")

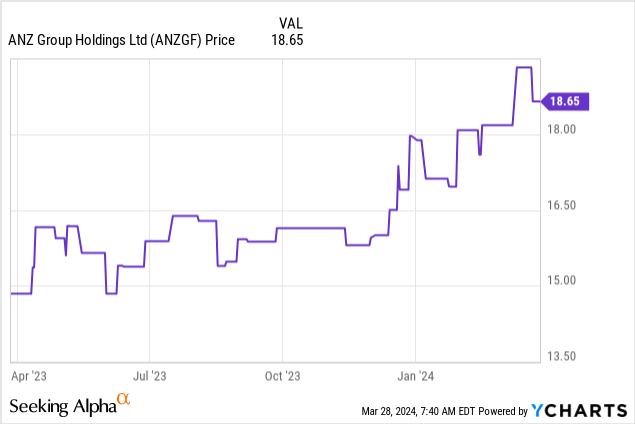

Alongside the rest of its ‘big four’ Australian banking peers, Australia and New Zealand Banking, or the ‘ANZ’ Group (OTCPK:ANZGF), has been on a tear since I last made the case to own it (see ANZ Group: Shelter From The Australian Banking Storm). While some of the upside is certainly well-deserved, growing concerns about an Australian “bank bubble” are perhaps worth considering; after all, a not insignificant portion of this rally has also come from multiple expansion, rather than purely fundamental outperformance.

Yes, monthly banking data has been robust, with ANZ, in particular, outpacing the system and gaining share at the expense of the regionals. The bank’s latest quarterly report was also generally in line, though there was little indication of major upside surprises ahead – certainly nothing to justify a bigger premium from here. Instead, this story could potentially get more complex if a merger with Suncorp goes through; scale is good for a bank, but making this deal work will be challenging, given the steep price and delayed synergy realization timeline.

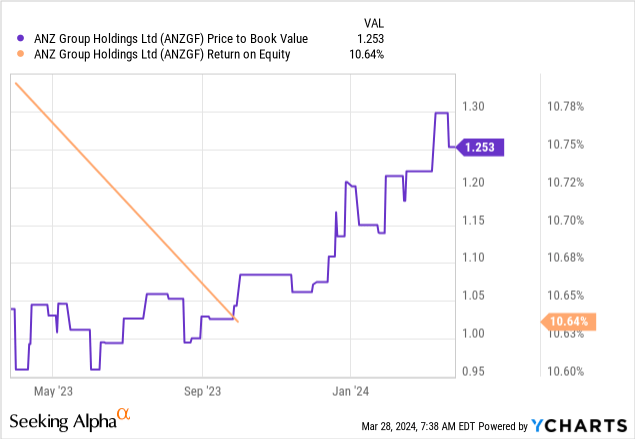

Perhaps the biggest headwind of all, though, is at the macro level; Australia is finally dialing back on its rate hikes and that will pressure net interest margins going forward. In the meantime, the Australian economy will also need to navigate tricky waters, given a backdrop of slower growth and high debt levels – a tricky setup for asset quality. ANZ won’t be entirely immune, even if its institutional focus keeps it under-indexed to the more problematic segments. Plus, the stock is now more expensive at a ~25% premium to book – nowhere near ‘bubble’ territory, but certainly not all that cheap for a stock that has been generating less than 10% returns. All in all, I’m leaning toward neutral on the stock at these levels.

Resilience on Show in Q1

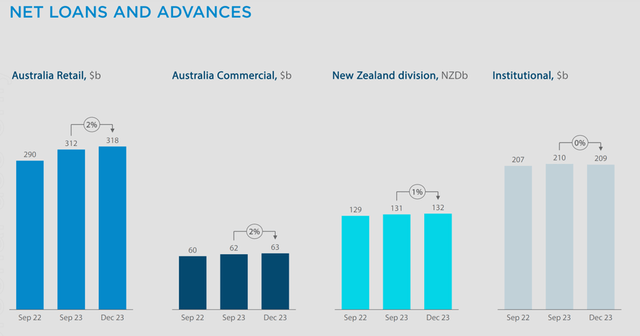

ANZ may have seen a strong rally in its shares recently, but the bank’s Q1 2024 update was relatively benign. To recap, group revenue is pacing ahead of last year’s levels on the markets side (i.e., forex, rates, commodities, etc.), though the retail/commercial banking P&L has been largely status quo (i.e., in line with H1 2023). On another bright note, ANZ only incurred ~$53m of provision charges, reflecting the underlying health of its book – likely a result of its higher institutional exposure (mainly to higher quality businesses and sovereigns). Other balance sheet items were also quite solid; most notably the ~13.1% CET1 ratio (post-dividend), as well as the flattish non-performing asset trend (only ~1bp higher).

