")

")

Shares of pet insurer Trupanion, Inc. (NASDAQ:TRUP) have moved higher after they slid 17% in the trading session subsequent to its Q1’24 report as a technical bounce and short squeeze took hold. Unable to achieve GAAP profitability since going public in 2014, the company’s founder and CEO is stepping aside and handing the reigns over to the current president in August 2024. The founder’s recent insider purchase despite the fact that Trupanion’s FY24 top line is projected to grow below 20% for the first time in its publicly traded history merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview:

Trupanion, Inc. is a Seattle based pure play pet medical insurance provider with operations in the U.S., Canada, Europe, Puerto Rico, and Australia. With over one million pets on subscription plans as of March 31, 2024, the firm is the largest insurer of pets in North America. Trupanion was formed in 2000 and went public in 2014, raising net proceeds of $72.8 million at $10 per share. The stock currently trades around $26.50 a share, translating to an approximate market cap of $1.15 billion. The stock is down some 12% today.

November Company Presentation

Operating Segments

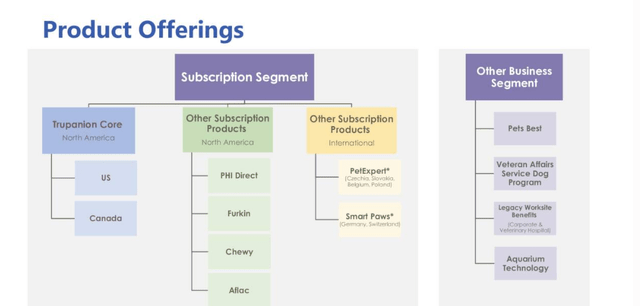

The company views its performance through the lens of two operating segments: Subscription business, and Other business.

Subscription business consists of Trupanion’s direct-to-consumer offerings, with revenue generated from monthly premiums. Although priced for the pet’s unique characteristics, the offerings typically consist of 90% payouts after a $200 deductible and no cap on the payout. Vets like the firm’s products as they receive payment when the pet owner checks out their offices. The segment generated an operating loss of $36.0 million on revenue of $712.9 million in FY23, which represented a slight improvement on an operating loss of $39.8 million on revenue of $596.6 million in FY22.

Other business is essentially B2B pet insurance, including employer sponsored programs, as well as underwriting policies on behalf of third parties. It also houses insurance software solutions sales. It was responsible for an operating loss of $4.4 million on revenue of $395.7 million, versus an operating loss of $3.0 million on revenue of $308.6 million in FY22.

Marketplace and Approach

Stepping back a bit, during its two plus decades of existence, Trupanion has seen the pet insurance market surge, with premiums expanding at a CAGR of 24% from $770 million in 2015 to $3.51 billion in 2022. This growth hasn’t really been fueled by a rise in household dogs and cats in North America, although that figure has increased from 200.4 million just prior to the pandemic to ~210 million today. It is more a function of Millennials having fewer children and treating their pets as such. That said, only 3% of pets in North America are covered by insurance products – a small percentage relative to some European countries, most notably Sweden (67%) and the UK (25%). With 120 million annual visits to the vet in the U.S. and Canada, that under-penetration represents a significant opportunity for insurers like Trupanion.

To further infiltrate the direct-to-consumer market, the firm enlists independent contractors (known as ‘territory partners’) to raise awareness among veterinarians about its offerings. They in turn educate pet owners, who are converted into subscribers through Trupanion’s contact center and/or website. From its subscribers, the firm generated a monthly profit (premiums minus payouts to vets and fixed costs) of $7.66 in Q4’23. With an average subscriber life of 73 months, that translates to a lifetime value (LTV) of $553 per pet.

Share Price Performance

However, owing to elevated new pet acquisition costs and veterinary cost inflation, profitability for Trupanion has been elusive. In the year before it went public (2013), the firm calculated a $612 LTV for each pet enrolled, based on monthly revenue of $42.57 per pet, who cost $103 on average to onboard. After its IPO, Trupanion embarked on a more aggressive acquisition strategy, which coupled with increasing competition in the industry, created substantial inflation in its marketing spend, peaking at $289 per pet in 2022.

The market shrugged off this surge in per pet spend, even though its LTV per pet peaked at $717 in 2021 as the focus in the low-interest rate environment was on growth in the largely underpenetrated market. Shares of TRUP rallied off a pandemic low of $22.48 in March 2020 to an all-time high of $158.25 in December 2021. This performance was despite the firm never achieving profitability. On a GAAP basis, its best showing was a loss of $0.03 a share in FY18. Ironically, after losing $0.16 a share (GAAP) in FY20, losses accelerated to $0.89 a share (GAAP) in FY21 as pet acquisition costs surged from $47.8 million to $78.6 million in an attempt to grow at any cost. After its stock touched an all-time high, losses continued to mount in FY22 with the firm shedding $1.10 a share as acquisition expenses continued their rise to $89.5 million.

