Q1 2024 Earnings Call Transcript")

")

The recent expectations for a quick pivot of the Fed’s interest rate policy somewhat cooled down, which reminded me of the attractiveness of floaters. Since my previous coverage on Invesco Variable Rate Investment Grade ETF (NASDAQ:NASDAQ:VRIG), the fund has gained 8.8% on a total return basis, surpassing my expectations by 3.5%. Despite the Fed’s interest rate reversal suggestions in the second half of the year, I believe that the fund could generate a moderate return of at least 5% over the next 12 months. Hence, my Hold rating on VRIG is still relevent.

Fund overview

VRIG gives investors the opportunity to gain exposure to floating-rate bonds with an investment-grade credit rating. The fund’s primary objective is to generate current income while maintaining a low portfolio duration.

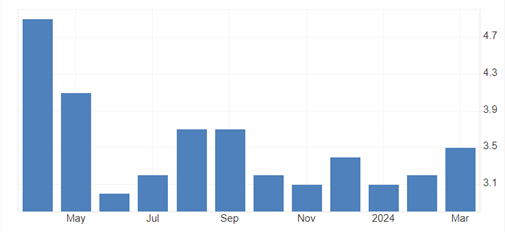

Recently, the market has revised its expectations for the Fed’s interest rate trajectory due to the inflation data.

U.S. inflation rate (tradingeconomics)

The annual rate of inflation picked up since the beginning of the year to 3.5% in March, which undermined the confidence of achieving the 2% target level in the near term significantly. As a result, the rate cut scenario is no longer seen to take place in the first half of the year.

Currently, the prevailing scenario for interest policy actions is for no more than one rate cut in the second half of the year to a range of 5-5.25%. This scenario looks quite compelling for the VRIG prospects, as the fund is linked to current dollar interest rates, which are at levels unseen in the last 15 years.

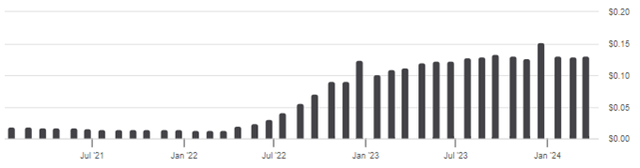

The average coupon to the fund’s portfolio reached 6.2%, which is a consequence of the persistent increase in the coupon rate, which is periodically adjusted to reference rates. This brought a significant increase in dividend payments, as evidenced by the following chart.

Dividend history (Seeking Alpha)

Meanwhile, the effective duration was just 0.09 years, as the prices of the portfolio securities practically did not deviate from their nominal value, which gave investors the opportunity to avoid negative revaluation during the rising interest rate period.

Investment opportunity

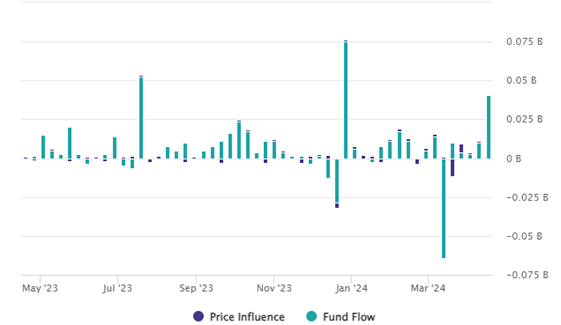

Looking at the following chart, it appears that the scenario of elevated interest rates for a longer period is shared by investors as well.

Fund flows (etfdb)

VRIG recorded a $350 million net inflow for the last 12 months, with the last noticeable outflow of $64 million just a week before the Fed’s March meeting. Hence, the outflow was compensated, as the fund is currently an attractive alternative to the money market yield. VRIG earns a 6.20% coupon rate from its bond portfolio, which has increased prominently compared to 5.68% since my previous article. And going forward, market expectations are pricing a 50-bps cut and suggest that the Fed rate could be in the 4.75–5% range in one year.

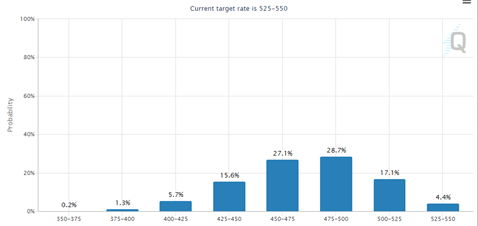

Target rate probabilities for April 2025 Fed Meeting (CME)

As a result, I believe that in the current market conditions, the Invesco Variable Rate Investment Grade ETF could still be an interesting case for investors, as the fund not only generates a stable and attractive level of income but also provides protection from market volatility. For reference, the market’s early optimistic expectations regarding the timing and scale of interest rate cuts were costly for fixed-rate bond investors. The iShares Core U.S. Aggregate Bond ETF (AGG), which tracks investment grade US bonds, has brought a 4% loss for its holders since the beginning of the year, while VRIG recorded a moderate 1.30% positive return.

Now, let’s highlight some figures in order to assess the funds future potential. The current weighted average coupon on the portfolio is 6.20%, the fund distribution rate stands at 6.22%, and the management fee is 0.30%. Given the 50-bps potential interest rate cut that we mentioned, I believe that it’s reasonable to expect at least a 5% return over the next 12 months.

Conclusion

VRIG’s exposure to variable coupon bonds benefited its holders with moderate income levels in this elevated interest rate environment. The fund portfolio of investment-grade bonds can be considered a kind of safety net, given its protection from market volatility. I am keeping a Hold rating on VRIG due to its potential to deliver at least a 5% return to investors. Obviously, during the period of rate cuts, the relevance of flatters is less obvious. However, the forecasts do not imply a quick return to low interest rate levels, which means the coupon rates for the fund’s portfolio could remain in elevated territory at least for the next 12 months. Still, it cannot be ruled out that, in the event of a sharp indication of recession, monetary policy easing may be more pronounced. But on the horizon of one year, I wouldn’t say that the average coupon rates on the fund’s securities will decrease more than 100 bps.

")