ANZ Group

Banking Sector Statistics also Robust

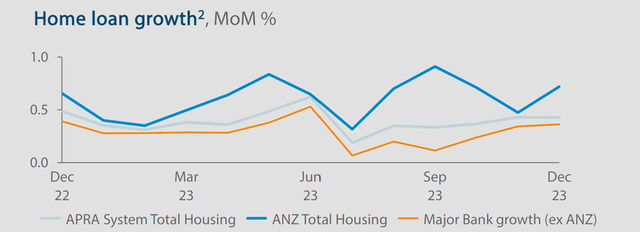

More interesting was monthly data from the Australian financial regulator, the Australian Prudential Regulation Authority (APRA), which increasingly shows a healthier mortgage lending backdrop for the big banks. For a mature market, housing credit growth of over 4% YoY for Australian banks is quite strong, especially considering the steep trajectory of the country’s recent interest rate hikes. Within the sector, ANZ stands out for its relative outgrowth in recent months, particularly in key areas like mortgage lending. Depending on how long the RBA stays ‘higher for longer’ and sector-wide competitive dynamics, ANZ has a path to further improvements in its lending margins from here.

ANZ Group

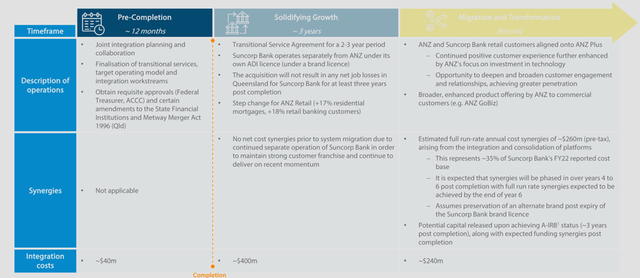

On-Off Suncorp Merger is Back On, Possibly Not a Good Thing

One of the more surprising outcomes this year was the Australia Competition Tribunal’s decision in favor of ANZ’s proposed merger with Suncorp – directly contradicting the Australian competition regulator’s (i.e., the ACCC) initial negative viewpoint. In essence, the Tribunal’s decision rested on its finding that the proposed merger would “not result in a substantial lessening of competition” (again in contrast with the ACCC’s concern that it would “further entrench an oligopoly market structure that is dominated by the four major banks”).

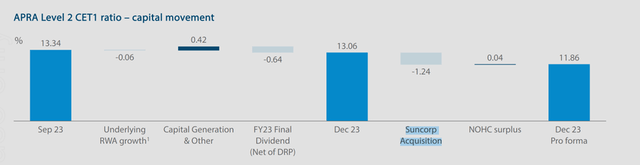

While ANZ’s management will no doubt be buoyed by the news, investors appear less happy, as the negative share price reaction post-announcement showed. The move seems very logical to me. On the one hand, adding scale tends to be a good thing in banking. Yet, the transaction will also come at a ~30% premium to net tangible assets (also a relative premium to other Australian regionals) against ANZ fundraising below book value, which will weigh on the deal economics. And perhaps more importantly, it signals a fundamental shift away from ANZ’s previously outlined returns-focused strategy. In the meantime, ANZ will also need to reserve a fair bit of capital for the merger (note that Q1 2024 CET1 goes from ~13.1% to ~11.9% pro-forma); even after recent non-core stake sales, it leaves a lot less headroom for capital returns (dividends and buybacks).

ANZ Group

Even if the deal gets through, making it work won’t be an easy task – per ANZ management’s guidance, the merger integration costs will be a big hurdle at ~$400m (pre-tax) for the first three years before normalizing lower to ~$240m. The opportunity cost of holding on to excess capital (i.e., foregone earnings) to fund the merger will also be quite significant. Of course, there are quite a bit of synergies as well, most notably on the cost side (~$260m pre-tax), though full realization will only happen after year six based on the bank’s system migration timeline. Other synergies like scale and funding could also be material but are similarly distant. Thus, all signs point to a dilutive outcome in the initial years post-merger, after which strong execution (akin to ANZ’s successful acquisition and integration of the National Bank of New Zealand) will be needed to unlock value.

ANZ Group

Final Thoughts

Australian banks may have endured a tough competitive environment over the last year, but if Q1 results and APRA’s monthly banking numbers are anything to go by, the worst looks to be well and truly behind us now. The issue, though, is that ANZ, together with the rest of the Australian banking sector, has also seen quite a bit of P/Book multiple expansion in recent months. With Australia also on the verge of an interest rate policy shift (which will pressure bank margins) and potentially some repayment challenges as the lagged impact of rate hikes start to bite, the premium multiple doesn’t leave a lot of margin for error. Finally, there’s a complex (and potentially dilutive) merger on the horizon, which adds more risk than reward to the ANZ investment case, in my view. All in all, I still like the long-term ANZ story, but I would much prefer buying it on a pullback.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")