| Seeking Alpha")

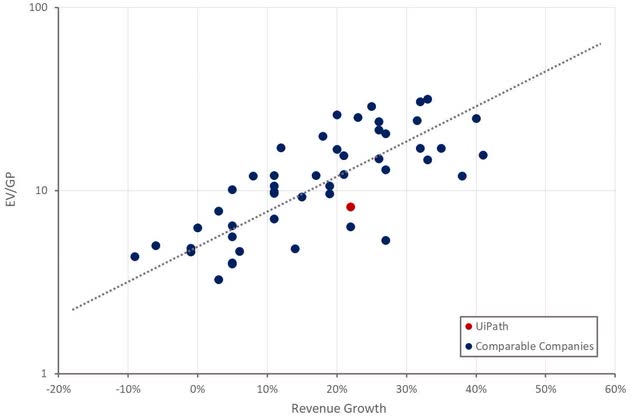

I have alternated between thinking generative AI is a tailwind for UiPath (NYSE:PATH) and suspecting that it will ultimately end up disrupting the company. The company’s financial performance remains impressive though, with strong growth at scale and a recent transition to profitability. The market appears skeptical, as UiPath’s valuation is quite low relative to peers. Some of this is likely due to the fact that UiPath’s cloud business is still building. UiPath may also be suffering from competition concerns due to the complimentary nature of RPA with Microsoft’s business. Despite this, UiPath has a dominant position in the RPA market and could be an attractive long if the share price drops into the mid-teens.

The last time I wrote about UiPath, I suggested that it was a leader in an unloved segment and deserving of a higher valuation given its dominance. I questioned the company’s sales efficiency though and suggested that Robotic Process Automation was too close to the strategic interests of Microsoft (MSFT) for my liking. UiPath’s stock is down roughly 13% since then, and my view of the company hasn’t really changed.

Market Conditions

UiPath believes its TAM is around 60 billion USD, meaning the company still potentially has a long growth runway. It is not clear that RPA will fulfill this potential though, as it is something of a stop gap solution that risks being replaced by more integrated solutions over time. UiPath is defending itself against this possibility by expanding the capabilities of its platform. Rapidly evolving AI capabilities also make it difficult to predict how the market will evolve.

In the near-term, customers want to deploy AI, which is driving spend. Accenture (ACN) had over 600 million USD of new generative AI bookings in its most recent quarter. The company’s clients are prioritizing large-scale transformations and projects that can drive near-term ROI. Accenture is still seeing delays in decision-making and reduced spending though, which it has attributed to macro uncertainty.

There is little evidence of generative AI spend spilling over into RPA so far, which is somewhat surprising. While customers recognize the importance of AI, many organizations lack the technology infrastructure to successfully implement AI across the entire enterprise. This could place RPA down list the list of priorities.

In general, the demand environment still appears to be soft, even if it has stabilized in recent quarters. While some software companies saw strength towards the end of 2023, this could just have been related to expectations of an imminent rate cut. With rates now anticipated to stay for longer, there is a real risk of growth disappointing in coming quarters.

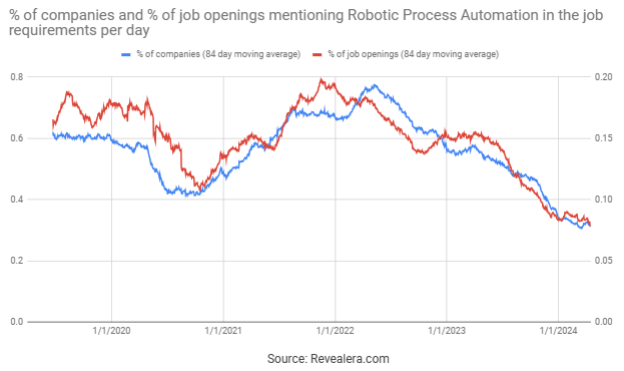

Figure 1: Job Openings Mentioning Robotic Process Automation in the Job Requirements (source: Revealera.com)

