Q3 2024 Earnings Call Transcript")

")

Like most people in this world, I really enjoy eating. To be honest, I probably enjoy it more than I should. My love of food, however, has led me to some interesting companies over the years. One of these happens to be TreeHouse Foods (NYSE:THS), an enterprise that focuses on different packaged foods and beverages such as hot cereals, jams, crackers, cookies, and more. Well, back in January of this year, I decided to see what kind of upside potential, if any, the company might still offer investors.

Based on my analysis at the time, I ended up taking a slightly bullish stance on the company. This was because of the firm’s ability to grow revenue and improve its cash flows. Asset purchases and sales aimed at optimizing the company and growing it over the long haul also encouraged me, as did the fact that shares were attractively priced. Since then, however, things have not gone exactly as I thought they might. While the S&P 500 is up 8.9%, shares of this food producer are down 10.8%. Digging deeper, I definitely understand why. As of late, revenue, profits, and some cash flow metrics for the company have been on the decline. This follows a really robust 2023 fiscal year.

Despite these troubles, I remain optimistic about the long haul. Yes, this year might not be the best for the company. But shares are still quite cheap even after factoring in this weakness. This is true on both an absolute basis and relative to similar firms. Of course, this picture could always change. After all, before the market opens on May 6th, the management team at the enterprise is expected to announce financial results covering the first quarter of the company’s 2024 fiscal year. Leading up to that time, there are some data points that investors should be paying attention to. But assuming nothing significantly negative that’s unexpected comes out of the woodwork, I believe that my bullish stance is still appropriate.

A look at recent weakness

Author – SEC EDGAR Data

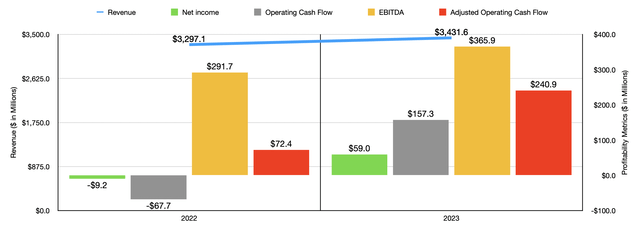

As you can see in the chart above, TreeHouse Foods had a rather strong showing in 2023. Revenue rose and the company’s bottom line went from a loss of $9.2 million to a profit of $59 million. Cash flows also improved without exception, with those improvements being rather remarkable. However, not all of 2023 ended up being a bullish time for the firm. To see what I mean, we need only look at results for the final quarter of the year. These can be seen in the chart below.

Author – SEC EDGAR Data

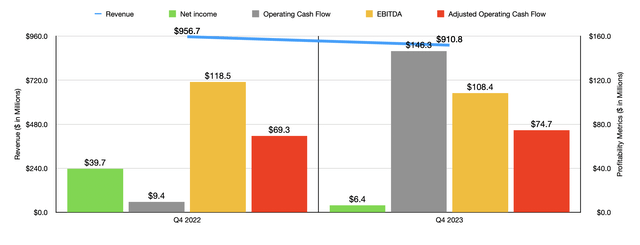

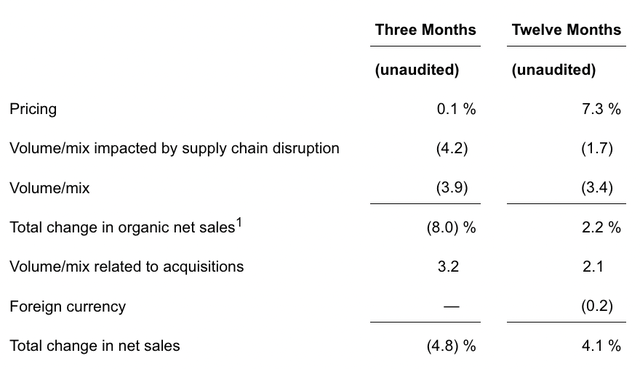

During the final quarter, revenue for the company totaled $910.8 million. That represents a decline of 4.8% compared to the $956.7 million generated one year earlier. According to management, this drop was in spite of a 0.1% improvement associated with the pricing of the company’s goods. It was also despite a 3.2% benefit associated with changes in volume and product mix associated with acquisitions that the company made throughout the year. Actual organic revenue was down 8%. And all of this had to do with changes in volume and product mix. Interestingly, however, management did break up the data into two separate categories there. As you can see in the image below, 4.2% of the decline involved supply chain disruptions. Management had previously made clear that they were having issues at one of its broth facilities, as well as with production involving pretzels and cookies. The other 3.9% of the decline, meanwhile, seemed to involve planned distribution exits associated with its in-store bakery and coffee categories.

