Q3 2024 Earnings Call Transcript")

")

The spice is flowing.

Investment Thesis

Warner Bros. Discovery, Inc. (NASDAQ:WBD) was created by the 08 April 2022 merger of AT&T Inc.’s (T) WarnerMedia unit and Discovery, Inc.

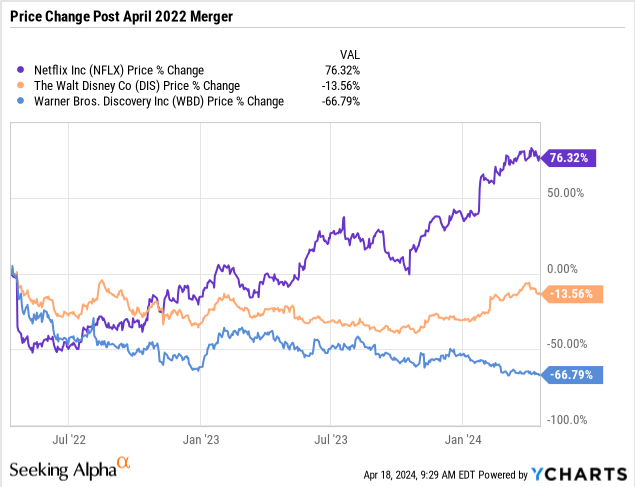

WBD stock price has declined 66% since the merger, underperforming against larger category rivals, and is now trading near all-time lows.

Among the frequently cited negatives for WBD is the large debt load. Even after retiring $12.4 billion of debt since April 2022, WBD still had a gross debt of $44.2 billion at the end of 2023.

Investors who believe management will continue to focus free cash flow on debt reduction, and that the stock will eventually reflect this reduction in risk, may find WBD an attractive opportunity.

Warner Bros. Discovery Overview

WBD ranks #3 in Enterprise Value and #5 in market cap among the 35 companies in Seeking Alpha’s Movies and Entertainment Industry category.

WBD claims the “largest TV and motion picture library in the world,” and to be “the largest producer of content in the world.”

WBD and its even larger (4x by EV, 10x by market cap) rivals in this category, Netflix, Inc. (NFLX) and The Walt Disney Company (DIS), are massive and complex businesses. The entire category is in flux.

I’m only casually interested in the debates around the tension between the creative muse and corporate cash flow, the decline of linear programming, the rise of direct-to-consumer streaming, and the merits of how to best exploit owning the IP for comic book characters.

Seeking Alpha has published more than two dozen articles on WBD so far this year, so I think those debates are pretty well covered.

I am, however, interested in WBD as an investment. I own some WBD stock spun out of T, and I can’t help noticing that the stock is trading near all-time lows when the market is trading near all-time highs.

In particular, I’m interested in WBD’s debt, and how it is being managed. I’m generally not a fan of debt, and WBD certainly has a lot of debt. So, in this article, I’m going to take a look at WBD’s debt situation.

I think it’s important to assess management’s intent and commitment toward debt reduction. To that end, I reviewed three earnings calls, the Q2 2022 call which was a couple of weeks after the merger took effect, the Q4 2022 call which reflected the messy and partial year of the merged WBD, and the most recent Q4 2023 call, which follows the first full year of WBD operation.

As part of their quarterly earnings information, WBD also provides some very nice summaries of debt and operational results, which I’ve also used.

Abbreviations used: DTC is direct-to-consumer, FCF is free cash flow, and EOY is end of year.

A Quick Recap of the Business

WBD operates in three segments, Network, Studios, and DTC. The numbers below are for 2023.

The Network segment is a $21.2 billion revenue business, generating $9.1 billion EBITDA.

Studios generated $12.2 billion in revenue, with $2.2 EBITDA.

DTC is a $10.2 billion revenue business, with $0.1 billion EBITDA.

Corporate costs absorb $1.2 billion of EBITDA, leaving $10.2 billion of EBITDA net for the year.

The network generates 80% of EBITDA, Studios 19%, and DTC 1%.

Key Numbers for 2023

$10.2 billion adjusted EBITDA in 2023, up 11% from $9.2 billion in 2022.

$6.2 billion FCF in 2023, up 88% from $3.3 billion in 2022.

61% EBITDA to FCF conversion in 2023, up from 36% in 2022.

