A month ago, I published an article about the EDV ETF, which is a peer fund relative to PIMCO 25+ Year Zero Coupon U.S. Treasury Index ETF (NYSEARCA:ZROZ). Initially, I compared the EDV ETF to the TLT, but I got a request to compare it with the ZROZ. Now it’s time to fulfill that request and compare two major zero coupon treasury ETFs and define a winner.

Even though both funds have some differences, my recommendation on ZROZ is the same as for the EDV ETF: zero coupon treasury bonds, in my opinion, are one of the best ways to fully benefit from rate cuts. There’s a lot of blood in the streets in the bond market these days, and this is exactly the moment when investors should acquire positions in long-duration bonds, in my view. Therefore, I give the ZROZ ETF a Buy rating.

About Zero Coupon Bonds

First things first, a short reference about zero coupon bonds. Zero coupon treasuries are a type of U.S. treasury security that doesn’t pay periodic interest payments or coupons. Instead, they are issued at a significant discount to their face value (par value) and mature at that face value. The investor’s return is the difference between the purchase price of the bond and what they receive when the bond matures.

The variation of the zero coupon treasuries is the treasury STRIPS (Separate Trading of Registered Interest and Principal Securities). STRIPS are regular treasury bonds that have been separated (stripped) into their principal and interest components and sold individually as zero-coupon securities.

The key advantage of zero coupon bonds over ordinary bonds is that zero coupon bonds have a way more pronounced reaction to interest rate changes, as they offer the entire payment only at their maturity. Thus, zero coupon bonds are optimal for hedging and investing purposes when there’s a certain probability that the Federal Reserve may cut rates.

Zero coupon bonds (especially when bought directly) are not an optimal solution for income investors, simply because there aren’t interest payments.

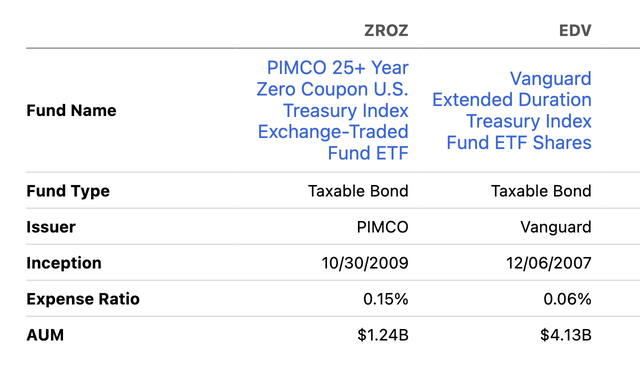

ZROZ ETF Overview And Comparison

According to the description of the Fund, the ZROZ ETF seeks to track the total return of The BofA Merrill Lynch Long Treasury Principal STRIPS Index. Thus, it’s a passively managed fund that tracks a particular index related to STRIPS Treasuries.

The first differentiating factor between the ZROZ and EDV ETFs is the expenses. With an expense ratio of just 0.06%, EDV looks like a much better option compared to the ZROZ ETF’s expense ratio of 0.15%.

Seeking Alpha

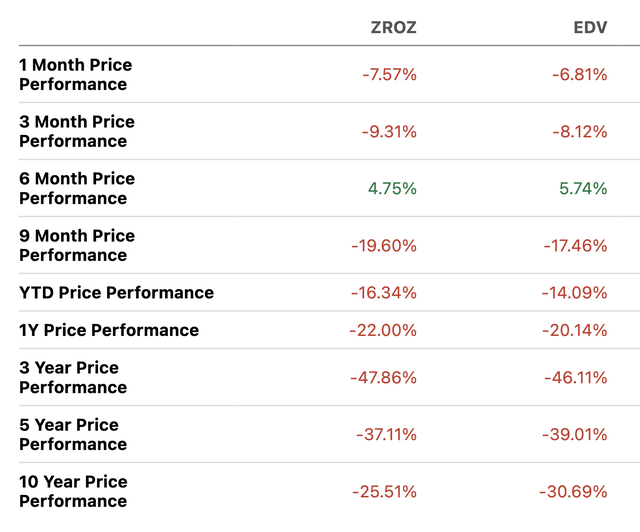

The short-to-mid-term performance of the ZROZ ETF is slightly worse compared to EDV, though the 10-year performance is a bit better.