UiPath Business Updates

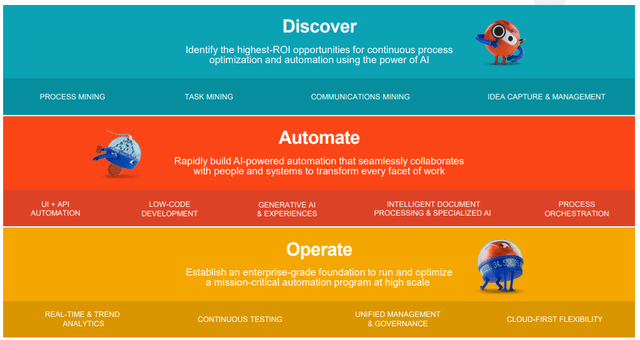

UiPath operates an automation platform that has gradually expanded from RPA to business automation more generally, encompassing areas like process mining and testing.

Figure 2: UiPath’s Platform (source: UiPath)

Advances in AI are increasing the capabilities of RPA and UiPath is leveraging this in areas like:

- Document understanding

- Application and automation testing

- Autopilot

Document Understanding

Document understanding is a core part of UiPath’s platform, and it is being aided by LLMs. For example, 65 of UiPath’s top 100 deals included intelligent document processing in Q4. Intelligent Document Processing leverages AI to enable anyone to train AI models to understand documents. UiPath is also introducing its own LLMs, which leverage open-source LLMs and UiPath’s AI and proprietary knowledge of business documents, potentially strengthening the company’s IDP solution. It is not really clear that UiPath can add significant value in areas like LLMs and vector search, but this type of a technology is a force multiplier for the company’s platform.

Information retrieval using generative AI is a focus area for many companies at the moment. For example, companies like Elastic (ESTC) and C3.ai (AI) are offering technology for generative AI search. Companies like Microsoft are also building information retrieval into their existing products. Information retrieval probably needs to be tied into a larger workflow in order for vendors to capture value though. Competition is also likely to be based on the ability to provide accurate results and ensure data security.

Application and Automation Testing

Testing is another use case seeing early adoption of generative AI. UiPath will likely face a variety of competitors though, both from software vendors and from internally developed customer tools. For example, PubMatic (PUBM) is using generative AI to automate a lot of its software testing process, increasing the ratio of engineers to testing personnel.

UiPath’s Test Suite was initially targeted at automation testing but potentially also addresses the application testing market. The product should appeal to customers, even in the current environment, given that UiPath estimates a six-month payback period. Test Suite customers increased in excess of 75% YoY in Q4.

Autopilot

Autopilot provides guidance and allows users to work with a natural language interface, lowering the barrier to building automations and increasing employee productivity.

Autopilot for Studio allows developers to create automations and apps faster, while Autopilot for Test enables testers to generate tests rapidly and automate testing. Autopilot for Studio and Autopilot for Test are in public preview. Early interest in the product is strong, with Autopilot for Studio having the largest number of preview participants in UiPath’s history. Autopilot for process mining and Autopilot for communications mining are in private preview.

Most software companies appear to be adding some sort of autopilot feature, raising questions about whether it will be considered a differentiator by customers.

Competition

Competition is potentially a consideration holding back UiPath’s valuation. In particular, Microsoft has an RPA solution which could benefit significantly from the company’s distribution.

The two companies aren’t really in direct competition at the moment though. UiPath is focused on complex, multi-application automations that are deployed at scale across the enterprise. Microsoft’s solution is more focused on personal productivity, particularly within its own applications and ecosystem. Power Platform is generating over 2 billion USD revenue annually, but this is likely weighted towards business intelligence.

UiPath is Microsoft’s preferred enterprise automation vendor and UiPath is reportedly deepening its partnership with Microsoft, which aims to bring best-in-class automation capabilities to Azure.