$44.2 billion gross debt at EOY 2023, down 11% from $49.5 billion at EOY 2022

$39.9 billion net debt at 2023 EOY, down 12% from $45.6 billion at EOY 2022.

$5.4 billion debt repaid in 2023, down from $7 billion repaid in 2022.

$2.2 billion interest expense in 2023, down 3% from $2.3 billion interest expense in 2022.

2.44 billion shares outstanding.

2.5-3.0x gross debt / EBITDA confirmed as the long-term leverage target.

WBD does not pay a dividend.

WBD Stock Price Down 66% Since Merger

WBD stock price has declined about 66% since the April 2022 merger and significantly underperformed both NFLX and DIS.

Debt Down 22% Since Merger

The WBD CEO, David Zaslav, opened the Q4 2023 earnings call on 23 February 2024 this way:

We said we would be less than 4 times levered, and we are. We paid down $5.4 billion in debt for the year for a total of more than $12.4 billion since the deal closed. We’re now at 3.9 times [net debt] and expect to continue to de-lever in 2024.

Gross debt is $44.2 billion at EOY 2023, after paying off $12.4 billion. That’s a 22% reduction in seven quarters, a commendable achievement.

In the Discussion section below, we will go into more detail on the cost reduction and cash flow that support this debt reduction.

Leverage Reduced From 5.6x to 4.3x

The “right” amount of debt is always an interesting question. WBD has established a target of 2.5x-3.0x Gross Debt/EBITDA. They often also report the Net Debt/EBITDA ratio, which may be materially lower due to the large amount of cash they usually hold.

Gunnar Wiedenfels, Chief Financial Officer, cautioned in the Q2 2022 call that 2022 was going to be “messy” and “noisy” as the financials were integrated and that Warner Media had come into WBD weaker than expected, but said:

I remain very confident that we are on track to achieve our target gross leverage of 2.5 times to 3 times at the latest 24 months after closing.

That would be April 2024. That’s not going to happen.

By the Q4 2022 earnings call, the CFO had this to say:

We are laser-focused on delevering the balance sheet, where I see net leverage very comfortably inside of 4x by the end of 2023 and reiterate our prior guidance to be within the investment grade range by mid-2024 and within our gross leverage target of 2.5x to 3x by the end of 2024.

Net debt was, in fact, under 4x by EOY 2023, coming in at 3.9x. But it was also clear by that time that the 2.5x-3.0x gross debt target was not going to be achieved in 2024.

Part of the issue is that EBITDA growth has been slower than anticipated. With the $44.2 billion gross debt, meeting the 3.0x leverage target would have required $14.7 billion EBITDA, rather than the $10.2 billion actually delivered.

To get a feel for the sensitivity here, we can compute the gross debt required to meet the 3.0x target at several EBITDA levels, and the additional debt reduction needed to achieve that:

- EBITDA $10 billion, gross debt $30 billion, $14.2 billion reduction.

- EBITDA $12 billion, gross debt $36 billion, $8.2 billion reduction.

- EBITDA $14 billion, gross debt $42 billion, $2.4 billion reduction.

WBD declined to give EBITDA guidance for 2024 in the Q4 2023 earnings call.

Assuming WBD pays down $4 billion per year going forward, and EBITDA increases to $12 billion, the 3.0x gross leverage target should be reached by EOY 2025.

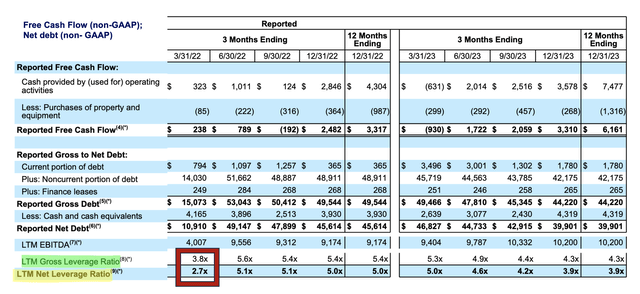

WBD publishes a helpful Trending Schedule with their quarterly results. The portion of the table of immediate interest to us is below, with some highlights. Note that the Q2 2022 is the first quarter to reflect the merger. The red-boxed results (Q1 2022) reflect the last quarter of Discovery results.

WBD Trends – FCF, EBITDA, Debt (WBD data, table edits and annotations by author)

There are a couple of points to note.

In the seven quarters of progression from Q2 2022 to EOY 2023, gross and net debt has declined every quarter, except for Q1 2023, averaging about $1.3 billion per quarter.