Seeking Alpha

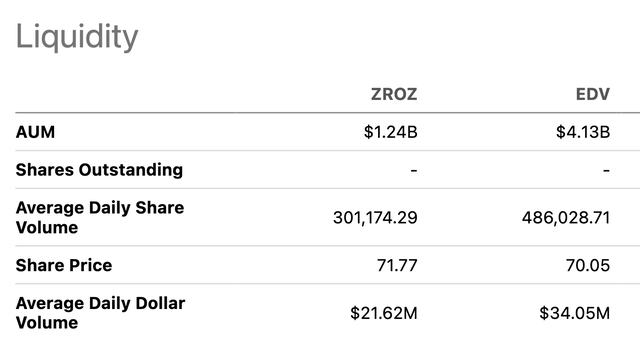

I’d say that the difference in performance between the two ETFs is negligible. When it comes to liquidity, the ZROZ ETF looks inferior to EDV with a smaller AUM and lower daily trading volumes.

Seeking Alpha

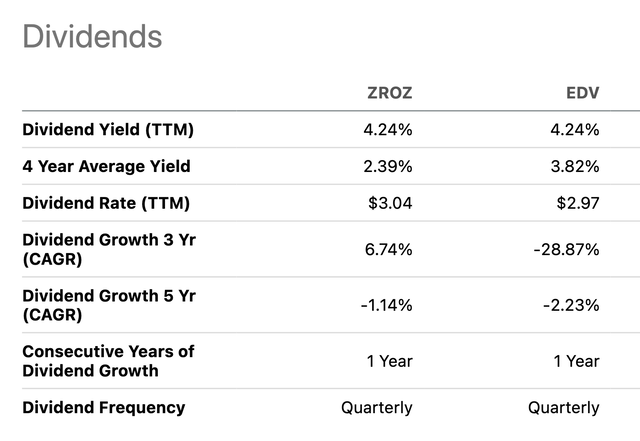

As for dividends, both ZROZ and EDV have a similar TTM dividend yield of 4.24%. The ZROZ ETF has a better track record of 3-year dividend growth, though EDV’s 4-year average yield is higher compared to ZROZ.

Seeking Alpha

In my opinion, it’s a bit disappointing that both funds pay dividends, as it effectively undermines the idea of zero-coupon bonds. As stated in the ZROZ ETF’s prospectus:

Each Fund distributes substantially all of its net investment income to shareholders in the form of dividends. The PIMCO 25+ Year Zero Coupon U.S. Treasury Index Exchange-Traded Fund intends to declare and distribute income dividends quarterly to shareholders of record. In addition, each Fund distributes any net capital gains earned from the sale of portfolio securities to shareholders no less frequently than annually.

Basically, the ZROZ ETF maintains its dividend payments through regular selling of zero coupon bonds from its holdings and distributing the proceeds from such sales. This is not a dealbreaker if you seek exposure in zero coupon bonds through ZROZ or EDV, but still an important factor to consider for both funds.

Be Greedy When Others Are Fearful

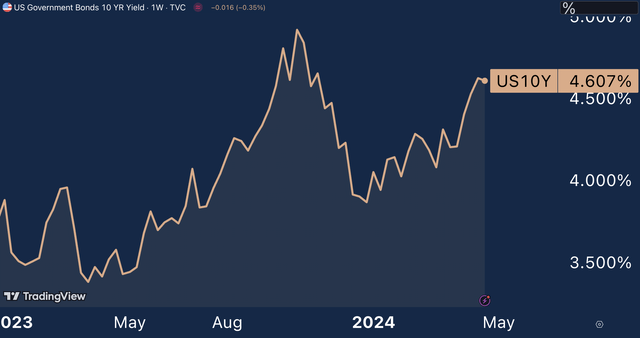

The market environment for bonds isn’t especially favorable these days. The US economy keeps firing on all cylinders, and Fed officials are now discussing the possibility of another rate hike. Against such a news background, long-duration bonds have dipped, and their yields have surged substantially since December 2023. The 10-year US government bonds yield currently stands at 4.6% yield, up from 3.9% in December 2023:

