouts have been varied since inception, total growth has been exceptional.

We can see that the dividend has grown over 636% since inception. This blows SCHD and Vanguard Dividend Appreciation Index Fund ETF Shares (VIG) out of the water. Even on a smaller time frame of 5 years, the dividend increased at a CAGR of 17.41%. The strategy of picking high free cash flow yielding companies should in theory support this level of continued dividend growth. While there are certainly macro challenges due to the high interest rates, I anticipate dividend growth to be stronger during ideal market conditions.

Downsides

The starting dividend yield of 1.8% is a bit disappointing. While the fund isn’t trying to be a dividend growth fund exclusively, it would be better to see some more impactful dividend raises in the future. In order to generate a substantial dividend income from shares of COWZ, you need several millions invested in a position to produce a living income. For reference, the average individual income in the US is $63,795 per year. In order to generate this kind of cash flow, you’d need about approximately $3.5M invested to generate the average individual income in the US.

While the dividend growth is strong, SCHD offers a much better starting yield that can compound into a larger snowball a lot quicker. This is due to the higher starting yield of 3.5%, which is nearly double that of COWZ. Therefore, if you want any sort of meaningful dividend income without having to wait for the growth aspect, SCHD is the better fund here.

In addition, if the US plunges into a recession we can see further price suppression of the top industries that COWZ has exposure to, such as Energy, consumer, and healthcare. The tightening of consumer spending can ultimately reduce profitability and limit free cash flow yield growth. While this can certainly impact profitability metrics, at least COWZ gives you the exposure to the companies which would be managing these headwinds most efficiently.

Takeaway

Pacer US Cash Cows ETF has delivered strong results because of the fund’s methodology for selecting quality stocks with growing free cash flow yields. This formula’s proven track record outperforms the SPY and dividend growth focused ETF, SCHD. The portfolio’s holdings get rebalanced quarterly and this frequency helps keep holdings up to date. The largest sector exposure is to energy stocks, which are known for their cash-rich businesses. The downside to COWZ is that the starting dividend yield is relatively weak and doesn’t pack enough punch to deliver sizeable income.

Q1 2024 Earnings Call Transcript")

")

")