Over the 18 months from 30 June 2022 to 31 December 2023, net debt is down 19%, and gross debt is down 17%. LTM EBITDA is noisy and is only up about 7% from Q2 2022. Debt is going down significantly faster than EBITDA is going up.

Overall, gross debt / EBITDA has declined from 5.6x to 4.3x, and net debt/EBITDA from 5.1x to 3.9x.

Evolution and Status of the WBD Debt Stack

WBD provides a clear presentation of the debt issues outstanding.

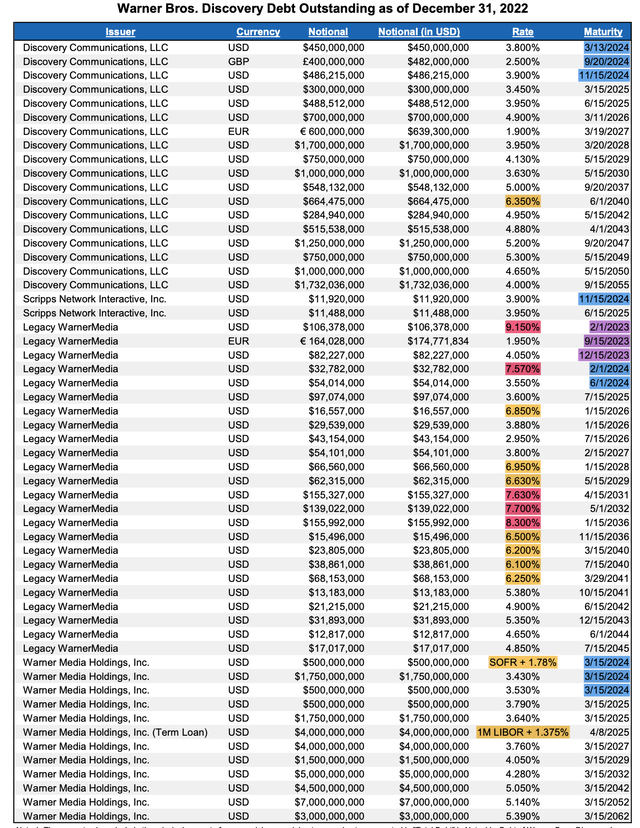

First, we’ll look at how things stood at the end of 2022. Recall that WDB paid down $7 billion of debt in 2022.

Note that the primary sort is by Issuer, then by Maturity data.

In the Maturity column, the three 2023 maturities are highlighted in purple ($0.36 billion), and the nine 2024 maturities in blue ($4.27 billion).

In the Rate column, the issues with rates >6% are highlighted in yellow, those with rates >7% are highlighted in pink. Legacy Warner Media has 12 Rate highlighted issues ($0.9 billion), Warner Media Holdings two issues ($4.5 billion), and Discovery Communications only one issue ($0.7 billion).

The table below shows the situation at EOY 2022.

31 December 2022 WBD Debt Stack (WBD Q4 2022 data, author highlights)

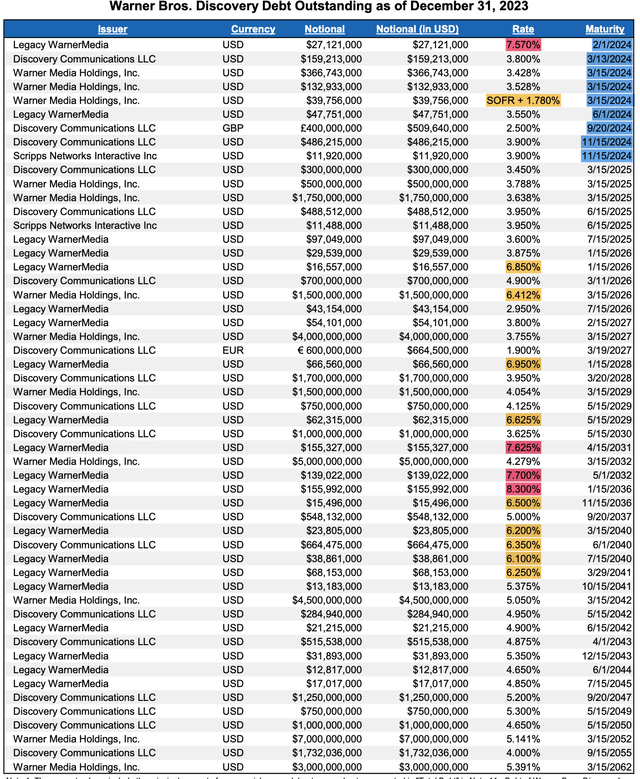

The next table shows how things stood at EOY 2023. WBD paid down $5.4 billion of debt in 2023.