TreeHouse Foods

With revenue falling, it’s no surprise that profits would decline. Net income went from $39.7 million down to only $6.4 million. In addition to revenue contributing to this, the company also suffered from a contraction in its gross profit margin from 18.3% to 16.7%. Management said this was mostly because of the aforementioned supply chain disruption at one of its broth facilities, as well as from a packaging quality matter that impacted cookies and pretzels. Unfavorable fixed cost absorption stemming from lower production volumes also played a role in this, as did higher costs for labor and manufacturing plant maintenance. While this may not seem like a big decline, when applied to the revenue generated during the final quarter of the year, it translates to about $14.6 million in reduced pre-tax profits.

The company also booked a $12.3 million non-cash mark to market charge involving its hedging activities because of changes in interest rates. And a note receivable that was repaid in the final quarter of the year resulted in interest income falling by $7.2 million. Other profitability metrics ended up coming in mixed. For starters, operating cash flow actually grew from $9.4 million in the final quarter of 2022 to $146.3 million the same time last year. If we adjust for changes in working capital, however, the growth was far more modest, from $69.3 million to $74.7 million. However, EBITDA for the company contracted from $118.5 million to $108.4 million.

For the year as a whole, management does seem to expect that the picture will improve. They anticipate revenue for 2024 of between $3.43 billion and $3.50 billion. This would be between flat and being up about 2% year over year. Profitability is also expected to grow, with operating cash flow expected to be around $275 million compared to the $240.9 million it was on an adjusted basis in 2023. Meanwhile, EBITDA is expected to be between $360 million and $390 million. That compares favorably, at the midpoint or high end, to the $365.9 million generated in 2023.

Author – SEC EDGAR Data

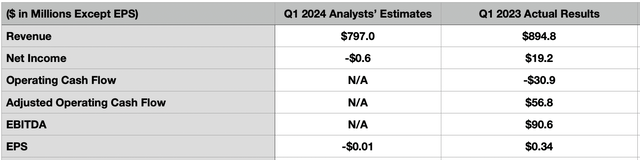

Given this expectation, you might think that the company would start off 2024 with a strong showing. But that’s unlikely to be the case. Analysts are currently forecasting sales of $797 million for the first quarter of the 2024 fiscal year. That would be down from the $894.8 million generated the same time last year. Interestingly, management also thinks the first quarter will be weak from a sales perspective, with revenue coming in at between $780 million and $810 million. Similarly, it’s anticipated that the bottom line for the company will also be weak, with a loss per share of $0.01. By comparison, in the first quarter of 2023, the company generated a profit per share of $0.34, amounting to a gain of $19.2 million. In the chart above, you can see other profitability metrics for the first quarter of 2023. Analysts have not forecasted anything else. However, management did say that EBITDA should be between $45 million and $55 million.

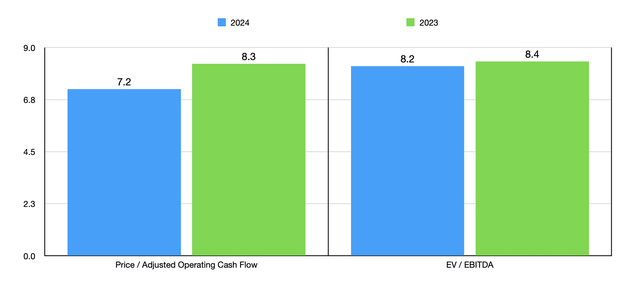

Author – SEC EDGAR Data

If we assume that management is correct when it comes to current guidance, the picture for the company should still be positive moving forward. Using their estimates for 2024, as well as historical results for 2023, I valued the company as shown in the chart above. It’s always great to see a company trading in the mid to high single digits. I then, in the table below, compared it to five similar firms. On a price to operating cash flow basis, two of the five were cheaper than TreeHouse Foods. This number declines to one of the five using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| TreeHouse Foods | 8.3 | 8.4 |

| Utz Brands (UTZ) | 18.6 | 30.4 |

| J&J Snack Foods (JJSF) | 13.2 | 14.5 |

| The Simply Good Foods Co. (SMPL) | 15.3 | 13.9 |

| Cal-Maine Foods (CALM) | 7.6 | 5.4 |

| Whole Earth Brands (FREE) | 8.1 | 15.9 |

Takeaway

At present, things are not exactly the best for TreeHouse Foods and its investors. Financial performance has been a bit weak and, if both management and analysts are correct, the first quarter of the 2024 fiscal year will show continued weakness. Once we are past this point, however, it looks as though the rest of 2024 will be rather robust. If this comes to fruition, shares do look attractively priced, both on an absolute basis and relative to similar firms. Because of this, and despite recent underperformance relative to the broader market, I would argue that a ‘buy’ rating is still appropriate right now.

")