Financial Analysis

UiPath’s ARR increased 22% YoY in Q4 to 1.46 billion USD and revenue was up 31% to 405 million USD. Cloud ARR increased 70% YoY to 650 million USD. Revenue benefitted from enterprise customer demand and licensing. UiPath’s second half is seasonally stronger due to its renewal portfolio being weighted towards the fourth quarter, contributing to recent strength. UiPath has suggested that given fluctuations in its revenue growth rate from quarter to quarter, ARR growth is a better indicator of performance.

First quarter revenue is expected to be 330-335 million USD, an increase of roughly 15% YoY at the midpoint. UiPath has a history of extremely conservative guidance though and will likely beat by something like 15 million USD. ARR is expected to be around 1.5 billion USD at the end of the first quarter, increasing approximately 21% YoY. For the full year, UiPath expects roughly 19% revenue growth and 18% ARR growth.

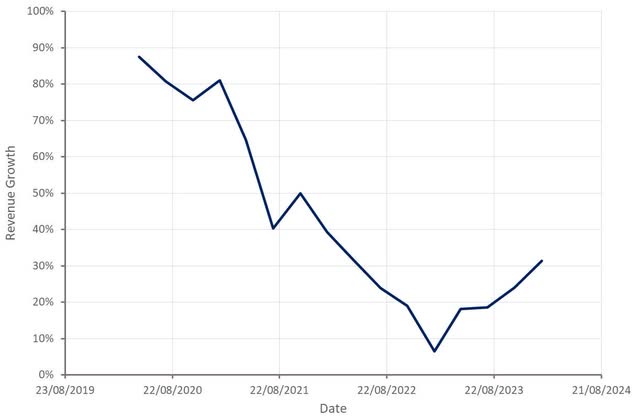

Figure 3: UiPath Revenue Growth (source: Created by author using data from UiPath)

UiPath believes its competitive advantage is larger amongst larger organizations and is targeting its sales efforts towards this segment. As such, the company should be seeing low churn, strong expansion and growth in larger customers. This is broadly the case at the moment:

- Dollar-based gross retention – 98%

- Dollar-based net retention rate – 119%

- Number of customers with more than 5 million USD ARR increased 50% YoY in Q4

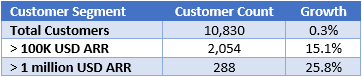

- Customers with ARR of more than 100,000 USD accounted for approximately 86% of total revenue in Q4

Table 1: UiPath Customers (source: Created by author using data from UiPath)

UiPath is seeing churn amongst smaller customers and has struggled to increase its total customer base in recent quarters. This isn’t necessarily a problem given the company’s strategy, but it probably isn’t looked upon favorably by investors.

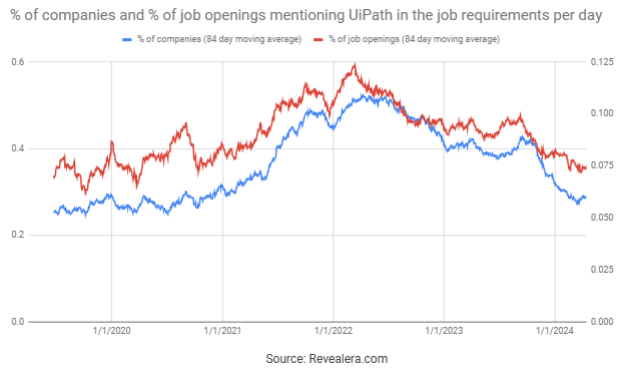

Figure 4: Job Openings Mentioning UiPath in the Job Requirements (source: Revealera.com)

The number of UiPath job openings also remains relatively muted, which is suggestive of steady growth rather than a large acceleration.