The primary sort is now by Maturity date. The Rate color codes are the same; >6% yellow, >7% pink.

All the 2023 debt is gone. All the 2024 debt maturities are still present (blue), but the amount due in 2024 has been paid down to $1.78 billion.

31 December 2023 WDB Debt Stack (WBD Q4 2023 data, author highlights)

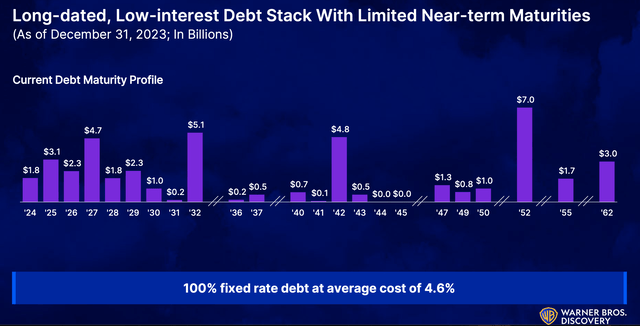

The slide below summarizes the debt by year of maturity at EOY 2023.

And this slide shows the situation at the end of 2023. test (Q4 2023 WDB Earning Release)

That brings us up to date.

Fitch affirmed a BBB- / Stable ratings for WBD on 27 March 2024, and an A- / Stable rating for DIS on 22 January 2024. S&P Global upgraded Netflix to BBB+ in August 2023.

There is yet more to do.

Looking Ahead

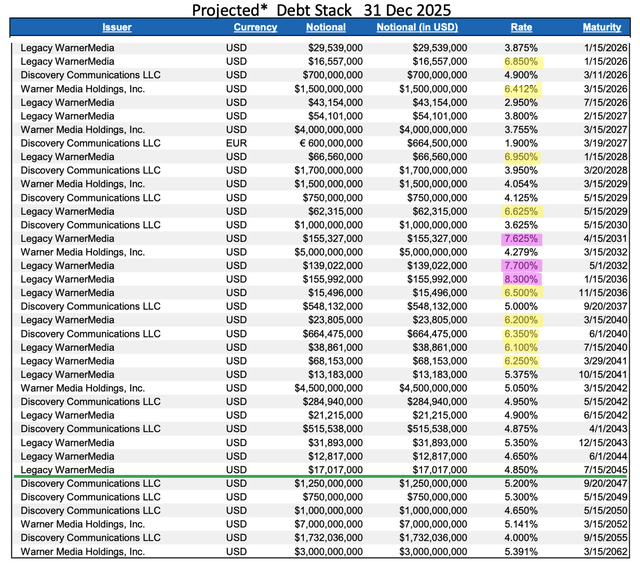

We can now make a hypothetical projection (marked *) of what the debt stack might look like at EOY 2025. We will assume $7.8 billion of FCF (~ 72% of the 2023 FCF allocation to debt payoff) is used to pay the debt in 2024 and 2025:

- all the 2024 debt is paid off ($1.8 billion).

- all the 2025 debt is paid off ($3.1 billion).

- all the debt remaining with Rate > 7% is paid off ($0.45 billion).

- all the debt remaining with Rate > 6% is paid off ($2.45 billion).

That leaves us with the 31 December 2025 Projected Debt Stack table below. The 12 highlighted debt lines would be fully paid off, but have been retained in the table to show where those payoffs would fall on the maturity schedule. A few points to note:

- gross debt would now be $44.2 billion – $7.8 billion = $36.4 billion.

- remaining 2026 debt would be only $0.78 billion.

- 2027 debt is still $4.7 billion.

- the $14.7 billion in debt below the green line is very long-term, with a maturity more than 20 years away and a maximum Rate of 5.4%.

Projected WBD Debt Stack 31 Dec 2025 (WDB data, edited and annotated by author)

One might argue that rather than pay off higher rate debt, it would be better to focus on paying off nearer-term debt. I’ll leave that to the CFO to determine, but I think this illustrates what’s possible.

Where does that leave us?