TradingView

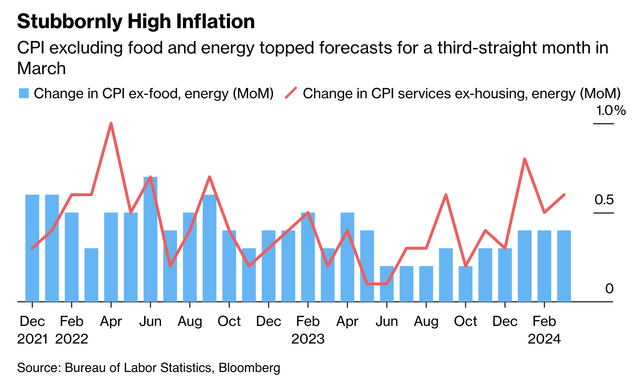

With the US economy seemingly staying surprisingly strong, the main issue for the Federal Reserve that prevents the regulator from cutting rates is high inflation. US consumer prices picked up again in March, and there are no signs that inflation may cool off anytime soon.

Bloomberg

However, in my opinion, the Fed may still cut rates if the US economy is at risk of a recession, which may provide a so-awaited relief for US Treasuries.

In this regard, it seems that the economic resilience of the US economy may turn out to be not so long-lasting. S&P Global reported that its U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, declined to 50.9 in April from 52.1 in March. For reference, a value above 50 indicates expansion in the private sector and a value below 50 means contraction. New orders received by private businesses also dropped to 48.4 from 51.7 in March, a noticeable decline just in one month.

Even though one data point is not enough to make far-reaching conclusions about further economic dynamics in the US, it’s still an important indication that the current interest rate environment in the US is pretty tough to operate in the longer run.

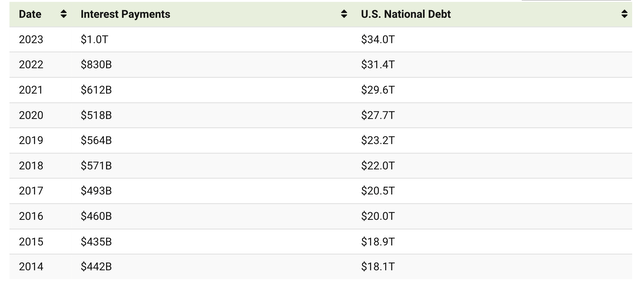

Another important consideration why the Fed may have to cut rates in the near future is skyrocketing interest payments on the rapidly increasing US national debt. The interest payments have hit a new high of $1 trillion in 2023, which is more than such US budget expenses as defense spending or Medicaid.

VisualCapitalist

Without substantial rate cuts in the foreseeable future, maintaining the national debt may become a serious threat to the fiscal stability of the United States, aside from the US’ huge budget deficit.

The key takeaway for investors is that it’s quite likely that in the next 6 to 12 months, interest rates in the US will likely be lower than today, providing an opportunity for investors to benefit from this trend via investing in long-duration zero-coupon bonds.

The Bottom Line

For me, it’s hard to find a reason to prefer ZROZ over EDV when picking between these two ETFs. The EDV ETF has better liquidity, lower expenses, and similar performance, making it a more preferable option overall compared to ZROZ.

Nonetheless, if you already have the ZROZ ETF shares in your portfolio, it’s totally fine to keep them and add up more shares to average the position down. Alternatively, you can just buy EDV and keep both ETFs in your portfolio for some diversification. I made an overview of EDV here, so feel free to learn more about this ETF.

Q1 2024 Earnings Call Transcript")