The firm finally applied the brakes in FY23 to new pet acquisition spending, which fell to $77.4 million, or 21% on a per pet basis from $289 to $228. However, cost inflation from veterinarians rose significantly, with their invoice costs as a percentage of revenue (essentially Trupanion’s medical loss ratio) increasing from 72.5% in FY22 to 75.7% in FY23 versus its target ratio of 71.0%. The lower gross margin substantially impacted the lifetime value of a pet, which cratered 35% to $419 at YE23.

Unsurprisingly, shares of TRUP nosedived 88% from its all-time high to a six-and-half-year low of $19.14 in November 2023.

Likely in reaction to this development, it was announced on the day that the company reported Q1’24 financials (May 2, 2024) that Founder, Chairman and CEO Darryl Rawlings would be stepping aside as CEO in favor of Margi Tooth in August 2024.

One might be thinking, “why not just raise premiums” to cover its expenses? The answer: as an insurance firm, Trupanion is beholden to state regulatory authorities and in most cases must apply for rate increases. Even in the cases where there are few headwinds from regulators, the inability to accurately estimate veterinary invoice expenses results in timing mismatches, which in FY23 significantly impacted margins, resulting in a loss of $1.08 per share (GAAP) despite the 21% drop in new per pet acquisition expenses. That said, it did generate FY23 Adj. EBITDA of $6.4 million, up from $0.7 million in FY22.

Q1’24 Financials and Outlook

With the introduction of Ms. Tooth as the heir to the CEO position, Trupanion reported a decent quarter versus expectations, posting a Q1’24 loss of $0.16 per share (GAAP) and Adj. EBITDA of $4.8 million on revenue of $306.1 million versus a loss of $0.60 per share (GAAP) and Adj. EBITDA of negative $4.9 million on revenue of $256.3 million in Q1’23.

Lifetime value of the pet improved 2% sequentially from $419 to $428, although down 21% year-over-year, while new pet acquisition costs fell 5% sequentially and 16% year-over-year to $207. In the Subscription business, the firm’s medical cost ratio improved 230 basis points year-over-year to 75.3%.

These metrics were slightly ahead of the Street’s and Trupanion’s expectations, compelling management to marginally raise its FY24 guidance, which now stands at operating income of $110 million on revenue of $1.26 billion, based on range midpoints. If the top-line metric proves prescient, it would be the first time since the firm went public that it did not grow its top line by at least 20%. Either way, even though Ms. Tooth appears focused on the bottom line, there is no line of site on profitability for FY24 or FY25 on a GAAP basis.

The market reacted negatively to the news, with shares of TRUP down to $19.85 in the subsequent trading session in what appeared to be an overreaction (or a pile on by shorts). That said, they are up 55% in the past six trading sessions – more on this dynamic below.

Balance Sheet and Analyst Commentary:

Despite its struggles with profitability, the firm’s balance sheet is in solid stead, reflecting cash and short-term investments of $275.2 million against debt of $128.8 million. It should be noted that $38.1 million of the cash and short-term investments was unencumbered, while $237.1 million was domiciled at the firm’s insurance entities, which held $103.4 million in excess of their estimated risk-based capital requirement. Trupanion does not pay a dividend and has not repurchased any share under its buyback authorization in FY24, which is sanctioned until May 2026.

Since first quarter results hit the wires, Canaccord Genuity ($34 price target), Lake Street ($50 price target) and Bank of America ($49 price target) have assigned/reissued Buy ratings on the stock. Piper Sandler initiated the shares as a Hold with a $22 price target while Stifel Nicolaus maintained its Hold rating with an identical price target. On average, they expect Trupanion to lose $0.43 a share (GAAP) on revenue of $1.26 billion in FY24, followed by a nine cent a share loss in FY25 on revenue of $1.38 billion in FY25.

Outgoing CEO Rawlings gave the incoming CEO a vote of confidence, investing nearly $500,000 at an average price of $24.14 on May 7, 2024, upping his ownership interest to just under 615,000 shares.

Verdict:

The recent rally is a function of Trupanion’s stock bouncing off its now seven-year low after shorts attempted to drive it under its $19 support on May 3rd. The balance of the rally ($4.97 a share on May 13, 2024) was due to shares of TRUP appearing on a screen for heavily shorted stocks after Keith Gill (AKA Roaring Kitty), the ostensible leader of the January 2021 GameStop short squeeze mania (and the focus of the movie Dumb Money), returned to social media on May 13, 2024 after a three-year hiatus.

Therefore, until the company reaches profitability, it is a ‘show me‘ stock in my view.

")

(NASDAQ:SOFI)")

")