Our projection above results in $36.4 billion of gross debt. To make the 2.5x-3.0x gross debt / EBITDA goal, that would require $12.1 billion in EBITDA. That seems feasible.

It appears that with two or perhaps three years of $4 billion a year debt pay down, WDB will reach their 2.5x-3.0x leverage target, and have essentially mitigated the debt risk. It would leave them with a still significant $32-$36 billion in gross debt, but with 40% of this very long-term debt, none of it with interest rates above 5.4%.

Furthermore, it’s not impossible that inflation might be running at a rate that would leave WBD in no hurry to pay off that long-dated debt before maturity.

Discussion

1. WBD Management is Focused on Cash Flow

I believe WBD management has demonstrated and will maintain the emphasis on free cash flow that they brought from Discovery. The message has been strong and consistent from day one.

In the Q2 2022 earnings call, the first WBD call, a few weeks after the merger, CEO David Zaslav identified “durable and sustainable free cash flow generation” as one of the four key ingredients for WBD’s success.

Cash flow was not a priority for Warner Media before the merger. From the Q2 2022 earnings call, the WBD CFO Gunnar Wiedenfels said:

But if I take a step back here and just look at, call it, the past 15 months for Warner Media sort of as a carve out-group, we’re looking at more than $40 billion of revenue and really virtually no free cash flow.

The contrast with Discovery is fairly stark. The CEO commented in the same earnings call:

I’ve been at Discovery now for 15 years, and for those of you that have followed us, we’re focused. Discovery was a free cash flow machine. We were generating over $3 billion in free cash flow for a long time with investing in our new media, which we did successfully, and we learned a lot. We still were generating almost $2.5 billion of free cash flow.

In the Q4 2022 earnings call, the CFO enumerated his major goals, including rigorous evaluation of capital allocation opportunities and improved cash flow, noting the goal to:

drive overall efficiency and free cash flow conversion towards our near-term goal of 1/3 to 1/2 conversion of adjusted EBITDA with longer-term upside towards our 60% goal.

The CEO commented on that call:

This is one team now. Everybody has a strategic focus on improving free cash flow, and market share for each of the businesses.

We want to run this company to drive free cash flow and the ability to monetize a lot of the content that isn’t critical to subscriber growth … or helpful to [reducing] churn.

2. Free Cash Flow Funds Debt Reduction

The management at WBD promised they would use the FCF to pay down the debt, and they have. WBD paid down $12.4 billion of debt since the April 2022 merger, and finished 2023 with Gross Debt / EBITDA of 4.3x, well down from the 5.6x number reported for Q2 2022, the first post merger quarter, and well on their way to their goal of 2.5x-3.0x.

From the Q4 2023 call, the CFO said:

We remain committed to our long-term gross leverage target of 2.5 times to 3 times, and while we do not expect to hit that target by the end of this year [2024], we do expect to continue de-levering in 2024 as we stay focused on debt repayment with our free cash flows and any proceeds from non-core asset sales.

The CEO added, in response to a question about guidance and capital allocation:

You’ll see us driving free cash flow this year. You’ll see us delevering the balance sheet.

We do have the optionality of looking at other assets, but it’s going to be a very high bar for us.

3. Cost Savings Significantly Improve Free Cash Flow

WBD initially set a $3 billion dollar annual cost reduction goal and achieved $4 billion by EOY 2023.

In the Q4 2022 earning call, CFO Gunnar Wiedenfels reported:

Through the end of 2022, we’ve already realized over $1 billion of synergy, … are now confident in a path to at least $4 billion of savings largely addressable through 2024, … and are working on a total potential opportunity of $5 billion over the next few years.

In the Q4 2023 call:

First, our post-merger integration is substantively complete as of the end of 2023. We have now achieved total combined merger and transformation savings of $4 billion. There are substantial improvement opportunities left for us to capture, … and we expect to see this reflected in our near and long-term free cash flow generation.

Some of this is just the reduction of duplicate expenses one would expect in any merger, but a lot of it looks like bringing better management to the Warner Media assets and business processes. The magnitude of these savings speaks to how significant these management improvements have been.

This is a $4 billion annual contribution to FCF, with potentially another billion to come. Recall that WBD reported $6.2 billion FCF in 2023.

These cost savings roughly appear to provide over half the FCF for 2023.

4. Looking Forward

It appears reasonable to expect FCF to run $5 billion or more a year over the next three years, and for $4 billion or more per year of the to be used for debt reduction.

