")

All of a sudden, the stock market looks shaky again. Rising Middle East tensions and persistent inflation have pummeled interest rate expectations and hence stock valuations, making now a challenging time to bank on unsteady turnaround names.

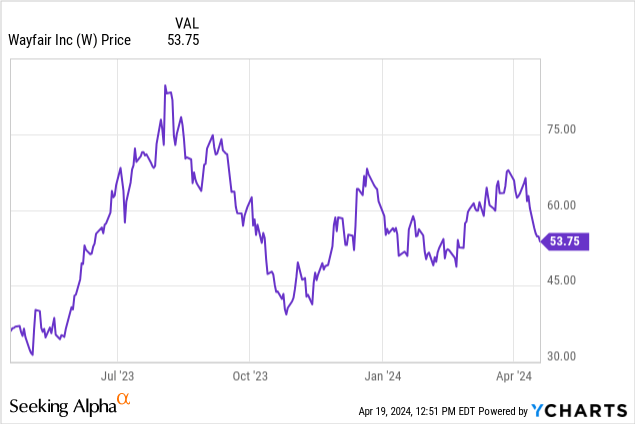

Few e-commerce stocks have been as deeply challenged as Wayfair (NYSE:W), the online furniture retailer that enjoyed a brief spike during the pandemic when people scrambled to move out of cities and furnish new homes, but retrenched just as quickly in the post-pandemic period. Year to date, shares of Wayfair have underperformed the market, falling nearly 10%:

Shakiness over feasibility of adjusted EBITDA targets

I last wrote a bearish note on Wayfair in January, when the stock was trading closer to the high $50s and was just off the back of announcing its third major round of layoffs.

Over the past two years, Wayfair’s ethos has been to get back to its bootstrapped roots and drive efficiency through smaller, more motivated teams. Writing in the year-end shareholder letter, CEO and founder Niraj Shah noted as follows:

We decided to reduce the size of our team in the summer of 2022. Soon thereafter, we discovered we were getting more done, and it was getting done faster and at a lower cost. This led to the realization that we had only scratched the surface of our efficiency gains, and in Jan 2023 we further reduced the size of our team. Yet again we found the same thing – getting more done, and faster, at a lower cost. Unfortunately yet again it became clear that we had not yet gotten back to where we needed to be. And so this time we did things differently – we did a white sheet org model exercise and rebuilt the org from the ground up. This led to a reduction in Jan 2024 but one rooted in our core principles of organizational design. And again, while it is early, it does seem like we are getting more done, and faster, and at a lower cost. It also feels like we have the right level leaders in charge of the right things.”

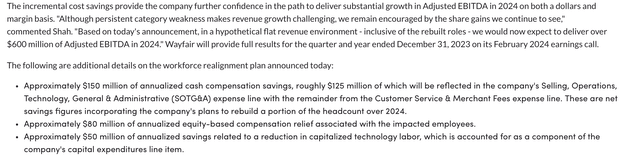

In announcing the latest series of layoffs in January, Wayfair noted that it had a path to generating $600 million in adjusted EBITDA in FY24:

Wayfair FY24 profit expectations (Wayfair layoff press release)

This expectation relied on the twin conditions of layoffs generating $280 million in annualized cost savings, and flat revenue growth.

And yet, in its most recent earnings quarter released in late February, Wayfair acknowledged that while it still appeared to be on track to deliver this expectation, it also put out a cautionary warning that in a softer macro scenario, adjusted EBITDA growth may only be “north of 50%”, which would translate to ~$460 million of adjusted EBITDA, per CFO Kate Gulliver’s remarks on the Q4 earnings call:

It is critically important for us to deliver on our commitment of substantial adjusted EBITDA growth in 2024. We have multiple levers at our disposal to drive adjusted EBITDA independent of the top-line. Even if the macro environment remains challenged across 2024, we have line of sight to full year 2024 adjusted EBITDA growth north of 50% year-over-year.”

In my view, this warning may be the first step in Wayfair retreating from its previously stated target. I remain quite bearish on Wayfair’s prospects for the remainder of the year, given the risk of underperforming expectations.

Revenue declines substantiate the weaker macro story

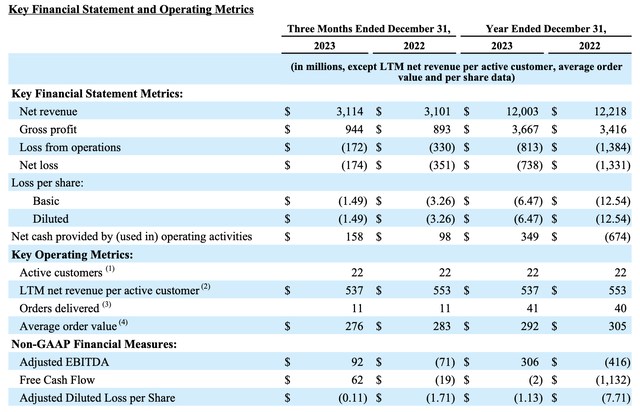

There is more and more evidence to substantiate the risk of a weaker macro pressuring Wayfair’s sales this quarter. In Q4, Wayfair’s revenue growth decelerated:

Wayfair Q4 results (Wayfair Q4 shareholder letter)

Revenue growth of 0.4% slid sharply versus 3.6% y/y growth in Q3. Average order values also continued to decline -2% y/y to $276, as customers opted for more budget-friendly purchases.

It’s also going to get worse before it gets better. CFO Gulliver’s remarks on the Q4 earnings call noted that revenue will decline in the first quarter:

Now let’s turn to guidance for the first quarter. Beginning with the top line, quarter-to-date, we are trending down in the mid-single digits year-over-year and we would expect the full quarter to end in a similar place. We are continuing to win share among consumers but see the weight of a category correction now rivaling the great financial crisis dragging on top line growth.”

The positive offset here is that Wayfair’s gross margins continue to see leverage. Q4 gross profit margins rose to 30.3%, 150bps better than 28.8% in the year-ago Q4; and the company is also expecting Q1 gross margins in the 30-31% range. Margin leverage is another critical path to improved adjusted EBITDA alongside layoffs and opex savings.

Valuation and key takeaways

Despite elevated risks, Wayfair still trades at what I believe to be elevated valuation multiples. At current share prices near $54, Wayfair trades at a market cap of $6.50 billion. After we net off the $1.35 billion of cash and $3.09 billion of debt on Wayfair’s most recent balance sheet, the company’s resulting enterprise value of $8.24 billion.

Even if we optimistically assume that Wayfair can hit its $600 million adjusted EBITDA target for this year, its valuation multiple stands at 13.7x EV/FY24 adjusted EBITDA. In the “low case” scenario in which revenue for the full year is not flat and macro pressures continue to linger, and Wayfair’s adjusted EBITDA grows only 50% y/y, adjusted EBITDA would be $456 million and its multiple would be 18.1x EV/FY24 adjusted EBITDA.

In my view, I’m not keen to pay a double-digit adjusted EBITDA multiple for a low-margin e-commerce company laden with risk. I’m content to stay on the sidelines here.

Q4 2024 Earnings Call Transcript")

")