")

Introduction & Investment Thesis

I initiated a Buy rating on Wix (NASDAQ:WIX) on February 16. My bull thesis was predicated on my belief that the company continues to drive strategic growth in its Partners business by launching Wix Studio, as well as rapidly innovating on its AI product offerings while expanding profitability. Since then, the company has released its Q4 FY23 earnings report, where revenue and earnings exceeded expectations.

In Q4, the company continued to see deeper adoption of Wix Studio as its Partners business grew 38% YoY. Meanwhile, the company continues to innovate with its AI offerings. In Q4, it launched its AI site generator, which is designed to build ready-to-publish websites based on user prompts. At the same time, the management remains laser-focused on improving margins.

Moving forward, I believe that Wix should continue to see growth in the low to mid-teens as it harnesses its growth drivers by attracting higher-intent users on its platform. This, in turn, will result in higher conversion and monetization, which will lead to expanding margins. As a result, I am increasing my price target to $196, which represents an upside of 40% from its current levels, and rating the stock a “buy.”.

About Wix

Wix is a cloud-based web development platform that enables users to create websites and mobile applications without extensive coding skills, utilizing an easy-to-use, drag-and-drop interface and customizable templates.

As of Q4 FY23, Wix derived 73% of its revenue from subscriptions, while the remaining 27% came from Business Solutions, which include e-commerce features and booking systems. The company is focused on driving growth primarily in these two areas: 1) Partners Business, which saw a 38% YoY growth in Q4, with the introduction of Wix Studio; and 2) AI, where Wix is rapidly innovating in building new capabilities to accelerate growth in their Self Creator and Partners business by enabling them to create visual and written content more easily and optimize web designs to drive better business outcomes.

The good: Continuing growth in Partners business, rapid innovation, & growing margins

As per Wix’s Q4 FY23 earnings report, it generated $1.56B in revenue, up 13% YoY. Out of the $1.56B, Creative Subscription revenue contributed 73%, growing 12% YoY, while Business Solutions contributed 27% of the total revenue, growing 20% YoY.

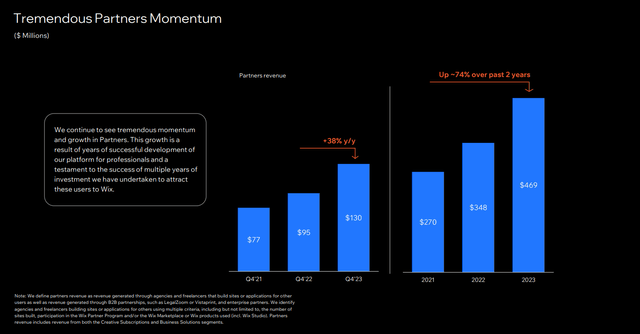

In my previous post, I talked about the promising Partner business, which Wix characterizes as “revenue that is generated through agencies and freelancers that build sites or applications for other users, as well as revenue generated through B2B partnerships, such as LegalZoom or Vistaprint, and enterprise partners.” Being one of the strategic growth drivers for the company that the management has outlined in its Investor Day Presentation, this segment grew 38% YoY to $130M in Q4, as well as 9% sequentially on a QoQ basis.

Q4 FY23 Earnings Slides: Wix’s growing Partner momentum

During the earnings call, the management sounded very optimistic about the progress they are seeing with the adoption of Wix Studio and the capabilities it offers to optimize their partner’s workflow and productivity while improving their own client services. This is what Avishai Abrahami, CEO of Wix, said during the earnings call, which demonstrates the success of Wix Studio and its strategic initiative around Partners business thus far.

“Since August, more than 500,000 agencies and freelancers have created Studio accounts, and we currently have more Studio premium subscriptions than we expected to have at this point. This growth has been driven by the incredible strides we’ve made in building a best-in-class product tailored for the agency and freelancers’ market. And we have no plans of slowing. There are a number of improvements and new exciting tools on the way for partners. We expect Studio and our broader professional product offering to be a meaningful catalyst of growth in the coming years.”

Moving forward, I maintain my thesis that I see Wix Studio driving accelerated growth in Wix’s Partner business as product innovation and enhancement in the Studio will continue to bring new customers, as well as drive deeper monetization and Gross Payment Volume (GPV) from existing customer cohorts on the platform.

Simultaneously, Wix is committed to driving rapid innovation in its AI capabilities by building solutions to help its customers create visual and written content, optimize design, write code, and drive better business outcomes. In my previous post, I talked about Wix’s AI solution offerings, which include the AI Meta Tags Creator, which is built to help generate optimized title tags and meta descriptions, as well as the AI Chat Experience, which is designed to generate recommendations on web templates, commerce applications, and other business needs. In Q4, the company also released its AI site generator, which will create a ready-to-publish website based on user prompts. During the earnings call, Avishai Abrahami mentioned that the majority of their new customers are using at least one AI tool on the platform, and the engagement has been encouraging. In my opinion, the company is moving in the right direction with its focus on AI as a growth driver, as I believe that the innovation pipeline will provide a superior customer experience, leading to deeper customer engagement and adoption. This, in turn, should result in a higher monetization rate, which will help the company unlock operating leverage to continue to expand its profitability. This is what Avishai Abrahami said during the earnings call, which highlights the optimism of the company’s AI efforts so far.