That would give a gross debt at EOY 2026 of about $32 billion, of which ~46% is 20+ years out. With 2026 EBITDA of $12 billion, leverage would be 2.7x.

Another three years of the same level of effort, and gross debt would be $20 billion, and leverage 1.7x. WBD might be approaching “fortress balance sheet” territory at that point.

5. Stock Buybacks Are Now Feasible and Attractive

WBD’s aggressive debt reduction and significant stock price decline has created an unusual situation where they have the option to make material stock buybacks and also continue deleveraging.

Two billion dollars would buy back ~10% of the stock at current prices. There should be sufficient FCF in 2024 to do that and pay the $1.8 billion in debt maturing in 2024.

As much as I support debt reduction, this is an attractive, perhaps even compelling, opportunity. There are probably a few other options that provide a guaranteed and permanent 10% increase in EBITDA/share, with zero execution risk. Their own stock might be the unusual “other asset” that meets the high bar mentioned above.

WBD Stock Valuation

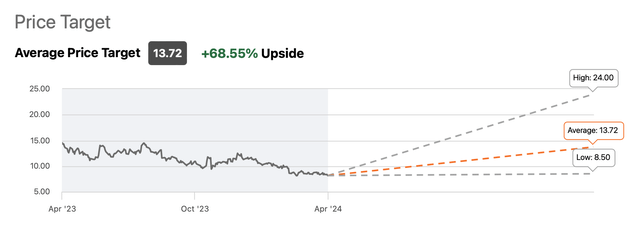

Wall Street (29 analysts) has a 12-month price target for WBD of about $14, but the range is pretty wide, $8.50-$24.

Wall Street Price Target (Seeking Alpha)

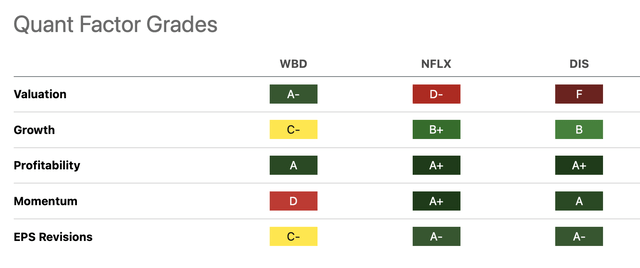

The “peers” aren’t really very directly comparable, and WBD has an arguably very brief at best track record as the WDB that will exist in a few years. Seeking Alpha’s Quant Factor analysis also suggested that WBD is cheap, and peers are expensive.

Seeking Alpha Quant Grades (Seeking Alpha)

By EOY 2026, I would expect another $12 billion in debt reduction and an EBITDA of $12 billion or better. All in all, I think the WBD of 2026 will be worth 2-3x the current price, i.e. ~ $17-$26. We shall see.

Risks to Investment Thesis

The primary risk to this investment thesis is that a faster or deeper decline in the network segment could reduce EBITDA and FCF, hindering both debt reduction and the long-term financial performance of the company.

The Network segment provided 80% of 2023 EBITDA. Large improvements in the Studio and DTC segments would be required to counter-balance a material decline in the Network.

One strategy to mitigate this risk is to be aggressive in paying down debt in the next few years, even beyond the current 2.5x-3.0x goal.

Investor Takeaway

WBD stock is trading today near all-time lows, down 66% from the price at the April 2022 merger. FCF is large enough to materially pay down debt, and management has done that, with debt down $12.4 billion since the merger.

Over $4 billion in annual cost savings from increased post merger efficiencies of the combined companies, and better management of the Warner Media business and assets, provide a large part of this FCF.

It’s a subjective assessment, but I believe management is strongly committed to reaching their long-standing goal of 2.5x-3.0x gross debt/EBITDA. With modest EBITDA growth, this goal may be achieved by EOY 2025 and is highly likely by EOY 2026.

In the near term, I expect WBD to pay off at least another $725 million of debt in Q1 2024, and $1.8 billion for the year. Opportunistic stock repurchase in 2024 is possible, but probably unlikely before the leverage goal is achieved.

I expect the Warner Bros. Discovery, Inc. stock price to eventually reflect the risk reduction created by the debt pay down and would look for a $17-26 target by EOY 2026. I would rate WBD stock a Buy near the current price.

Personally, I own a nearly full position in WBD. After doing the research for this article, I entered an $8.01 limit order to double that holding.