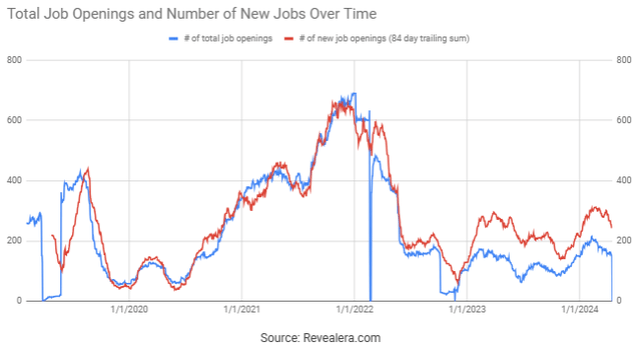

Figure 5: UiPath Job Openings (source: Revealera.com)

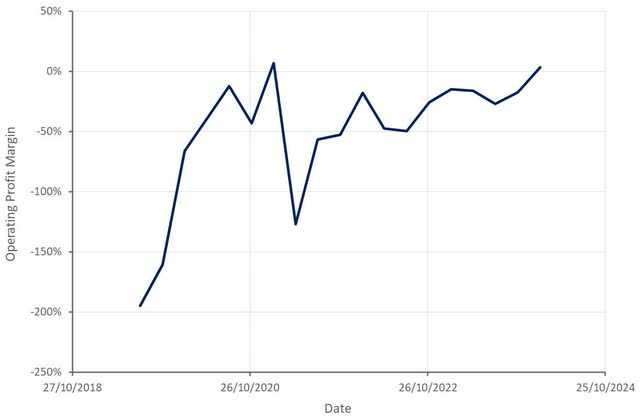

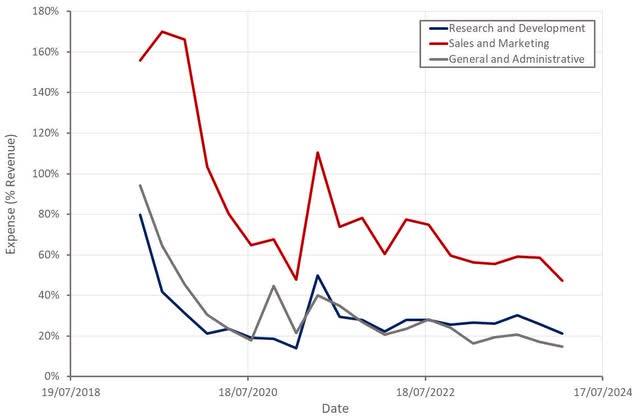

One of my primary concerns with UiPath has been its high operating expenses and lack of profitability. The company’s margins are steadily improving, driven by greater sales and marketing efficiency. UiPath’s high gross retention rate should eventually lead to solid margins, provided that the company’s competitive position remains consistent.

UiPath plans to continue investing in sales and marketing though, taking an industry verticalization approach, which could weigh on margins in the near-term. R&D investments are relatively low given the nature of the platform and rapidly evolving technological capabilities.

Figure 6: UiPath Operating Profit Margin (source: Created by author using data from UiPath) Figure 7: UiPath Operating Expenses (source: Created by author using data from UiPath)

Conclusion

It is easy to make the argument that UiPath’s valuation should be higher, given the company’s high gross profit margins and solid growth. ARR growth continues to soften though. UiPath’s net customer growth is also weak, particularly given how much the company is spending on sales and marketing. The long-term viability of the business is also unclear given proximity to Microsoft’s core business and rapidly changing AI capabilities.

UiPath is already growing steadily, generating positive free cash flow and approaching consistent GAAP profitability. UiPath also repurchased 2.6 million shares at an average price of 19.21 USD in the fourth quarter, and another 938,000 shares at an average price of 23.46 USD between January 31st and March 12th, 2024. Share repurchases are supported by UiPath’s strong balance sheet (1.9 billion USD in cash, cash equivalents, and marketable securities and no debt) and positive cash flows. None of this has stopped the stock from falling significantly over the past 2 months though. Even if investors believe that UiPath is undervalued, it is unclear what catalyst would cause the stock to rerate higher.

Figure 8: UiPath EV/S Multiple (source: Created by author using data from Seeking Alpha)

Q1 2024 Earnings Call Transcript")

")