“We expect our AI technology to be a significant driver of growth in 2024 and beyond. We also leveraged AI to improve many of our internal processes at Wix, especially research and development velocity. With these platforms, we are able to develop and release high quality AI-based features and tools efficiently and at scale. We expect AI to continue to be a major competitive advantage for us as we build our product suite and more AI tools to make the web creation experience more frictionless for our users, as well as helping to improve operations.”

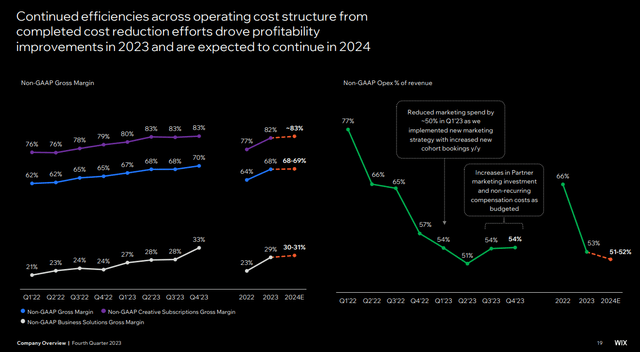

Shifting gears to profitability, Wix generated $240M in non-GAAP operating income in FY23, a significant improvement from a $36M loss in FY22. Non-GAAP Operating Margin expanded from -3% in FY22 to 15% in FY23. The company was able to achieve this by streamlining its operating expenses, particularly in Sales and Marketing, which accounted for 25% of total revenue in FY23, compared to 28% of total revenue in FY22. At the same time, I believe that as the company continues to drive its strategic initiatives to attract high-intent users coupled with product innovation, it will drive higher conversion, monetization, and therefore higher Average Revenue per Subscription (ARPS), which will translate to a better return on investment (ROI) on Sales and marketing spend as well as improved operating leverage.

Q4 FY23 Earnings Slides: Wix’s improving profitability

Looking forward, Wix expects to generate revenue in the range of $1.73-1.76B in FY24, which would represent a growth rate of 11–13%. At the same time, the company has guided for non-GAAP gross margins of 68-69%, with non-GAAP operating expenses of 51-52% of total revenue. This would translate to a non-GAAP Operating income of approximately $315M, representing a growth rate of 31% YoY with a margin of 18%, an improvement of 300 basis points from FY23.

The bad: Price hikes amid an uncertain macroeconomic environment

In my previous post, I had outlined the risks that Wix faces, especially as macroeconomic conditions remain uncertain and competitive threats from Shopify (NYSE:SHOP) and Squarespace (NYSE:SQSP) remain. The longer the interest rates remain high, the harder it gets for small and medium-sized businesses as the cost of borrowing remains at elevated levels. This can constrain their spending capacities, which would be a headwind for Wix’s growth prospects. At the same time, the competitive landscape forces Wix to continue to invest in R&D in order to maintain its competitive edge.

At the same time, the company also implemented a new pricing model that will be applied to all new and existing subscriptions. While the management is confident about its decision based on the success it had with raising prices in the past, I am cautious, as we may see some churn and a resulting decline in Net Retention Rate, especially as macroeconomic conditions remain uncertain.

Tying it together: Wix is a buy

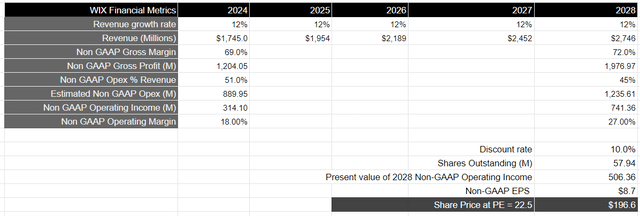

Assuming that Wix grows its revenue by 12% annually over the next 5 years until FY28, it should be able to generate $1.98B in revenue. This will take place as long as the management continues to drive growth in its Partners business while improving customer engagement and monetization by building AI capabilities on its platform.

At the same time, I believe that should Wix continue to drive higher-intent users on its platform, as it continues to drive better business outcomes for them, it should drive a higher conversion rate, which in turn will improve overall profitability for Wix. On Investor Day, the management outlined its long-term financial model for non-GAAP operating expenses to slow to 51–52% in FY24, followed by 47.5% in FY25 and less than 45% after that. Assuming that Wix’s non-GAAP gross margin improves from 68% to 72% during that time period, it should generate a total non-GAAP operating income of $741M by FY28, improving its margin from a projected 18% in FY24 to 27% in FY28. This will translate to a present value of $506M, when discounted by 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings by 8% on average over a 10-year period, with a price-to-earnings multiple of 15–18, I believe that Wix should trade at least 1.5x the multiple, which would result in a price target of $196, or a 40% upside from its current levels.

Author’s Valuation Model

Conclusions

Although there are certain risk factors, such as the uncertainty around the impact of the pricing model given the current state of the macroeconomic and competitive landscape, I believe that Wix is thus far executing on its growth drivers exceptionally well while expanding profitability. As a result, I see further upside of around 40% from its current levels, thus rating the stock a “buy”.

")

Q1 2024 Earnings Call Transcript")

")